The practical answer

- Short answer

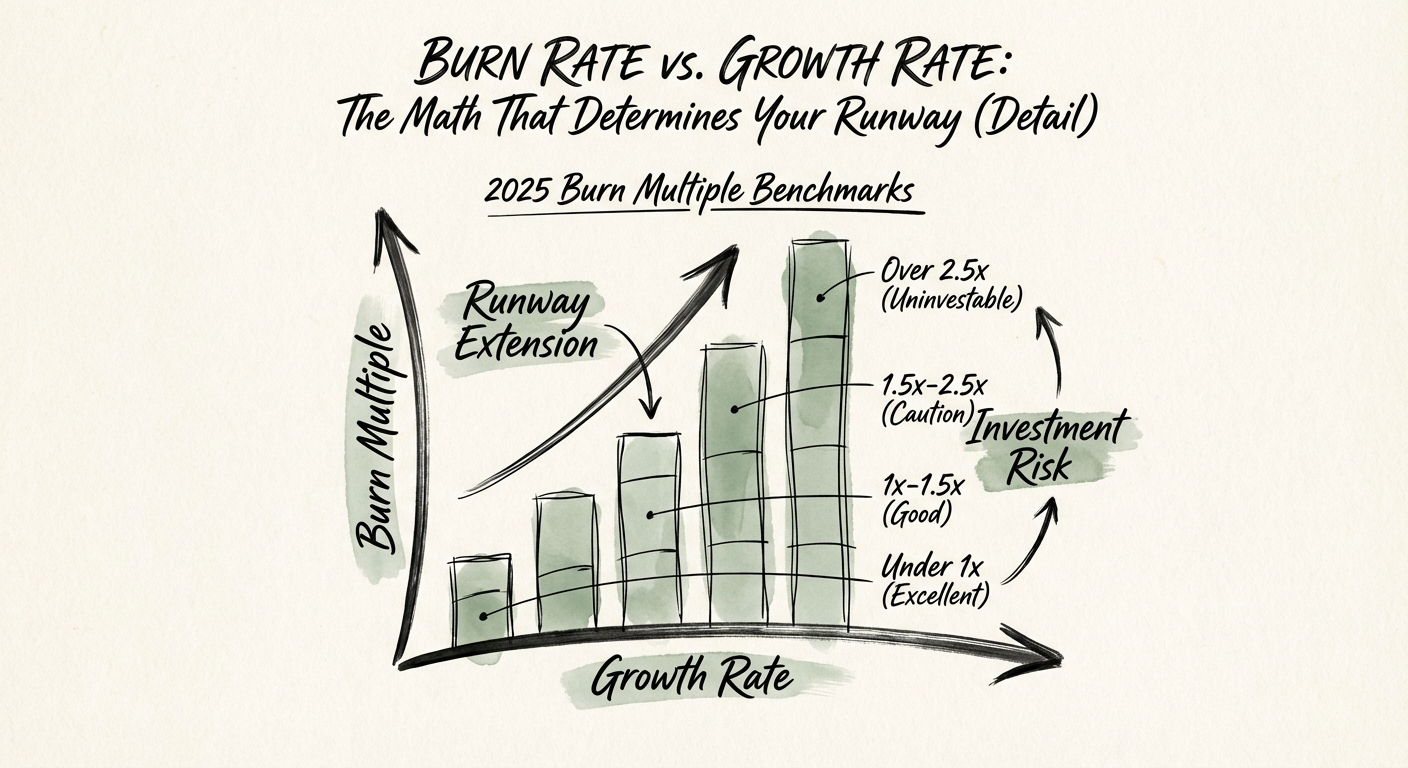

- Stop tracking vanilla burn rate. In 2025, the Burn Multiple is the only efficiency metric that matters. Here are the benchmarks for Series B survival.

- Best fit

- Industry: B2B SaaS. Function: Finance

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- 28 Months Median time between Series B and C rounds (up 61%)

The "Growth at All Costs" Era Left You with a Hangover

For the better part of a decade, the mandate from your board was simple: grow into your valuation. If you burned $3 million to add $1 million in ARR, nobody blinked. The next round was always six months away, and capital was cheap. That era didn't just end; it slammed shut.

Today, if you are a Series B founder bringing a "growth at all costs" P&L to a Series C pitch, you aren't just going to get a "no." You're going to get a lecture on unit economics. The market has shifted violently from rewarding top-line velocity to demanding efficient growth. Yet, too many founders are still managing their runway using vanilla "Monthly Burn Rate"—a vanity metric that tells you how fast you're dying, but nothing about whether you deserve to live.

The problem is simple: a $500k monthly burn is acceptable if you're adding $400k in Net New ARR. It is catastrophic if you're adding $50k. If you are only tracking cash out the door, you lack the operating visibility to steer. In the current fundraising climate—where the time between Series B and C has stretched by 61% to nearly 28 months—survival requires a new mathematical framework. You don't need more cash; you need better conversion of cash into equity value.

If you are currently sitting at a 3.0x Burn Multiple, you don't have a runway problem; you have a product-market fit problem masquerading as a cash flow problem.

The New North Star: The Burn Multiple

Stop obsessing over the Rule of 40 for a moment. While it remains the gold standard for late-stage private equity exits, it is a lagging indicator for early-stage operators. For a Series B company trying to extend runway, the Burn Multiple is the only diagnostic that matters.

Defining the Metric

Popularized by David Sacks at Craft Ventures, the Burn Multiple answers one question: How much cash do you burn to generate $1 of Net New ARR?

Formula: Net Burn / Net New ARR

The 2025 Benchmarks

Based on data from Bessemer Venture Partners and recent market analyses, the bar has been raised. Investors are no longer underwriting inefficiency.

- Under 1.0x (Excellent): You are capital efficient. For every dollar you burn, you add a dollar of recurring revenue. You control your own destiny.

- 1.0x – 1.5x (Good): This is the new standard for a healthy Series B company. You are investing in growth, but not recklessly.

- 1.5x – 2.0x (Suspect): You are entering the danger zone. Unless your LTV/CAC is exceptional, your board is getting nervous.

- Over 2.5x (Uninvestable): You are burning furniture to keep the house warm. In 2025, companies with a Burn Multiple >2.5x are failing to raise follow-on capital.

If you are currently sitting at a 3.0x Burn Multiple, you don't have a runway problem; you have a product-market fit problem masquerading as a cash flow problem. You cannot engineer runway extension purely through cost-cutting if your efficiency engine is broken. You must fix the ratio.

The "Death Zone" of Runway

Historical wisdom suggested 18 months of runway was safe. That advice is now obsolete. Data on fundraising cycles from Carta shows the median time between rounds has increased significantly. If you have less than 12 months of cash, you are already in the "Death Zone." You have lost leverage in M&A discussions, and you are unlikely to close a round before cash out. The new safe harbor is 24 to 30 months.

The Action Plan: From 2.5x to 1.5x

If your diagnostic shows you're inefficient, you cannot wait for the next quarter to pivot. You need an operational intervention immediately.

1. Zero-Based Budgeting for Every Department

Stop asking department heads what they need to "maintain" operations. Ask them to rebuild their budget from zero, justifying every expense against Net New ARR. If a marketing channel has a CAC payback period >18 months, remove it. If an engineering pod is working on a feature that won't drive revenue for two quarters, pause it. Efficiency requires disciplinedness.

2. The "Inactive Project" Purge

Most distressed startups are wasting cash into initiatives that are "90% done" but generating 0% revenue. We call these Inactive Projects. They eat developer cycles and cloud spend but feed no one. Conduct a board-level review of all R&D initiatives. If it doesn't ship and sell in 90 days, it gets cut.

3. Re-Forecast with Conservatism

Optimism is for pitch decks; pessimism is for cash flow management. Re-run your runway model assuming your sales cycle lengthens by 20% (a trend seen across B2B SaaS in 2025). Does your Burn Multiple hold up? If not, cut deeper now. The pain of cutting 15% of staff today is infinitely less than the pain of a down-round or liquidation in six months.

Conclusion

Your runway is not a timeline; it is a measure of your discipline. In a market that punishes inefficiency, the CEO who masters the Burn Multiple wins the right to build the future. The math is unforgiving, but it is also clear. Get to 1.5x, or get ready to exit.