The practical answer

- Short answer

- A buyer pays 7.1x for a B2B tech firm that runs without its founder and 3.5x for one that doesn't. Here's the exact math behind that 50% haircut — and how to close it.

- Best fit

- Industry: B2B Tech / Services. Function: Executive Leadership

- Operating path

- Founder Extraction → Operational Excellence → Interim Management

- Key metric

- 7.1x Average EBITDA multiple for autonomous (low founder dependency) firms

The diligence call where your growth chart stops mattering

Picture a Tuesday afternoon, week three of diligence on a profitable B2B software-services firm doing $4M of EBITDA. The financial review went fine — revenue is up, gross margin holds, churn is low. Then the buyer's operating partner asks a soft question: "Walk me through your last enterprise close. Who ran it?" The founder, proud, answers honestly. "I did. I always run the big ones — nobody else knows the product deep enough to handle the technical objections." Three more questions in, the same answer surfaces about pricing exceptions, about the renewal of the top-five account, about the one architecture decision that's blocking the roadmap. Every road leads back to one Slack handle.

That is the moment the growth chart stops setting the price. What the buyer just learned isn't that the founder is talented — they assumed that. They learned that the cash flows they're underwriting are attached to a person who, post-close, has every incentive to disengage. In their model, your firm just moved from the "platform" column to the "key-person risk" column, and those columns price very differently.

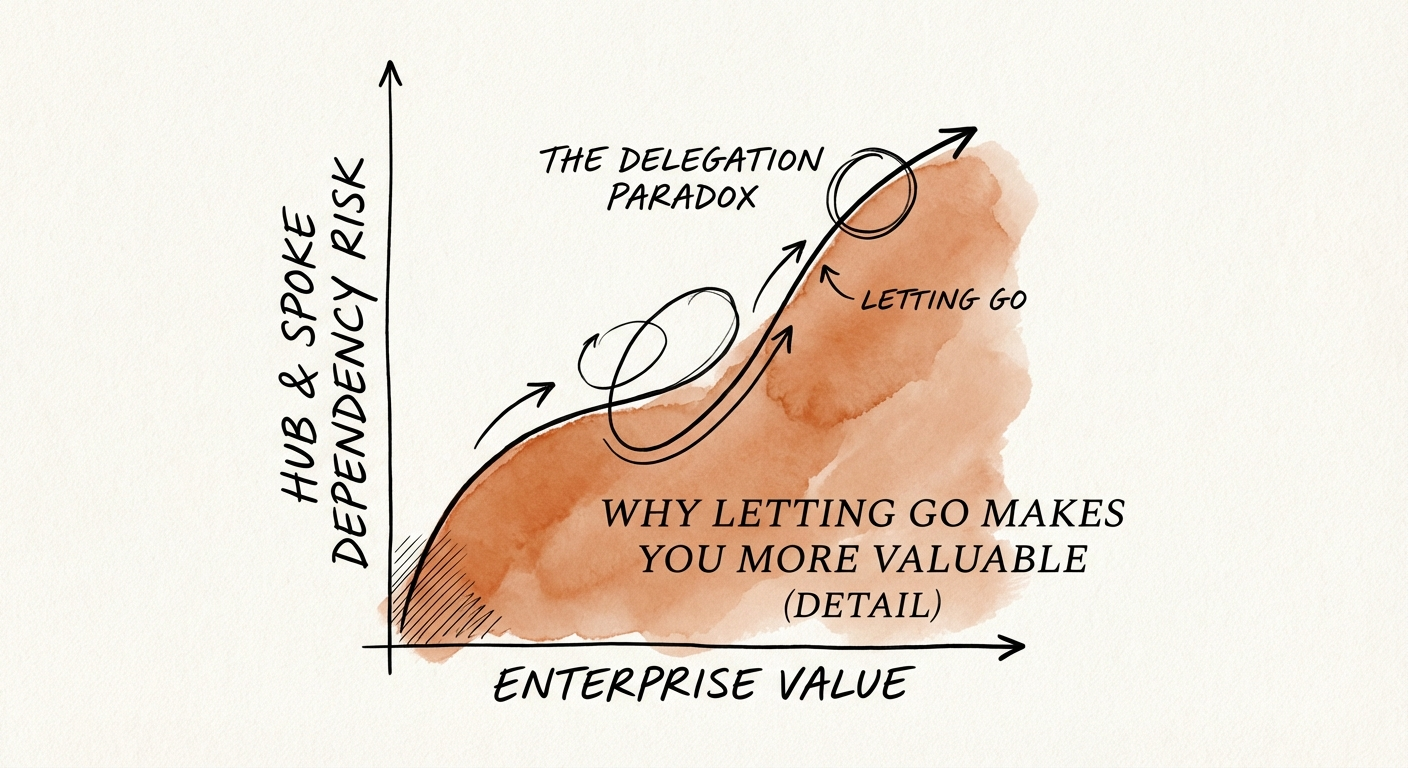

This is the Delegation Paradox, and it's brutal precisely because it inverts the instinct that got the founder here. In the zero-to-five-million phase, doing everything yourself was the strategy — you were faster, sharper, and more committed than anyone you could afford to hire. But somewhere past $10M ARR the same heroics flip from asset to defect. The buyer isn't grading effort. They're grading what happens to revenue if you vanish, and "I close all the big deals" is the answer they fear most.

The cruel part: the better the founder is at being indispensable, the worse it reads in the room. A mediocre CEO who built a sales team that closes without them is worth more than a brilliant one who never did. You haven't built a company that's hard to replace you in — you've built a job that happens to throw off profit, and almost nobody writes a premium check for a job.

The founder who closes every big deal isn't proving how good they are. They're proving the business is one resignation letter away from a 50% discount.

3.5x versus 7.1x: putting a price tag on your own indispensability

This isn't a soft "work on your work-life balance" argument. It is a line item. The Value Builder System, working from a dataset of more than 60,000 businesses, found that firms scoring high on owner dependency — what they call the Hub-and-Spoke pattern — drew acquisition offers averaging 3.5x pre-tax profit. Firms that ran autonomously, where the founder operated as a strategist rather than the tactical bottleneck, averaged 7.1x. Same profit. Roughly double the price. The entire delta is the buyer's answer to one question: does this thing still work on Monday if the founder is on a beach?

Run it against the $4M-EBITDA firm from that diligence call. At 3.5x, that's $14M of enterprise value. At 7.1x, it's $28.4M. The "nobody does it like I do" reflex isn't costing a vacation — it's costing roughly $14M in equity, most of it the founder's. William Buck's corporate finance analysis frames the same thing from the buyer's side: identified key-person risk typically triggers a discount of 20% to 50% on enterprise value. The haircut isn't a penalty for being founder-led. It's the price of the risk you've quietly placed on the buyer's balance sheet.

And the discount is the optimistic outcome — it assumes a deal still happens. Two uglier mechanics show up first:

- The earn-out cage. Sophisticated buyers don't just discount founder risk; they engineer around it. Instead of cash at close, you're handed a three-year earn-out tied to numbers that only hit if you keep personally running the deals you swore you'd hand off. You've sold the company and kept the job, with the equity held hostage to your own continued exhaustion. Walk away early or burn out, and the back-end evaporates.

- The buyers who just leave. Strategic Exit Advisors note that many strategic acquirers won't bother negotiating the discount at all — they pass entirely rather than absorb the integration risk of a firm whose institutional knowledge lives in one head. A thin buyer pool doesn't just lower the price; it removes the competitive tension that creates a price in the first place.

So when you protect quality by insisting on closing the deal yourself, the trade you're actually making is short-term control of one deal for long-term destruction of your multiple. Stated that plainly, it's a trade no rational owner takes.

Architecting your way out, not abdicating

The reason most founders fail at delegation isn't ego — it's that they confuse delegating with dumping. They hand off the task without handing off the judgment, the process blows up, it confirms the belief that "nobody does it like I do," and the cycle reinforces itself. Closing the 3.5x-to-7.1x gap isn't about working less. It's about moving the decisions out of your head and into a system a buyer can underwrite. Three places to start, in order of valuation impact:

1. Encode the revenue judgment first, not the busywork

Don't begin with expense approvals. Begin with the activities that scared the buyer in that diligence room: how you qualify, how you handle the technical objection that supposedly only you can answer, how you set the pricing exception, how you save the account that's about to churn. Those are the decision nodes carrying your multiple. Turn the "gut feel" into something written, testable, and teachable — the foundation our turnkey documentation guide walks through. If a process lives only in your head, it cannot be sold; it can only be inherited, and buyers don't pay platform prices for inheritances.

2. Demote yourself from closer to coach

If you are still the only one who can land the big enterprise deals, your sales team is functioning as expensive administrative support for you. The fix is to convert what you do instinctively into a repeatable motion — discovery scripts, objection libraries, deal-desk rules — so a capable rep, not a clone of you, can close. Our breakdown of moving from founder-led to scalable sales covers exactly that handoff. The signal a buyer wants isn't "the founder is a great closer." It's "great closing happens here whether or not the founder shows up."

3. Run the two-week test — and watch what breaks

The cleanest diagnostic costs nothing: leave for two weeks and don't check email. You're not doing it to rest — you're doing it to surface, in real time, every decision that silently routes through you. The things that pile up are your exact key-person risks, itemized for free. Use our Founder Extraction Playbook to take that list and systematically reassign each node. Do this twelve to eighteen months before you want to raise or sell, not during diligence, because a buyer can tell the difference between a business that has run without you and a founder who started practicing last quarter. The paradox resolves cleanly once you act on it: the less your company needs you, the more it — and your stake in it — is worth.