The practical answer

- Short answer

- Most VC-backed founders are replaced by Series C. Here is the exact failure pattern between Series A and B, and the four moves that get you through it as CEO.

- Best fit

- Industry: B2B Tech. Function: Executive Leadership

- Operating path

- Founder Extraction → Operational Excellence → Interim Management

- Key metric

- 52% Founders replaced by Series C (Wasserman)

The board meeting where you stop being the hero

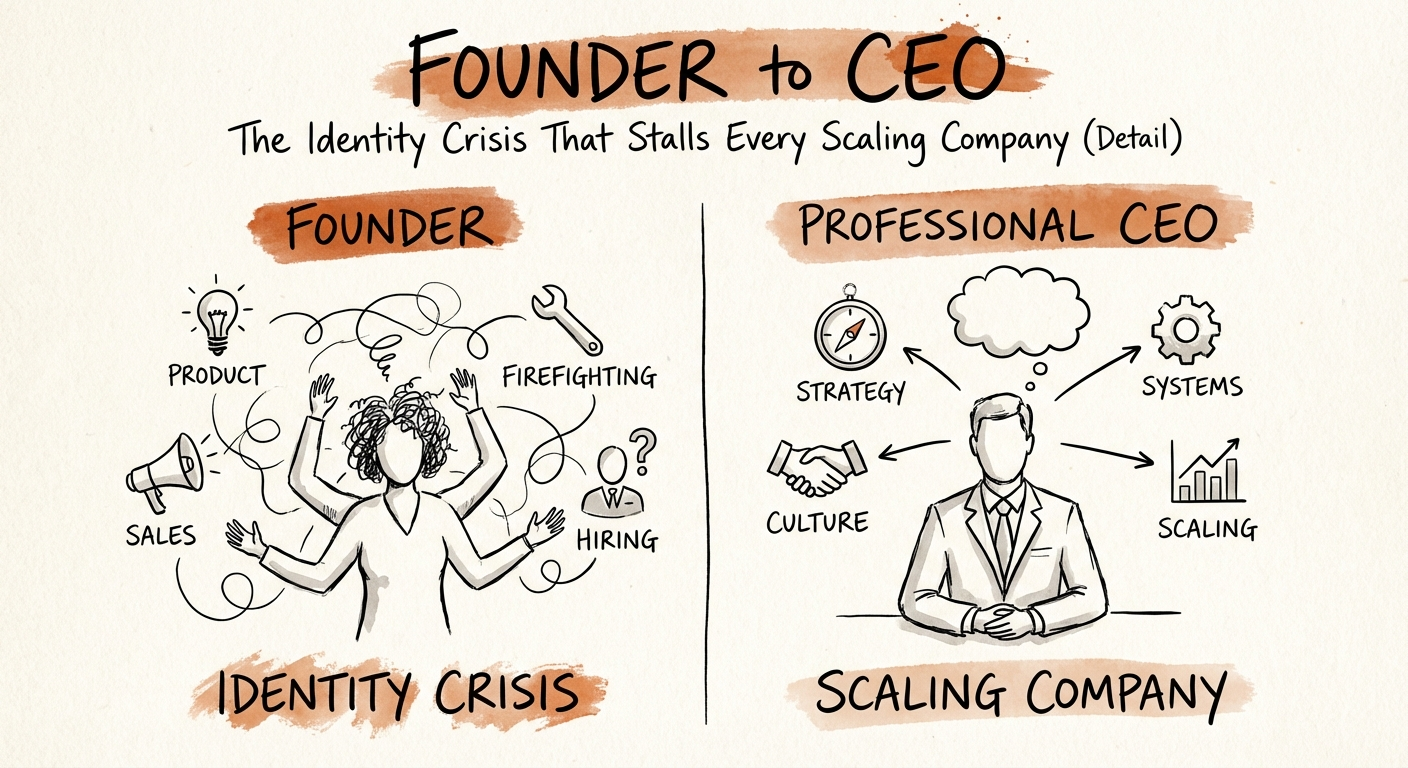

Picture the Series B board meeting. The deck looks fine. ARR is climbing past $12M. But three of your directors are quietly asking each other the same question between sessions: can this founder run a 200-person company, or are we funding a $20M ceiling? They are not waiting for the product to break. They are waiting to see whether you will redefine your own job before the company forces them to redefine it for you.

That is the real Series B exam, and it has almost nothing to do with metrics. From $0 to $5M, you won on heroics. You closed the first dozen logos personally. You wrote the schema. You knew every account by the founder's first name. Force of will was the entire operating system, and your investors loved it, because at that stage a founder who is everywhere is exactly what gets funded.

The cruel part is that the behavior that earned the Series A is the behavior that loses the Series C. Past roughly $10-20M ARR, "I'll just handle it" stops being leadership and starts being the bottleneck. You hover over deals your VP of Sales should own. You reopen architecture decisions your CTO already settled. Every escalation routes back to you because you trained the org to route it there, and now your calendar is a wall of tactical firefighting that leaves zero hours for the two things only you can do: capital allocation and executive hiring.

Noam Wasserman spent years measuring exactly this pattern across thousands of startups. His finding, laid out in The Founder's Dilemma, is blunt: by the time a company raises its third round, the founder is usually no longer the CEO. Not because they failed. Because they could not, or would not, change jobs.

Your board isn't waiting to see if you can scale. They're waiting to see if you'll let go before they have to make you. The founders who survive Series B decide first.

Rich versus King, priced in a term sheet

Wasserman's research puts a number on the trap that most founders treat as an emotion: 52% of founders are replaced by the time the company reaches Series C, and the majority of those exits are board-initiated rather than voluntary. He frames the underlying choice as "Rich versus King." Hold total control and you stay King of something small. Trade operational control for a real executive bench and you take a thinner slice of a far larger pie, often materially more valuable in absolute dollars. The founders who insist on being King tend to end up with neither.

For VC-backed companies, the math has a specific shape because the failure isn't smooth, it's stage-gated. Roughly a third of startups die between Series A and Series B. That gap is where founder heroics quietly stop scaling: the same hands-on intensity that closed the seed round now caps the pipeline, slows hiring, and starves strategy. The companies that clear it look almost nothing like the ones that don't, and the difference is rarely the product.

The discount waiting for you at exit

If your endgame is an acquisition, the identity crisis carries a literal price tag, and I have sat on the buy side watching it get applied. In diligence we hunt for Key Person Risk: if you are the only one who can close enterprise deals or the only person who actually understands the roadmap, the business breaks the day you leave, and a buyer prices that in. Willamette Management Associates work on key-person valuation puts those discounts in the 15% to 25% range. On a $40M outcome, that is the difference between $40M and $30M, erased by the fact that you never built anyone to replace you.

So the dependency you think is protecting quality is the same dependency a future acquirer reads as fragility. Every decision that only you can make is a deduction from your own enterprise value, sitting on the term sheet whether you see it or not.

Four moves before your next raise

You cannot decide your way into being a CEO; you have to engineer the handoff while the company is still moving. Here is the sequence I walk founders through, in order, because doing them out of order is how the wheels come off.

1. Audit two weeks of your own calendar

Pull your last ten working days and tag every block as CEO work (strategy, hiring, capital allocation, board) or operator work (sales calls, code review, support escalations). If CEO work is under half your hours, you are not yet running the company you are trying to raise on. Most founders are shocked to find they are functioning as a very expensive Super-VP of Sales.

2. Document how you decide, not what you do

Tribal knowledge is the enemy of equity value. Don't write down tasks, write down the heuristics behind your judgment calls: which deals you walk away from and why, what trips your "this hire is wrong" alarm, how you weigh roadmap bets. If you can't articulate the rule, you can't delegate the decision. (Our tribal-knowledge-to-turnkey guide shows the format.)

3. Hand off clean, then leave the room

When you hire a VP, give them a focused 30-day download and then physically remove yourself from their meetings. Six months of "collaborating" is just supervised hovering, and the team learns it. If everyone still glances at you for the final yes, you have delegated nothing. We go deeper on this in escaping founder-led sales, and the same principle applies to product and engineering.

4. Sit with feeling useless

This is the hard one. Operator work feels like output: emails sent, commits pushed, fires extinguished. CEO work, recruiting and thinking and aligning, feels like doing nothing for weeks until it suddenly compounds. You will feel lazy. That feeling is the old identity pulling you back toward the weeds. Ignore it.

Wasserman found the Series A to B crossing is where this gets decided, and it's the gate where roughly a third of companies fall. The founders who clear it are the ones who treated the transition as a project with a deadline, not a someday. If you want a structured path through it, that is the core of our founder extraction work: get you out of the weeds without the business missing a beat.