The practical answer

- Short answer

- 80% of tech M&A deals are now 'scope' plays. Here is the PE Operating Partner's diagnostic for when to consolidate tech stacks vs. keeping them separate.

- Best fit

- Industry: B2B SaaS / Tech Services. Function: Product & Engineering

- Operating path

- Migration & Integration → Turnaround & Restructuring → Transaction Advisory Services

- Key metric

- 80% Of tech M&A deals are 'Scope' plays requiring product integration (Bain)

The Holding Company Discount

For years, Private Equity’s playbook for tech services and SaaS was simple: buy a platform asset, then bolt on smaller competitors to aggregate EBITDA. The goal was financial arbitrage—buying at 4x, selling at 12x. But in 2026, the market has smartened up. Acquirers are no longer paying platform premiums for what is essentially a loose confederation of mismatched tech stacks, fragmented customer support teams, and siloed data.

This is the Holding Company Discount. If your portfolio company markets itself as a unified “end-to-end platform” but requires customers to log into three different portals and sign four different contracts, you aren't building a platform. You are building a museum of technical debt.

According to Bain & Company’s 2024 M&A Report, nearly 80% of all tech M&A activity is now comprised of “scope” deals—acquisitions designed to add new products or capabilities rather than just scale. The investment thesis relies on revenue synergies: cross-selling Product B to Product A’s customers. Yet, Bain notes that failure to integrate product portfolios is the single most common reason these revenue synergies never materialize.

The Integration Trap

The Operating Partner’s dilemma is clear. Consolidate too aggressively, and you risk stalling the roadmap for 18 months while engineers rewrite code that already works (the “Franken-stack” nightmare). Consolidate too loosely, and you bleed margin through duplicative hosting costs, security vulnerabilities, and a disjointed customer experience that kills Net Dollar Retention (NDR).

You need a diagnostic framework—not a gut feeling—to decide which assets get rewritten, which get wrapped, and which stay independent.

You aren't building a platform. You are building a museum of technical debt if you don't integrate.

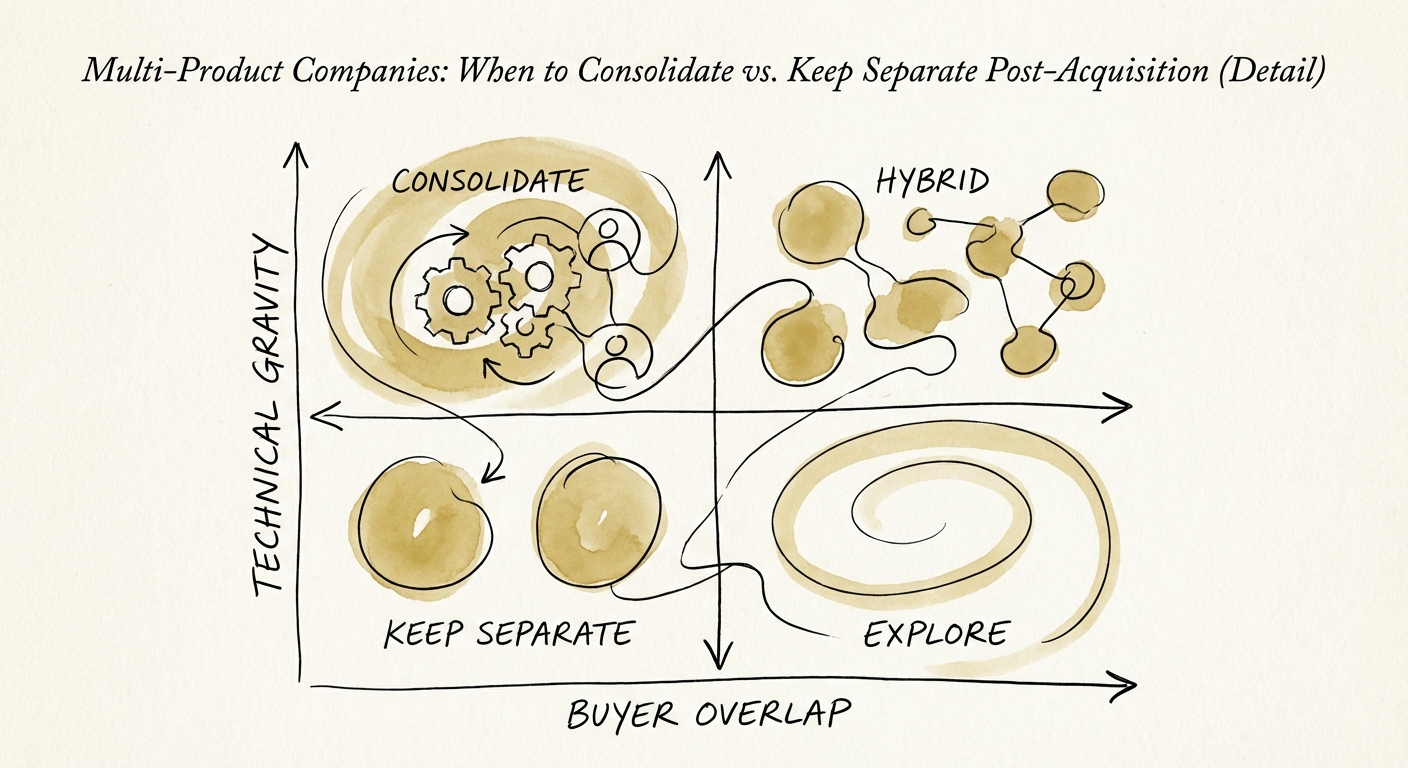

The Product Consolidation Diagnostic Matrix

Before you greenlight a $3M refactoring project or fire a CTO for resisting integration, map your acquisition against these three zones. The decision relies on two axes: Buyer Overlap (Do the same humans buy both products?) and Technical Gravity (How heavy is the lift to integrate?).

Zone 1: The “Portfolio” Play (Keep Separate)

- Profile: Low Buyer Overlap, High Technical Gravity.

- Scenario: You acquired a gov-tech firm selling to the DoD to complement your commercial HR SaaS. The buyers are different, the compliance requirements (FedRAMP) are distinct, and the tech stacks share no DNA.

- Strategy: Do Not Consolidate. Cross-sell is a marketing motion, not a product motion. Force-fitting these stacks will destroy value. Keep P&Ls separate. Focus on back-office synergies (Finance, HR) rather than product engineering.

Zone 2: The “Unified Experience” Play (UI/Data Integration)

- Profile: High Buyer Overlap, High Technical Gravity.

- Scenario: You bought a legacy on-premise ERP add-on to sell to your cloud-native CRM base. The customers want a single dashboard, but rewriting the legacy code is a two-year value-destructive project.

- Strategy: The Wrapper Approach. Build a unified Single Sign-On (SSO) and a shared data layer (API gateway) that feeds a common reporting dashboard. Leave the messy back-ends separate for now. This delivers 80% of the customer value (unified experience) at 20% of the integration cost.

- Metric to Watch: Time-to-First-Integrated-Value. If it takes longer than 90 days to show customers a combined win, you are failing.

Zone 3: The “Platform” Play (Full Consolidation)

- Profile: High Buyer Overlap, Low Technical Gravity.

- Scenario: You acquired a modern, API-first competitor to capture their market share. The stacks are similar (e.g., both React/Node), and the feature sets overlap.

- Strategy: Disciplined Consolidation. Pick the winner (usually the acquirer’s stack, but not always) and migrate customers. Retire the losing brand and code. Maintaining two similar codebases doubles your R&D cost for zero marginal revenue.

The Financial Impact of Inaction

Keeping stacks separate isn't free. McKinsey research indicates that companies fail to capture expected synergies in 70% of deals, often because they underestimate the “shadow costs” of non-integration: cybersecurity fragmentation (doubling the attack surface), split support teams (training reps on two tools), and inability to leverage data for AI initiatives.

The 100-Day Integration Roadmap

Once you have diagnosed the zone, execution is everything. Most Private Equity value creation plans fail because they treat integration as a “Year 1” goal. It is a “Quarter 1” mandate.

Days 1-30: The Triage

Stop the bleeding immediately. Freeze all non-critical roadmap items on the acquired asset. Conduct a Technical Debt Assessment to verify what you actually bought (due diligence code audits are rarely deep enough). Establish the “Integration Management Office” (IMO) with a clear mandate: Protect the Revenue.

Days 31-60: The Connectivity Layer

Even if you are in Zone 1 (Keep Separate), you need basic connectivity. Implement CRM consolidation so sales reps can actually cross-sell. If you are in Zone 2 or 3, ship the “Thread”—a single common feature (like a unified login or a shared report) that proves to the market that these companies are one. This is crucial for retention.

Days 61-90: The Retire-or-Retain Decision

This is where Operating Partners earn their carry. You must decide which legacy features, products, or versions are being retired. Communicate this to customers with a migration path. Silence undermines retention during M&A; clarity saves it.

Conclusion: Valuing the Platform

The market rewards platforms, not holding companies. A truly integrated platform with unified data and workflows commands a valuation multiple of 8x-12x revenue. A collection of loose assets trades at 4x. The cost of integration is high, but the cost of the “Valuation Gap” is higher.

Don't just buy revenue. Build the architecture that makes that revenue sticky, scalable, and saleable.