The practical answer

- Short answer

- Median hold periods have hit 6.5 years. If your portfolio company shows these 10 red flags, you need to intervene before the exit window closes.

- Best fit

- Industry: Private Equity. Function: Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 6.5 Years Median PE Holding Period (Highest in Decade)

The "Green Dashboard" Lie

You have seen the slide deck. The revenue chart is up and to the right (mostly). The EBITDA adjust-backs are aggressive but defensible. The CEO is confident. On the surface, the asset is performing. But in the boardroom, you have a gnawing feeling that the numbers do not match the operational reality you see on the ground.

You are right to be concerned. The era of pure financial engineering is dead. With median holding periods now exceeding 6.5 years—the highest in over a decade—you can no longer rely on multiple arbitrage or cheap debt to hide operational rot. According to McKinsey, top-quartile funds now derive over 50% of their returns from operational improvements, not leverage.

The danger isn't the disaster you see coming; it's the silent erosion of value that happens while the dashboard still looks green. We call this the "Green Dashboard Lie." By the time the KPIs turn red, you have already lost four quarters of value creation. You are now in turnaround mode, not growth mode.

As an Operating Partner, your job is not just to read the board packet; it is to detect the faint signals of distress before they become impairments. If you see more than three of the following ten signs, your portfolio company isn't just "working through some issues." It is in trouble.

You can no longer rely on multiple arbitrage or cheap debt to hide operational rot. Top-quartile funds now derive over 50% of their returns from operational improvements.

The 10 Operational Red Flags

1. The EBITDA-Cash Conversion Gap

The most common early warning sign is a divergence between Adjusted EBITDA and operating cash flow. If a company reports $4M in EBITDA but needs to draw on its revolver to make payroll, you have a problem. This usually signals aggressive capitalization of software development, ignored working capital bloat, or revenue recognition policies that are out of sync with collections. "Quality of Earnings" isn't just a pre-deal metric; it is a monthly pulse check.

2. The "Heroics" Dependency

If the founder still personally closes the biggest deals, writes the critical code, or resolves every major customer escalation, the company is hard to sell. This is not "hands-on leadership"; it is a single point of failure. Valuation data suggests that key-person dependency can result in a 15-20% discount on exit multiples. If the systems do not work without the founder, you do not own a company; you own a job.

3. The Forecast Variance Swing (>10%)

Ask for the sales forecast from three months ago and compare it to actuals. If the variance is consistently greater than 10%—in either direction—nobody knows what is happening. A "beat" based on luck is just as dangerous as a "miss" based on incompetence because neither is repeatable. Unpredictable revenue streams kill debt covenants.

4. The Silent Tech Debt Accumulation

Development velocity is slowing down. Features that used to take two weeks now take six. The CTO blames "complexity," but the reality is technical bankruptcy. A recent study highlights that technical debt acts as a silent killer in M&A due diligence, often triggering price retrades after the LOI. If your R&D spend is increasing while output decreases, you are paying interest on code you haven't fixed.

5. The "Committee" Deadlock

Decisions that should take days are taking months. The leadership team has become a debating society. This is often a symptom of post-merger indigestion, where cultures clash and authority is ambiguous. AlixPartners reports that 51% of PE executives cite financial performance as a source of tension, often driven by a paralysis in decision-making velocity.

6. High Turnover in "Engine Room" Roles

Ignore C-suite turnover for a moment. Look at your Senior Engineers and Account Executives. If you are churning the people who build the product or own the customer relationships, you have a cultural bleed that will show up in the P&L in six months. Replacing a salaried employee costs 1.5x to 2x their annual compensation, a direct hit to EBITDA that no add-back can fix.

7. Tribal Knowledge Monopoly

When you ask, "How does this process work?" and the answer is "Ask Steve," you have a scalability crisis. Undocumented processes are the primary barrier to integrating add-on acquisitions efficiently. If your value creation plan relies on "synergies," tribal knowledge is the enemy.

8. The Customer Concentration Trap

A single customer representing 20% of revenue is a risk; a single customer representing 20% of margin is a high-risk negotiating position. We often see portfolio companies hesitant to raise prices or enforce terms on their "Whale" clients, slowly eroding gross margins to keep the revenue optics intact.

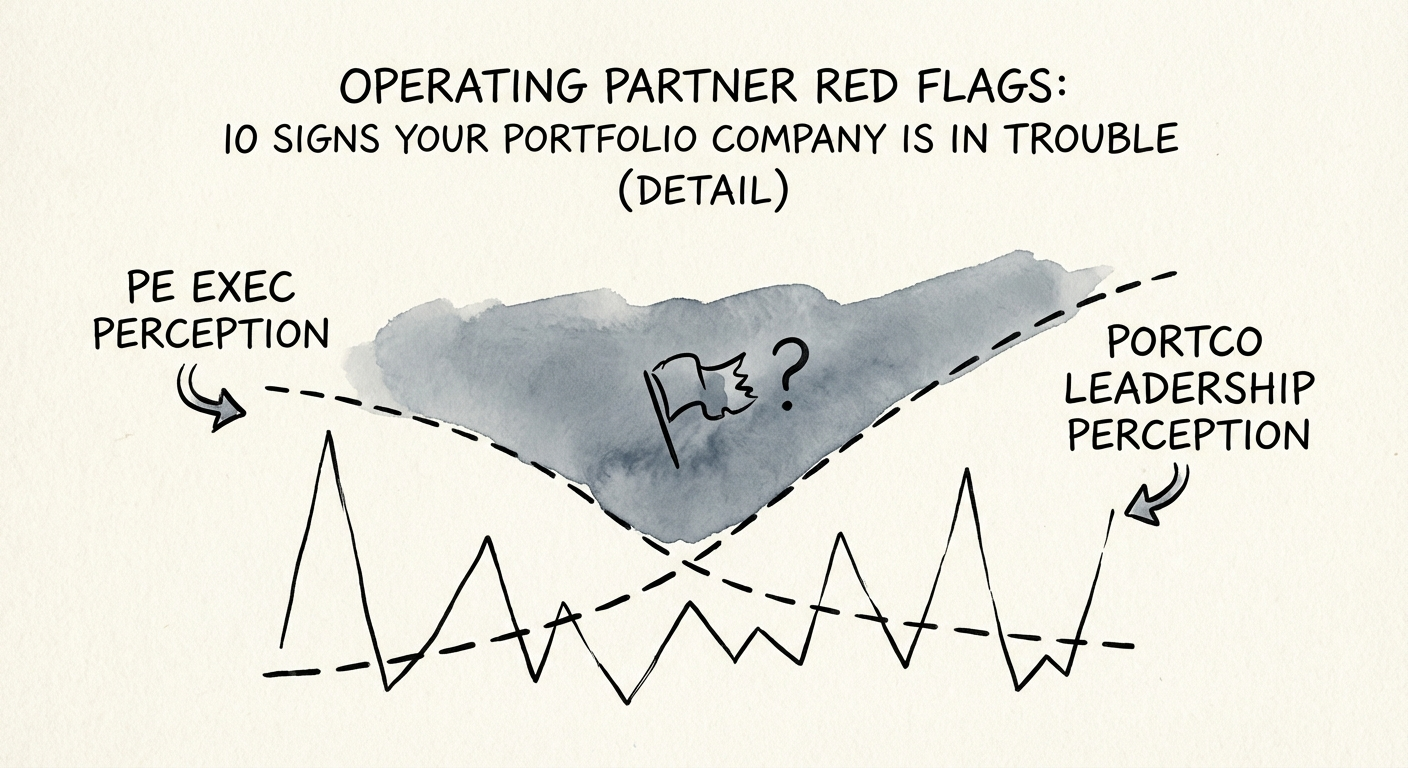

9. The Misalignment Gap (41% vs. 13%)

There is a dangerous disconnect in perception. AlixPartners found that while 41% of PE executives view the quality of portfolio company leadership as a significant challenge, only 13% of those leaders agree. If you think the management team is weak and they think they are crushing it, you cannot execute a value creation plan. You are speaking different languages.

10. The "Just One More Feature" Sales Excuse

When sales miss targets, do they blame the product? "If we just had X feature, we would win." This is rarely a product problem; it is a product-market fit or sales methodology problem. Building features to chase revenue is the fastest way to bloat your roadmap and destroy margins.

The Intervention Framework: Triage, Fix, or Sell

If you identified three or more of these red flags, the passive approach is over. You need to intervene, but "trying harder" is not a strategy. You need a structured triage process.

Step 1: The 30-Day Diagnostic

Stop relying on the board pack. Parachute a neutral third-party operator into the business for 30 days. Their mandate is not to consult, but to audit the operational reality. How real is the pipeline? How much technical debt actually exists? Who is really doing the work?

Step 2: The "Wartime" Re-Forecast

Tear up the budget. Build a 13-week cash flow forecast and a bottom-up revenue model based on proven conversion rates, not hope. This establishes the baseline for survival. If the company cannot survive on its own cash flow within two quarters, you are looking at a capital injection or a distressed sale.

Step 3: The Talent Upgrade

You cannot fix a "Level 5" problem with "Level 3" talent. If the CEO is a founder who has hit their ceiling, have the hard conversation now. If the VP of Sales is a glorified individual contributor, replace them. The misalignment gap mentioned above usually stems from PE firms waiting too long to upgrade talent out of fear of disrupting the culture. The culture is already disrupted; you are just formalizing it.

Conclusion: Operational Engineering is the Only Way Out

The days of buying low, doing nothing, and selling high are gone. The 2025 vintage of returns will be defined by Operational Alpha. Red flags are not failures; they are data. The failure is seeing them and doing nothing.