The practical answer

- Short answer

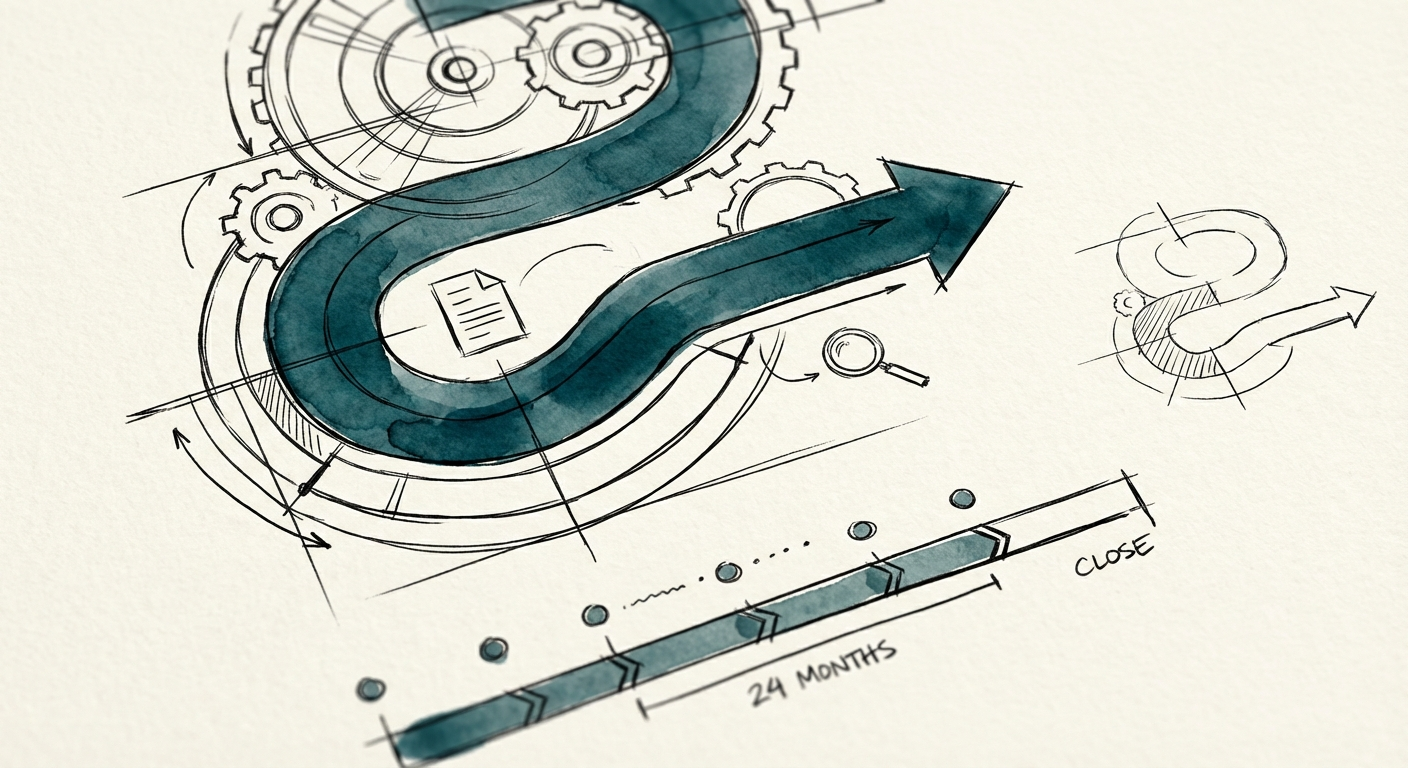

- Standard exits take 6 months; successful ones take 24. A diagnostic timeline for founders to fix operations, clear due diligence, and secure a 5-10% valuation premium.

- Best fit

- Industry: Private Equity. Function: Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 30% Faster Deal Closure with Sell-Side Diligence

The "Fire Drill" vs. The Engineered Exit

Most founders believe they can decide to sell in January and be on a beach by July. This delusion is the primary reason why, according to Harvard Business Review data, 70% to 90% of acquisition attempts fail. They don't fail because the product is bad; they fail because the company cannot survive the invasive surgery of private equity due diligence.

For a founder-led company, the gap between "market-ready" and "diligence-ready" is often measured in millions of dollars of lost enterprise value. When you rush to market without a 24-month runway, you are forced to trade on potential rather than proof. Buyers smell this desperation. They see your "heroics"—the late nights, the sheer force of will holding the P&L together—not as assets, but as Key Person Risk.

The difference between a failed auction and a multiple-expanding exit is Operational Engineering. It is the deliberate process of transforming a personality-driven business into a process-driven asset. This isn't about polishing the deck chairs; it's about structural remediation before the home inspector arrives. If you wait for the Letter of Intent (LOI) to start organizing your data room, you have already lost leverage.

Deals don't fail because the product is bad; they fail because the company cannot survive the invasive surgery of private equity due diligence.

The 24-Month Countdown Framework

An engineered exit follows a rigid reverse timeline. We break this down into four distinct operational phases designed to maximize transferability and valuation.

Phase 1: Operational Extraction (Months 24–18)

Your first priority is not financial, but structural. You must fire yourself. If you are still the Chief Selling Officer or the head of product strategy, your multiple is capped. Acquirers do not pay 12x EBITDA for a job they have to fill the day you leave.

- Goal: Reduce "Founder Hours" in delivery/sales by 80%.

- Action: Document the "Tribal Knowledge" currently stored in your head. Implement founder extraction protocols that delegate decision-making authority, not just tasks.

Phase 2: The Financial "Mock" Audit (Months 18–12)

Six months into the process, you strip the financials down to the studs. This is where you conduct a Sell-Side Quality of Earnings (QofE). Most founders wait for the buyer to do this, which is a tactical error. A buyer's QofE is designed to find price reductions; your QofE is designed to defend add-backs.

- Benchmark: Industry data shows that companies conducting sell-side due diligence achieve valuations 5% to 10% higher and close 30% faster than unprepared peers.

- Action: Identify and remediate revenue leakage and define your EBITDA adjustments now, so they are defensible facts rather than negotiation points later.

Phase 3: The Growth Story & Data Room (Months 12–6)

With operations stabilized and financials clean, you shift to the forward-looking narrative. This is not about projecting hockey-stick growth that no one believes; it's about demonstrating predictability.

- Goal: Show 4 consecutive quarters of forecast accuracy >90%.

- Action: Build a "Virtual Data Room" (VDR) that mirrors a PE readiness checklist. If a buyer asks for a contract, you should have it in 5 minutes, not 5 days. Speed breeds confidence.

Phase 4: The Market Process (Months 6–0)

By the time you formally engage investment bankers, the heavy lifting should be done. Your role shifts from "fixer" to "steward." The most dangerous trap in the final mile is distraction. We frequently see EBITDA compress by 15% during the deal process because the CEO is too busy answering diligence questions to run the sales team. This "deal fatigue" is a leading cause of broken transactions.

The "Transferability Premium"

Ultimately, private equity firms are buying certainty. They pay a premium for businesses that run better without the founder than with them. A 24-month timeline allows you to prove that the machine works independently of its creator.

Don't view this timeline as a delay. View it as an investment. Every month you spend documenting processes, verifying metrics, and removing yourself from the critical path is a direct deposit into your final exit value. The market is crowded with messy, founder-dependent companies. Be the one that is engineered to scale.