The practical answer

- Short answer

- Why some services firms trade at 15x EBITDA while others struggle at 4x: 2025 consulting valuation multiples and the recurring-revenue premium buyers pay for.

- Best fit

- Industry: Professional / IT Services. Function: M&A / Exit

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

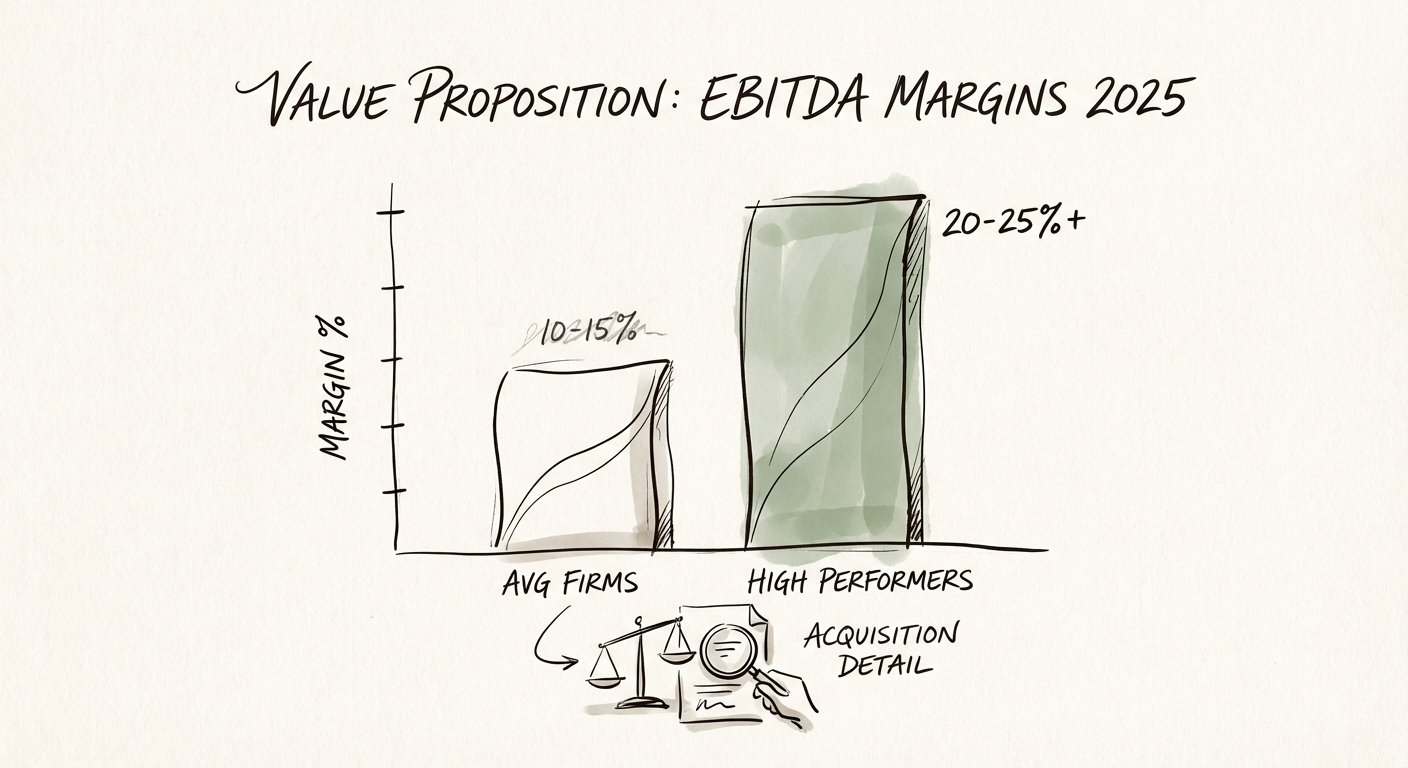

- Key metric

- 9.8% Average 2024 PS EBITDA margin, down from 15.4%

The Volatility Discount: Why Buyers Handcuff Services Firms

If you are a Private Equity sponsor, you hate surprises. You tolerate professional services firms because they are cash cows, but you resent them because the milk dries up the moment key partners leave or the economy sneezes. That resentment shows up in the valuation: while your SaaS portfolio trades on revenue multiples, your services firms are often handcuffed to a low single-digit EBITDA multiple.

The market data for 2024 and heading into 2025 proves this volatility. According to SPI Research and Deltek, the average EBITDA margin for professional services firms plummeted from 15.4% in 2023 to just 9.8% in 2024. Billable utilization followed suit, dropping to 68.9%, well below the optimal 75% threshold. This isn't just a "bad year"; it is a structural warning sign.

For a buyer, this data translates to risk. When I sit down with founders, I have to explain that their "handshake revenue"—projects won over golf or through personal networks—is worth 50 cents on the dollar. The only way to break out of the 4x-6x EBITDA trap is to prove that your revenue behaves like a product, even if you sell time.

A services firm that runs on the founder's golf-course relationships is worth four times EBITDA. One that runs on a recurring, documented system is worth fourteen. The multiple is a bet on whether the revenue survives you.

The New Math: Specialization and Recurring Revenue

The spread in professional services valuations has never been wider. In early 2025, generic consulting firms are trading in the 4.3x to 6.4x EBITDA range. However, highly specialized firms—specifically in IT consulting and digital transformation—are commanding multiples as high as 13.6x to 15.2x according to First Page Sage's 2025 Report. Why the massive delta?

The "Quality of Revenue" Premium

Buyers are paying a premium for predictability. The "Recurring Revenue" model—often achieved through managed services or long-term subscription-like contracts—drastically reduces the risk profile. Data from SPI Research indicates that High-Performing Organizations (HPOs) who leverage these models generate 31% higher annual revenue per billable consultant than their peers.

- Generic Staffing/Services: 4x - 6x EBITDA. (High churn, low differentiation.)

- Project-Based Consulting: 7x - 9x EBITDA. (Strong brand, but re-selling every year.)

- Productized/Managed Services: 12x - 15x+ EBITDA. (High NRR, predictable cash flow.)

If your firm is stuck in the "Project-Based" tier, your immediate goal is not just "more sales." It is better sales. You need to shift from "eating what you kill" to farming recurring yields.

The Action Plan: Structuring for the Exit

You cannot talk your way into a higher multiple; you have to engineer it. If you are preparing for acquisition in the next 12-24 months, you must mercilessly attack your own P&L before the Quality of Earnings (QofE) team does.

1. Fix Your Labor Multiplier

Your "Employee Cost-to-Revenue" ratio must sit between 40-60%. If it exceeds 60%, you are overstaffed or underpriced, and a buyer will discount your valuation to account for the necessary layoffs. Efficient firms generate significantly higher margins by leveraging technology, not just headcount.

2. Bridge the Gap with Structure

If your EBITDA is $5M but "lumpy," expect a buyer to offer a lower multiple on the base with an aggressive earn-out. To defend your value, present a Quality of Revenue report alongside your financials. Highlight your Net Revenue Retention (NRR) and client tenure. Show that your top 20% of clients provide predictable, expanding revenue streams.

3. The Final Verdict

Valuation is a function of confidence. A 4x firm asks the buyer to trust the founder's sales ability. A 14x firm asks the buyer to trust a proven, recurring system. Build the system.