The practical answer

- Short answer

- A data room full of "ask the founder" triggers a 25% Key Person Discount. Here's the documentation that moves a B2B tech firm from 4x EBITDA to 8x.

- Best fit

- Industry: B2B Tech. Function: Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

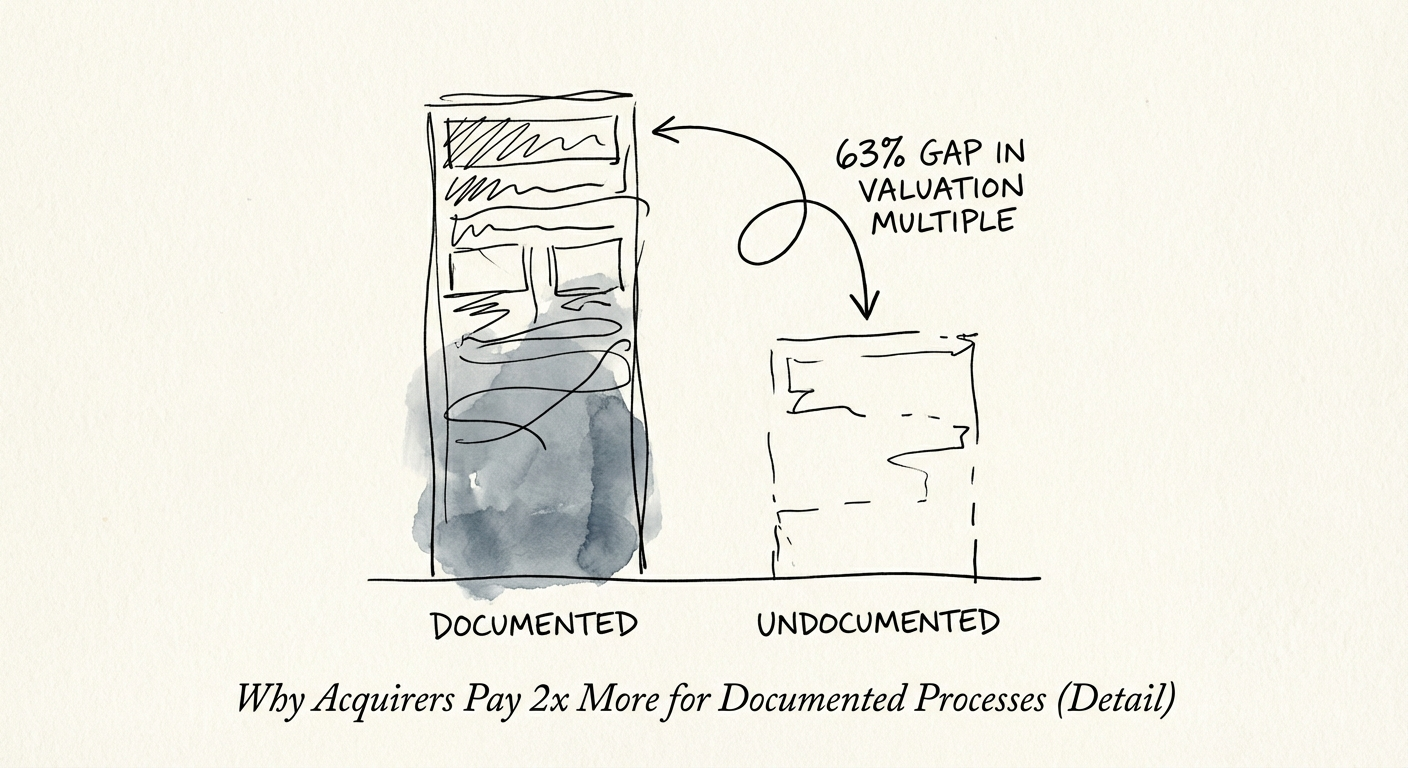

- 63% Valuation Multiple Gap (Documented vs. Undocumented)

The most expensive phrase in a data room is "ask the founder"

Picture the diligence call. A private equity associate has your VDR open and is clicking through the operations folder. Renewal process: "ask the founder." Deployment sign-off: "ask the founder." Pricing exceptions over $50K: "ask the founder." By the fourth one, they've stopped reading the document and started building a model — specifically, the model for how much they discount the offer because the business and the person are the same asset.

That discount has a name. It's the Key Person Discount, and on a founder-led B2B tech firm it runs 15% to 25% of enterprise value. Run the arithmetic on a $20M deal and the missing operations folder is a $5M line item — money that evaporates not because the business isn't good, but because the buyer can't prove it survives your absence.

You didn't build a company. You built a job that pays well.

Here's the uncomfortable reframe. When you're the $15M-revenue founder whose Slack DMs are the routing layer for every consequential decision, the cash flow isn't an asset that throws off returns — it's a wage you've negotiated with yourself. A buyer can't acquire a wage. They can only acquire it by acquiring you, which means an earnout, a retention package, and a multi-year bet that you'll stay motivated after the check clears. Every one of those is a reason to pay less today.

A buyer isn't paying for the revenue you booked last year. They're paying for the revenue that shows up after you're gone. If that number depends on you being in the building, you've priced yourself as a risk, not an asset.

Why a wiki is worth more than a quarter of good revenue

The gap isn't theoretical, and it isn't small. Empire Flippers' deal-flow data shows businesses above $1M in value — the ones that have grown past the owner and built real SOPs and a management layer — clearing roughly a 31.67x monthly multiple, while sub-$100K owner-dependent businesses trade closer to 19.38x. That's a 63% spread driven by transferability, not topline.

Carry that logic up-market and it compounds. A founder-dependent B2B tech services firm tends to clear 4-5x EBITDA. The same firm — same clients, same margins — with a documented delivery model and a team that ships without the founder in the room clears 8-10x. Nothing about the revenue changed. What changed is that the buyer can now answer "what happens if the founder walks the day after close?" with a shrug instead of a spreadsheet of risk reserves.

Documentation kills the three fears that price your deal

- Integration that needs you. Written processes drop into the acquirer's platform. Processes living in your head require keeping you on payroll to translate them — which is exactly the earnout you were trying to avoid.

- Quality that decays. Tribal knowledge degrades silently with every new hire. A documented standard makes your 50th engineer ship like your 5th — the thing a buyer is actually underwriting when they pay for "scalable."

- Diligence that stalls. Deals die in the gap between LOI and close, and a VDR that answers every operational question with "ask the founder" widens that gap. A complete SOP library closes it.

The Exit Planning Institute calls the distance between what your firm is worth today and what it could be worth the "Value Gap." For most founders, the majority of net worth is trapped inside a business they've never converted from human capital into structural capital. The conversion tool is boring. It's documentation.

What to write down first, starting Monday

You can't document a decade of accumulated judgment in a quarter, and you shouldn't try. Triage to the processes that, if they broke, would stop the cash flow.

Run the "founder fails to show up" audit this week

List the five tasks where you — or your one indispensable lieutenant — are the single point of failure. For a B2B tech firm it's almost always the same short list: pricing approval above a threshold, the deployment or release sign-off, the technical escalation no one else can resolve, the renewal conversation with your largest account. Document those five before anything else. If writing the SOP is slow, record a Loom walking through the live process and have a junior hire transcribe it into a real procedure with owners and triggers.

Get heroics off the P&L

If the quarter only closed because you personally pulled the all-nighter or made the save, that's not a process — it's a liability the buyer will eventually discover. Exit readiness means proving the machine runs without the mechanic. Define a standard of performance for sales and delivery that holds without outlier effort, and watch where it breaks when you step back.

Make documentation your team's job, not yours

Assign each functional head to document their own domain; your role is to review and reject anything below the bar. This doubles as a diagnostic. If your VP of Sales can't write down a repeatable sales process, you don't have a VP of Sales — you have your best closer with a title. Knowing that two years before diligence is worth more than learning it across the table from a sponsor. Sell them the machine that prints cash, not the operator the cash depends on.