The practical answer

- Short answer

- Why weak financial models get repriced or stall in diligence. How to build a defensible, PE-grade financial model that survives the Quality of Earnings audit.

- Best fit

- Industry: B2B Tech & Services. Function: Office of the CFO

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- 5% Target variance threshold for PE-grade forecasting discipline

The Hockey Stick is Dead. Long Live Predictability.

There is a specific moment in many stalled acquisitions where the deal loses credibility. It usually happens when the diligence team opens the "Growth Case" tab and realizes the revenue projection cannot be reconciled to current pipeline coverage, historical win rates, or delivery capacity.

We call this the "Credibility Cliff."

Founders are trained by the venture capital ecosystem to sell the dream. You build models that show "conservative" 3x growth to justify a Series B valuation. Private equity operates on a different basis. Sponsors are not just buying potential; they are buying predictability. When a model deviates from historical reality without granular operating mechanics, the buyer may discount the price, extend diligence, or question whether management understands the levers of the business.

The gap between "Founder Optimism" and "Sponsor Realism" is where deal value evaporates. If your model says you will do $20M next year, but your pipeline coverage is 2.5x and your historical win rate is 18%, you have not built a forecast; you have built a target. A PE-grade model needs to show how the revenue is earned, what assumptions drive it, and where the downside case breaks.

If you cannot trace a dollar of projected revenue back to a specific unit economic driver, it does not exist.

The Anatomy of a "PE-Grade" Model

A financial model ready for Private Equity scrutiny is not defined by its complexity, but by its defensibility. It shifts from "Top-Down" assumptions (e.g., "we will grow 20% year-over-year") to "Bottom-Up" mechanics. If you cannot trace a dollar of projected revenue back to a specific unit economic driver, it does not exist.

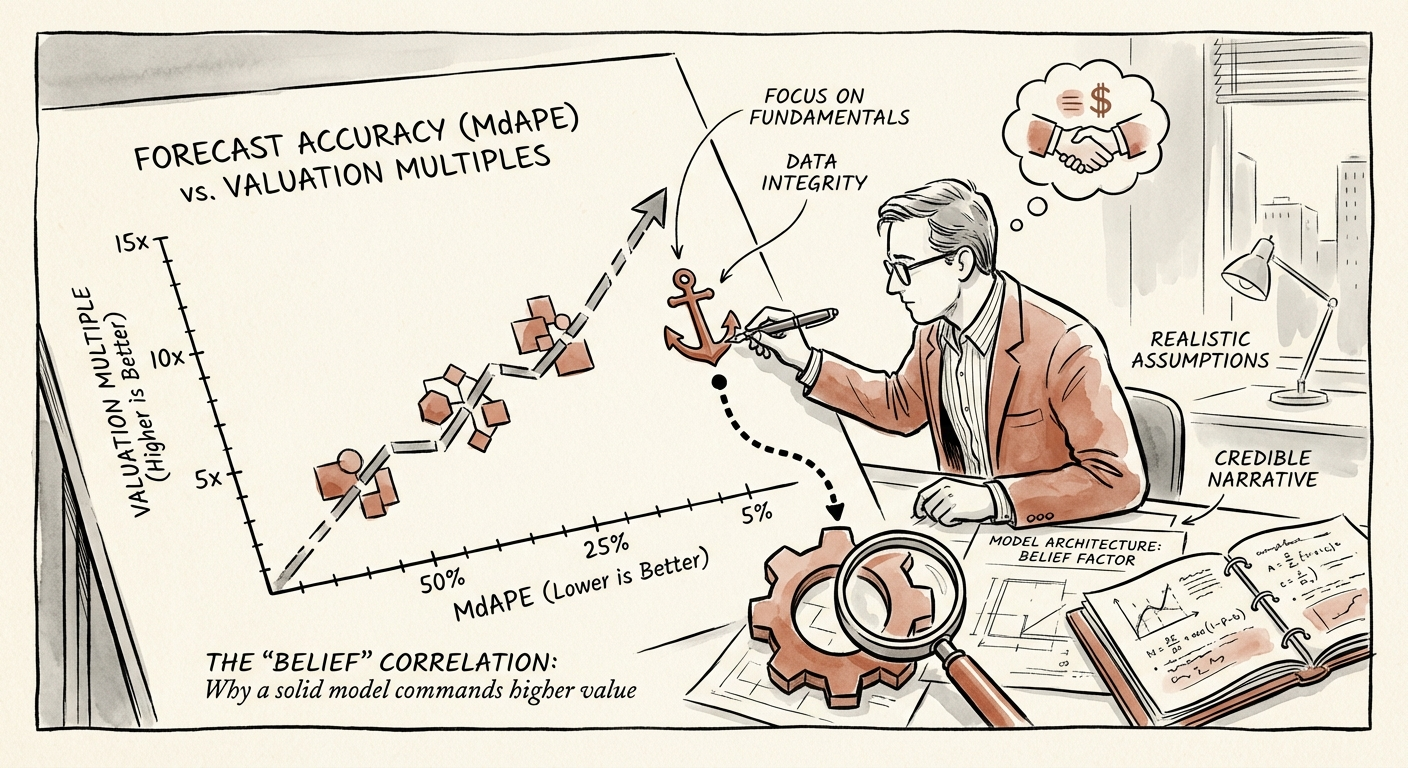

1. The 5% Accuracy Threshold

PE firms measure your forecasting ability using a metric called MdAPE (Median Absolute Percentage Error). High-performing management teams typically operate within a 4.0% to 8.8% variance range compared to actuals. If your historical forecasts consistently deviate by more than 10%, you are signaling that you do not understand the levers of your own business. To fix this, stop forecasting based on targets and start forecasting based on leading indicators like pipeline velocity and NRR.

2. The Revenue Build must be "Name-Based"

In the Lower Middle Market ($10M-$50M Revenue), generic growth assumptions are a red flag. Your model should explicitly list your top 50 accounts. Growth should be modeled based on specific upsell opportunities, contractual price uplifts, and known renewals. For new business, use a "Weighted Pipeline" approach: Opportunity Value × Stage Probability × Historical Win Rate. This is the difference between a "guess" and a "risk-adjusted projection."

3. The EBITDA Bridge & The Add-Back Trap

Founders love EBITDA add-backs. "If we hadn't hired that bad VP of Sales..." or "If we ignore the one-time server migration..." The reality is that aggressive add-backs are scrutinized heavily in 2025. Buyers are rejecting "pro forma synergies" that haven't been executed. A PE-grade model separates "Statutory EBITDA" from "Adjusted EBITDA" with a clear, line-item bridge that a Quality of Earnings (QofE) provider can audit in minutes, not days.

The 5-Day Model Scrub: Actionable Steps

Before you open your data room, you need to scrub your financial model. This is not about changing the numbers to look better; it is about making the structure auditable. Perform these three stress tests immediately:

- The Headcount Logic Test: Does your revenue growth outpace your headcount growth? If you project 50% revenue growth but only 10% headcount growth, your model implies a major spike in revenue per employee. Unless you can prove the operating leverage, buyers will challenge it. Ensure your operational expenses scale logically with revenue.

- The "Toggle" Test: A PE associate will immediately stress the model. Can they toggle "Churn" from 5% to 10% and see the cash flow impact instantly? If your model is hardcoded, it is not diligence-ready. Build dynamic sensitivity toggles for price, churn, and win rate.

- The Cash Reconciliation: Profit is opinion; cash is fact. Ensure your three-statement model actually balances. If your indirect cash flow statement does not match the change in cash on the balance sheet, trust drops quickly.

Conclusion: Valuing Certainty

In a market where capital costs are non-zero, PE firms pay a premium for certainty. A boring, accurate model that predicts 15% growth is more valuable than a chaotic model predicting 50% growth that misses its first quarter post-close. You are not just selling a company; you are selling confidence that you know how to run it.