The practical answer

- Short answer

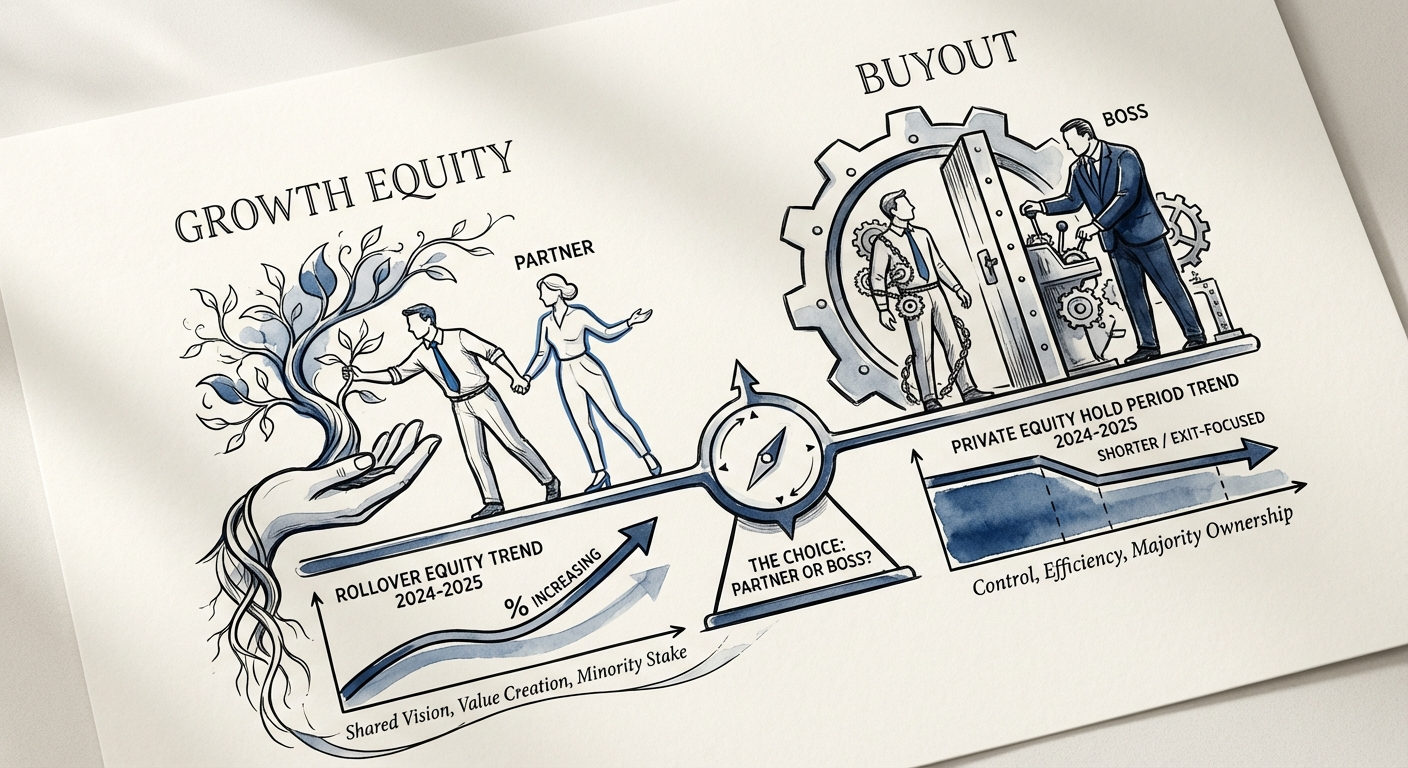

- Growth equity or buyout? The real divide is control, not check size. 2025 hold periods, the 11.7x NRR multiple, and the rollover math founders miss.

- Best fit

- Industry: B2B Tech / Services. Function: Executive Leadership

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 11.7x Median Revenue Multiple for SaaS with >120% NRR (vs 5.6x industry median)

Two term sheets, same dollar amount, opposite lives

I sat with a founder last year who had two offers on the table for his $24M ARR vertical SaaS business. Both valued the company at roughly the same number. He assumed they were interchangeable and planned to pick whichever wired faster. One was growth equity. One was a buyout. He nearly signed the buyout thinking he'd stay in the captain's chair the way he always had.

The check size told him nothing useful. What separated those two pieces of paper was a single variable he hadn't priced: who controls the board the morning after the money lands.

That is the entire decision, and most founders get it backwards. They sort by dollars. The thing that actually changes your daily life for the next half-decade is whether you keep the gavel or hand it over. When you sign, you are picking the governance model for your next 5.8 years — the current median PE hold period, down from a peak near seven. You are choosing between a partner who pulls you aside to ask "how do we grow faster?" and a controlling owner who pulls up the dashboard and asks "why is EBITDA off by 200 basis points?"

Your growth rate already chose for you

Here is the part bankers tend to soft-pedal until the LOI is signed: you don't get to pick your lane by preference. Your trailing growth rate picks it for you.

- Growth equity is fuel for a business that already works. You're compounding 30%+ a year with clean unit economics, and the money goes onto the balance sheet — more reps, more roadmap, a tuck-in acquisition. You stay CEO with majority ownership intact.

- Buyout is optimization for a business that's durable but plateauing. You're growing 10–20% with sticky revenue, and the money goes into your bank account as secondary liquidity. In exchange, the firm takes 51%+ and re-engineers the P&L on its terms.

So if you're the founder stuck at $20M ARR watching growth flatten toward the teens, telling yourself you'll only take growth-equity terms because you want to stay in control — the market disagrees with you. You're a buyout candidate wearing a growth-equity costume, and that mismatch is exactly what a clear-eyed exit readiness assessment exists to surface before a banker does it for you in front of an investment committee.

A 10x multiple with a partner who replaces you in month six is worth less than an 8x with one who helps you build the second bite. You are not pricing the business. You are choosing who signs your performance review for the next 5.8 years.

What the 2025 data actually says you're signing

Four numbers reshape this decision once you see them clearly. None of them show up on the cover slide of a pitch deck.

The strategic premium you're holding out for is mostly gone

The most expensive mistake I watch founders make is waiting for a strategic acquirer — a Salesforce, an Oracle — on the belief that strategics pay a fat premium over financial buyers. Strip out the AI-darling outliers and the gap collapses: in 2024, strategics paid roughly 9.7x revenue while PE paid 9.2x. Half a turn. If you're declining real PE offers today to chase a strategic bid that may never materialize, you're financing that fantasy with quarters of your own life.

The multiple is yours to earn, and it's set by retention

Valuation isn't a negotiation outcome; it's a scorecard you wrote before the process started. SaaS businesses carrying net revenue retention above 120% cleared a median of 11.7x revenue against a 5.6x industry median. That's not a rounding difference — it's more than double the company, decided by churn you could have fixed eighteen months ago. If your NRR sits at 95%, the honest move is to delay the process and repair retention first, because Rule of 40 performance is now table stakes, not a tiebreaker.

The rollover is where the headline number lies to you

You cannot fully cash out, and the part you keep is riskier than the part you sell. In 2024, 57% of mid-market deals required founder rollover equity, typically 12.5% to 25%. Picture the mechanics on that $24M business: you roll 20% into a minority stake in a company you no longer control. Then the firm layers on debt — often 50–70% of the purchase price. Your rolled equity sits behind that debt in the stack. Miss the growth plan, struggle to service the leverage, and your "20% upside" can settle to zero while the lenders are made whole first. The valuation headline tells you nothing about this. The capital stack tells you everything, which is why surviving your first PE partner starts with reading the debt schedule, not the offer price.

The clock is real and it's already running

That 5.8-year hold isn't a soft target. It's roughly 20 board meetings to double or triple enterprise value, and the timer starts the instant the wire clears. Growth equity gives you a longer leash on timing — but trades it for the relentless expectation that you hold 30–40% growth, every quarter, with no off-ramp.

Run the diagnostic before you call a banker

Be honest with yourself about which description fits, because the wrong door is expensive to walk back through.

Growth equity fits if you're north of 30% YoY, have a credible line to $50M+ ARR, and are constrained by cash rather than execution. You keep control — usually 60–80% ownership — but you accept negative-control provisions: the investor can block a sale, veto a budget, or kill a senior hire. And if you whiff on growth targets, many term sheets let them ratchet in structure that dilutes you hard.

Buyout fits if you're growing 10–25%, running 20%+ EBITDA (or have a clear path to it), and you're tired of the heroics it takes to keep the machine running. You get real cash up front — often 70–80% of value — plus a sophisticated partner with an M&A war chest and an integration playbook. The catch is permanent: you become an employee of the holding company, and two quarters of missed numbers can end with you fired from the company you built.

The second-bite math, run honestly

Plenty of founders choose buyout for one reason — the second bite. The pitch writes itself: sell 80% now for $40M, roll the other 20% at $10M, grow the company 3x over the hold, sell the remaining stake for $30M. On paper you out-earn the founder who held out for the perfect strategic.

It's a genuinely good plan — if you execute inside a leveraged structure, which is a different sport than running on founder instinct. Second bites are won on disciplined board reporting and a forecast the firm can underwrite, not on the gut calls that got you to $24M. The founders who get the full second bite are the ones who treat the first 90 days post-close like a new job, because it is one.

So before you optimize for the biggest number on the page, optimize for the governance you can actually live inside. A 10x with a partner who replaces you in month six is worth far less than an 8x with one who's still in your corner at the exit. Start with a clear-eyed readiness assessment, then go find the partner whose questions you can answer for the next 5.8 years.