The practical answer

- Short answer

- 73% of portfolio CEOs are replaced during the hold period. Stop relying on 'gut feel.' Use this quantitative Management Assessment Framework to de-risk your next acquisition.

- Best fit

- Industry: Private Equity. Function: Human Capital

- Operating path

- Team & Hiring → Operational Excellence → Transaction Execution Services

- Key metric

- 73% CEO Replacement Rate in PE Portcos

The $20M "Gut Feel" Mistake

You spend $150,000 on a Quality of Earnings (QoE) report to verify every dime of EBITDA. You deploy a technical specialist team to audit the codebase for IP risks. You have legal teams scrutinizing every contract clause. Yet, when it comes to the single biggest driver of ROI—the management team—most Private Equity firms still rely on a "dinner test."

You take the founder and their C-suite to a steakhouse. You check if they are articulate, if they seem passionate, and if you can "work with them." This is not due diligence; it is social gambling. And the odds are not in your favor.

According to AlixPartners' 2025 Private Equity Leadership Survey, 58% of portfolio company CEOs are replaced within two years of an acquisition. Over the full investment lifecycle, that number climbs to 73%. This churn is not just an HR headache; it is an EBITDA killer. Replacing a C-suite executive typically costs 213% of their annual salary in direct costs, but the opportunity cost is far higher. A botched leadership transition stalls value creation plans by 6 to 9 months—often the difference between a 3x and a 2x return.

The root cause is the Human Diligence Gap. While financial and legal diligence has become scientifically rigorous, human capital assessment remains dangerously subjective. Operating Partners need a "Quality of Management" (QoM) framework that is as quantitative and defensible as their QoE. We call this the Human Capital Audit.

You would never buy a company with 73% customer churn, yet firms routinely accept 73% CEO churn. Measure the management as rigorously as you measure the margin.

The 4-Pillar Diagnostic Framework

Stop asking "Do I like them?" and start asking "Can they scale?" A founder who built a company to $10M usually lacks the toolkit to scale it to $50M. This doesn't mean you fire them immediately, but you must accurately diagnose their ceiling. Use this four-pillar framework to quantify leadership capability during due diligence.

1. Strategic Elasticity (The Pivot Test)

Most founders are singular in their vision. In a PE context, where inorganic growth and margin expansion are mandated, rigidity is fatal. You need leaders who can absorb new data and change course.

- The Metric: The Kill Rate. Ask the leadership team to list the initiatives they have stopped in the last 12 months. A leadership team that cannot kill failing projects lacks the discipline for PE stewardship.

- The Drill: "Tell me about a product feature you loved that you killed because the unit economics didn't work." If they have no answer, they are emotionally attached to activity rather than outcome.

2. Execution Velocity (The Say/Do Ratio)

In the Human Diligence Gap, we often see leaders who talk a good game but fail to ship. PE firms operate on compressed timelines; you cannot afford "visionaries" who miss quarters.

- The Metric: Forecast Accuracy Variance. Look at their board decks from 18 months ago. Did they hit the numbers they projected? Did they launch the product when they said they would?

- The Benchmark: Elite management teams have a forecast accuracy of +/- 10%. If their variance is >25%, their projections are unreliable.

3. Talent Magnetism (The Follower Ratio)

A B-player CEO attracts C-player VPs. An A-player CEO brings a tribe of A-players with them. As you look to avoid the cost of mis-hires, assess the existing team's loyalty to competence rather than personality.

- The Metric: The Follower Count. How many members of the current executive team have worked with the CEO at a previous company? A high number indicates that high performers trust this leader enough to bet their careers on them twice.

4. Data Fluency (The EBITDA Test)

Many founders treat finance as a compliance function rather than a strategic lever. In a leveraged environment, this is dangerous.

- The Metric: Unit Economics Granularity. Can the CTO explain how technical debt impacts Gross Margin? Can the VP of Sales explain CAC Payback differences by channel? If only the CFO knows the numbers, you have a management team that is lacking operating visibility.

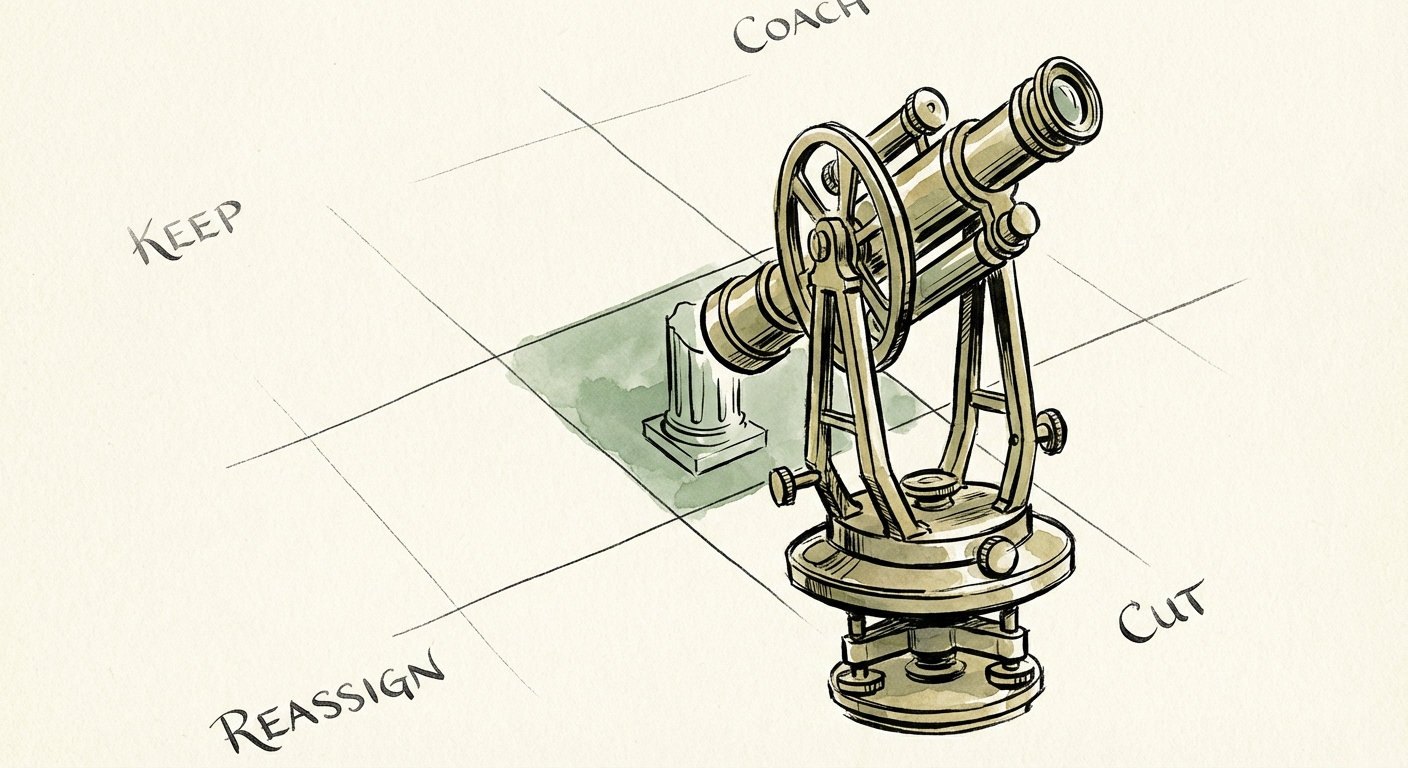

The Decision Matrix: Keep, Coach, or Cut

Once you have scored the management team across these four pillars, you must make a cold, unemotional decision. Too many Operating Partners fall into the trap of "waiting to see" during the first 100 days. This is a mistake. The highest leverage moves happen before the ink is dry on the purchase agreement.

The Quadrants of Action

- High Strategy / High Execution (The Unicorn): Keep and Incentivize. This is the rare founder-operator who can go the distance. Lock them in with a renewed equity package that aligns with your 5-year exit horizon.

- High Strategy / Low Execution (The Visionary): Coach and Supplement. This founder has the right instincts but lacks the gears. They need a heavy-hitting COO or President—someone you insert immediately to run the engine while the founder points the ship. Do not let them run operations.

- Low Strategy / High Execution (The General): Reassign. This person is an incredible VP of Operations or Sales but is not a CEO. They can execute a plan but cannot write one. Have the hard conversation about moving them into a functional role where they can win.

- Low Strategy / Low Execution (The Liability): Cut immediately. This is the most painful but necessary category. If you acquire a company with this leadership profile, you must have an Interim CEO ready to deploy on Day 1. Waiting 6 months to "give them a chance" will burn cash and destroy morale.

Conclusion: Quantify the Qualitative

The error rate in Private Equity management assessment is unacceptably high. You would never buy a company with 73% customer churn, yet firms routinely accept 73% CEO churn. By applying a rigorous, quantitative framework to the non-technical audit of your human capital, you move from "hoping they work out" to "engineering their success."

Your job as an Operating Partner is not just to buy assets; it is to ensure those assets are managed by people who can deliver the multiple. Measure the management as rigorously as you measure the margin.