The practical answer

- Short answer

- 75% of PE activity is now add-on acquisitions, yet 70% fail to capture synergies. Learn how to convert a loose collection of bolt-ons into a platform commanding an 8.2x valuation multiple.

- Best fit

- Industry: Private Equity. Function: M&A Integration

- Operating path

- Migration & Integration → Turnaround & Restructuring → Transaction Advisory Services

- Key metric

- 75% of 2024 PE Buyouts were Bolt-Ons

The Buy-and-Build Mirage

For the modern Operating Partner, the "Platform" strategy has become the default playbook. With high interest rates making mega-deals expensive and dry powder reaching record highs, Private Equity has pivoted aggressively toward add-on acquisitions. In 2024, add-ons accounted for approximately 75% of all buyout activity. The logic is seductive: buy a solid anchor asset, bolt on smaller competitors at lower multiples, and arbitrage the difference at exit.

But for many portfolios, this arbitrage is a mirage. Instead of building a cohesive "Platform" that commands a premium, firms are inadvertently building fragmented portfolios—loose confederations of acquired companies held together by little more than a consolidated financial statement. You have one logo, but four HR systems, three ERPs, and six different sales methodologies.

The market penalizes this complexity. A true Platform operates as a single, scalable machine. A fragmented portfolio operates as a holding company with bloated overhead and cross-functional friction. The difference isn't just operational headache; it is a massive valuation gap. While you are projecting a 15x exit based on combined EBITDA, the buyer's due diligence will reveal the integration debt and price you like a distress sale.

You have one logo, but four HR systems, three ERPs, and six different sales methodologies. The market penalizes this complexity... While you are projecting a 15x exit, the buyer will price you like a distress sale.

The Math: The 'Platform Premium' vs. The Synergy Trap

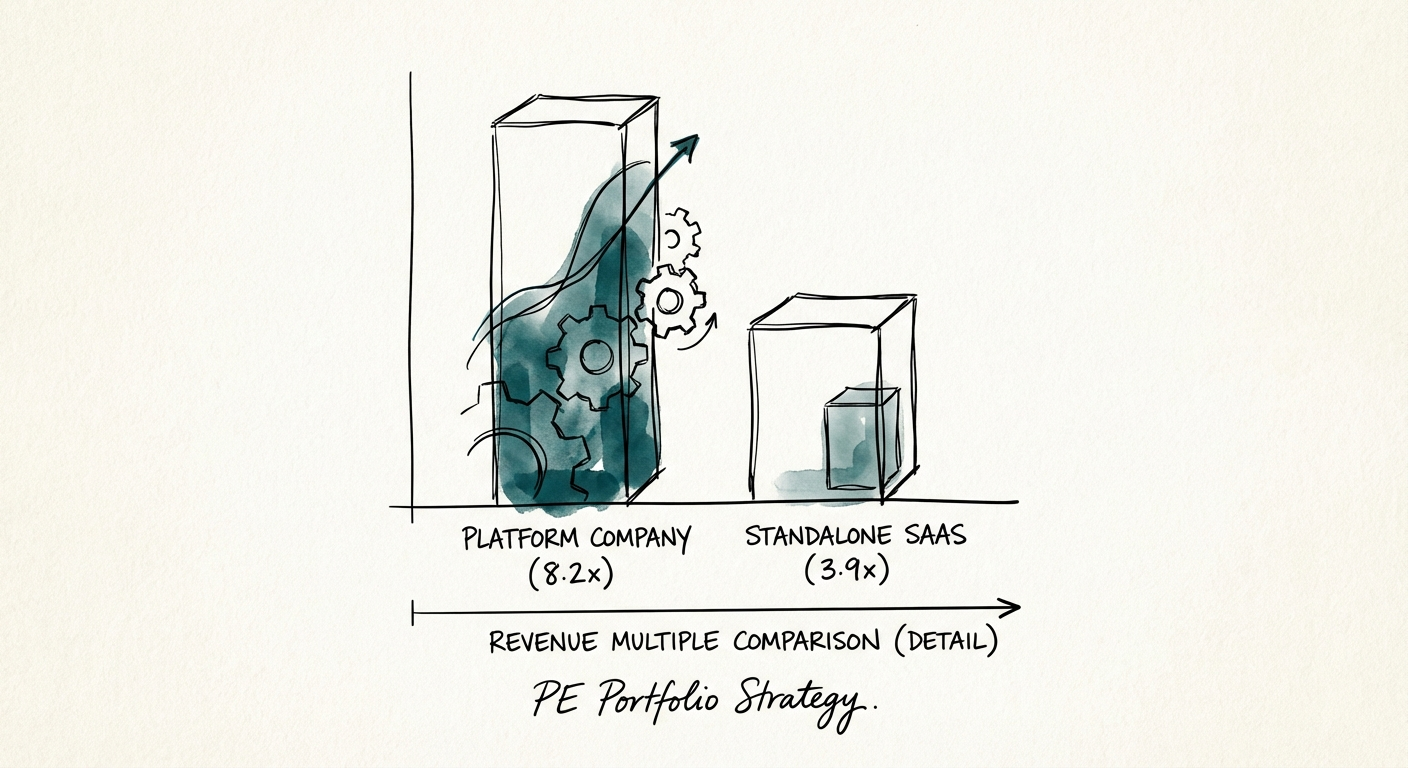

The valuation delta between a true platform and a collection of assets is not theoretical; it is quantifiable. Data from Bessemer Venture Partners highlights a significant "Platform Premium." Platform companies—those with unified data, distribution, and development ecosystems—commanded an average 8.2x Enterprise Value-to-Revenue multiple, compared to just 3.9x for standalone SaaS peers. That is a greater than 2x arbitrage available solely through effective integration.

Why Most Firms Miss the Multiple

Despite the potential upside, execution remains abysmal. Research indicates that 70% to 90% of M&A deals fail to achieve their intended value, often due to "digital underinvestment" and culture clashes. Worse, a McKinsey study found that in 42% of cases, pre-deal due diligence failed to provide any roadmap for actually capturing the synergies modeled in the deal thesis.

We see three distinct levels of integration in PE portfolios, and only Level 3 captures the Platform Premium:

- Level 1: Financial Consolidation (The Holding Co): You combine P&Ls and maybe appoint a Group CEO. Operations, tech stacks, and GTM remain siloed. Result: Zero synergy, increased overhead.

- Level 2: Back-Office Rationalization: You consolidate Finance, HR, and Legal. You might save 10% on G&A, but the core value drivers—Product and Sales—remain fragmented. Result: Marginal EBITDA improvement, no multiple expansion.

- Level 3: Operational & Technical Unification (The Platform): Single CRM, unified product roadmap, standardized delivery SOPs, and one brand voice. Result: 8.2x Valuation, scalable velocity.

The Fix: Turning Bolt-Ons into a Platform

If you are staring at a portfolio of unintegrated bolt-ons, you are bleeding value every quarter. The path to the Platform Premium requires moving from "Financial Engineering" to "Operational Engineering."

1. The 100-Day Integration Mandate

Stop treating integration as a "nice to have" that happens when operations stabilize. For every new bolt-on, launch a 100-day plan that prioritizes Post-Merger Technology Stack Consolidation. If you cannot get the new acquisition on your CRM and ERP within 6 months, you are not building a platform; you are managing a holding company.

2. Measure Integration, Not Just EBITDA

Your dashboard needs to change. Don't just track the acquired EBITDA. Track the integration velocity. Use frameworks like The Operating Partner's M&A Integration Scorecard to measure cultural alignment, system migration status, and cross-sell penetration. If cross-sell revenue isn't rising within two quarters, your "synergy" is a fiction.

3. Unify the Go-To-Market Motion

The biggest value-eroding factor in bolt-ons is maintaining separate sales teams selling separate products to the same customer base. It confuses the market and bloats CAC. Implement a unified revenue architecture immediately. For guidance on navigating this complexity, refer to The Platform Company Playbook: Integrating 4+ Acquisitions Without Chaos.

The Verdict: The market is awash in capital but short on quality assets. A true Platform is a rare asset that buyers will overpay for. A fragmented portfolio is a liability. The choice between the two is not made in the investment committee; it is made in the trenches of integration.