The practical answer

- Short answer

- Founders often confuse bookings with revenue. Discover why ASC 606 errors can inflate your ARR by 40% and reduce your exit value during due diligence.

- Best fit

- Industry: B2B SaaS. Function: Finance

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- 4-7% Annual Revenue Leakage due to Billing Errors

The $5 Million Illusion

You just closed the biggest quarter in company history. Your sales dashboard shows $5M in new bookings. The celebratory gong has been hit, the commission checks are calculated, and you are already mentally spending that growth capital on a new product line.

Then your auditor walks in.

They don't see $5M. They see $1.2M. And just like that, your "record-breaking" year looks like a flatline to the board.

This is the Revenue Recognition Trap. For founders of scaling B2B SaaS companies, the confusion between bookings (signed contracts), billings (invoices sent), and revenue (GAAP-recognized value) is not just a semantic debate—it is a valuation killer. In the early days, you ran the business on cash basis or simple spreadsheets. If a customer paid $120,000 for an annual contract, you high-fived and put $120,000 on the top line.

But as you cross the Series B threshold, that logic stops working. Enter ASC 606, the accounting standard that divorces when you get paid from when you earn the money. If you ignore it, you aren't just risking a bad audit; you are risking your exit. Data shows that 18% of term sheets are withdrawn during due diligence specifically due to financial irregularities. The number one culprit? Revenue recognition errors that artificially inflate ARR.

ASC 606 isn't just accounting nerdery; it's valuation math. We see companies claim $20M in ARR, only to have diligence restate it to $16M. At a 6x multiple, you just vaporized $24M in enterprise value.

ASC 606: The Valuation Haircut

Most founders view accounting standards as a compliance tax—something to be handed off to a controller and forgotten. This is a mistake. ASC 606 is actually valuation math. It dictates the quality and timing of the revenue you claim to have.

The "Performance Obligation" Landmine

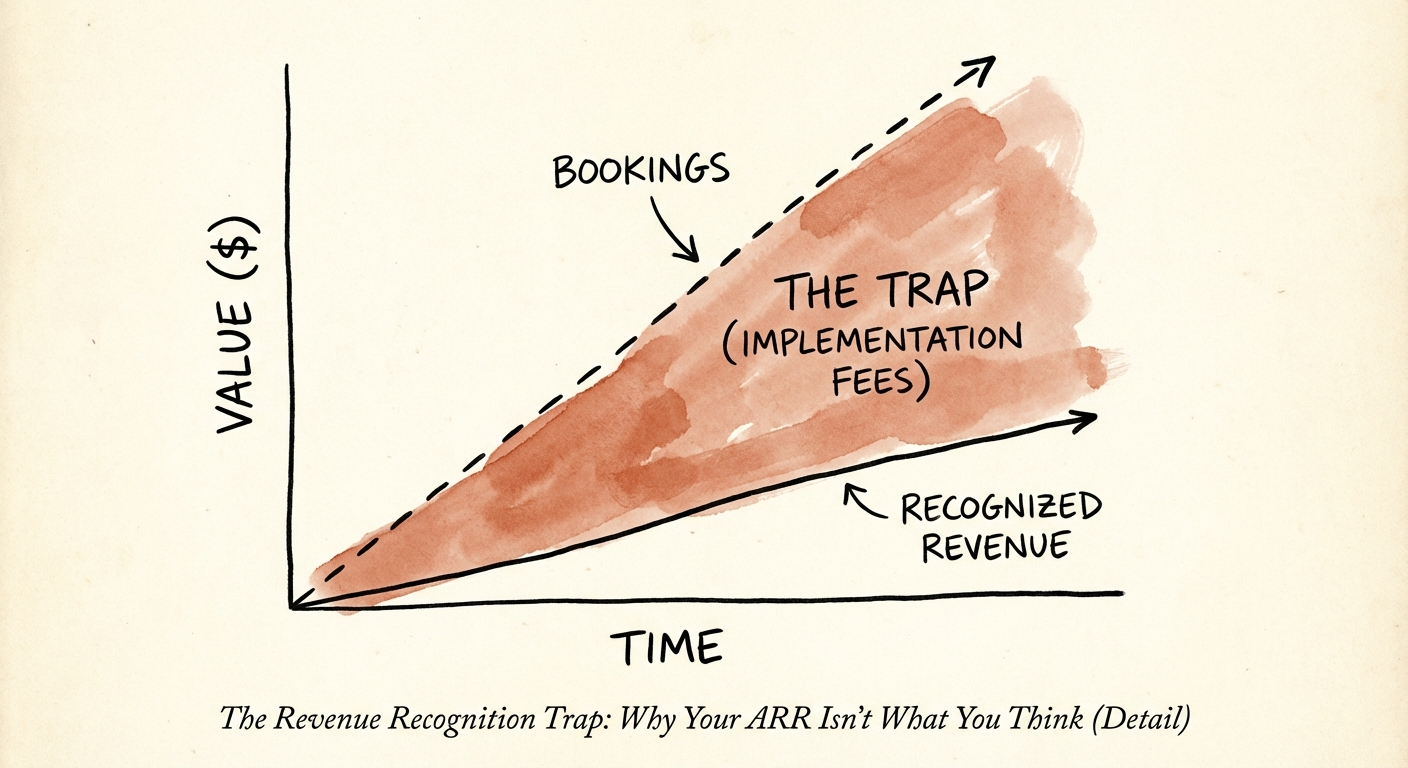

Under ASC 606, you cannot simply recognize revenue because you signed a contract. You must identify distinct "performance obligations." Here is where scaling companies get hammered:

- Implementation Fees: You charged $50k upfront for onboarding. You want to book that as revenue in Q1. ASC 606 says if that onboarding isn't a "distinct" value (i.e., the customer can't use the software without it), you must amortize that $50k over the entire lifetime of the customer (often 3-5 years). Your Q1 revenue just dropped from $50k to $2.5k.

- Bundled Support: You threw in "Gold Support" to close the deal. That support has a value. You must strip that value out of the license fee and recognize it ratably over time, even if you billed it all upfront.

- Variable Consideration: Usage-based pricing or potential refunds create "variable consideration" that compels you to estimate—and potentially constrain—revenue recognition until the uncertainty is resolved.

The impact? We see companies claim $20M in ARR, only to have a due diligence team restate it to $16M GAAP revenue. That isn't just a 20% drop in revenue; at a 6x multiple, you just vaporized $24M in enterprise value.

The Cost of Revenue Leakage

Beyond the accounting rules, sloppy contract management leads to actual cash losses. This is known as revenue leakage—money you are legally entitled to but fail to collect due to billing errors or missed renewals. Research indicates that SaaS companies lose 4-7% of revenue annually to these process gaps. In a low-margin environment, that leakage is coming directly out of your EBITDA.

For a deeper dive on how these numbers affect your board deck, read The CFO's Guide to SaaS Metrics for Board Reporting: Stop the Ambush.

The "Revenue Quality" Action Plan

You cannot wait for a Quality of Earnings (QofE) report to tell you your revenue is fake. You must audit yourself first.

1. Document Your RevRec Policy Immediately

Tribal knowledge is not an accounting policy. You need a written technical memo that defines your Standalone Selling Price (SSP) for every element you sell: licenses, implementation, support, and training. If you discount a bundle, your policy dictates how that discount is allocated across the elements. Without this document, auditors will make their own assumptions—and they will be conservative.

2. Get Out of Spreadsheets

If you are managing deferred revenue schedules in Excel at $10M+ ARR, you are negligent. One broken formula in a macro can force a financial restatement. Implement a billing system (like Maxio, Ordway, or Zuora) that natively handles ASC 606 revenue schedules. Automated systems enforce the rules you defined in step 1.

3. The "Papering" Audit

Review your last 50 contracts. Do the terms in the PDF match the terms in the billing system? We frequently find "side letters"—informal emails from sales reps promising "opt-out clauses" or "extended payment terms" that were never entered into the ERP. These side letters can trigger massive audit adjustments during an exit.

Conclusion: Certainty Commands a Premium

Buyers pay for predictability. A $20M ARR company with bulletproof, ASC 606-compliant financials is worth significantly more than a $25M ARR company with a black box of messy contracts. Don't let a technicality kill your deal. Treat your revenue recognition with the same engineering rigor you apply to your product code.