The practical answer

- Short answer

- In PPA disputes, buyers' numbers win 70% of the time. Here's exactly which EBITDA add-backs a Quality of Earnings team kills first, and how to defend yours.

- Best fit

- Industry: Private Equity. Function: Finance & Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 70% Rate at which Buyer PPA calculations are accepted over Sellers' in disputes

The Tuesday the Multiple Died

It is rarely the management meeting that kills a deal. It is rarely the indicative bid. It is a Tuesday roughly five weeks into exclusivity, when the buyer's Quality of Earnings team emails over a 60-page report and a normalized EBITDA bridge.

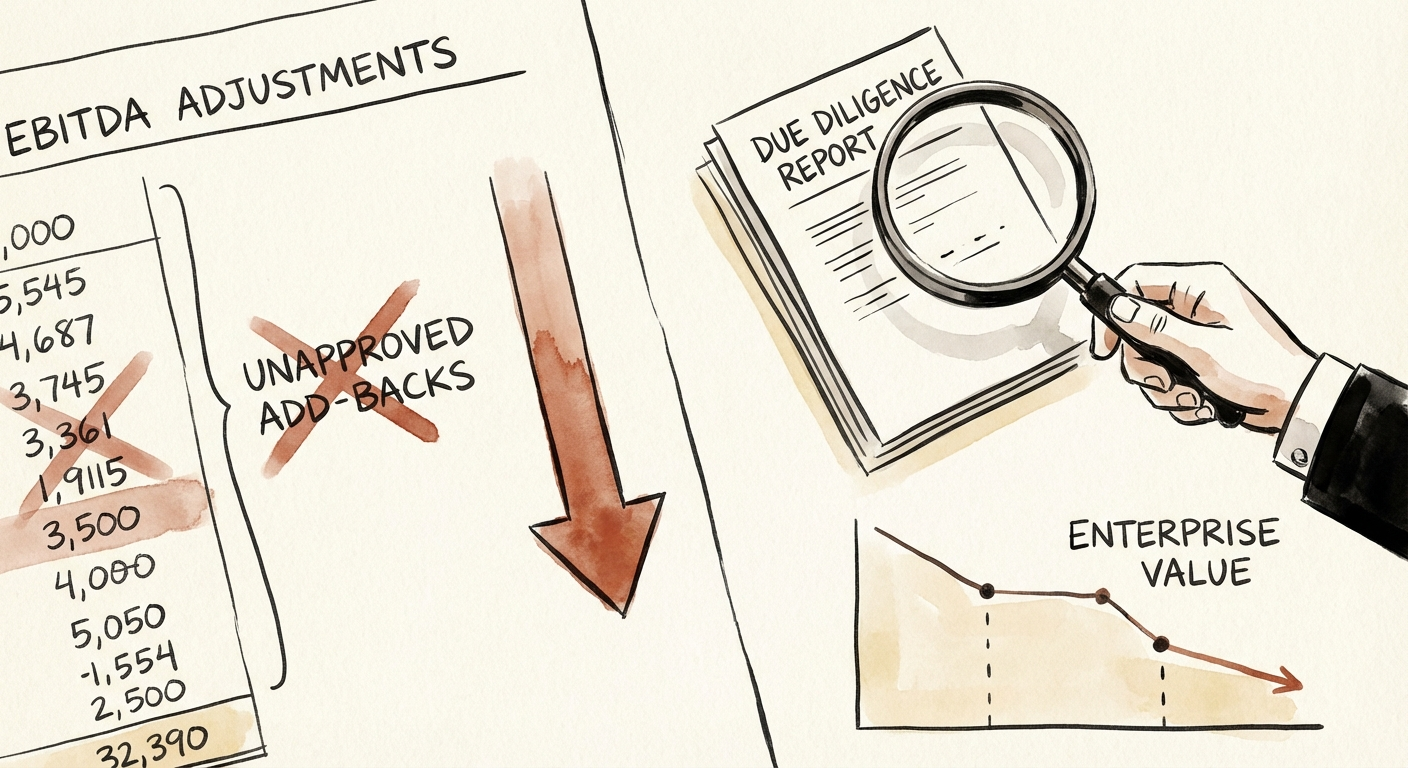

You marketed $12M of Adjusted EBITDA. The bridge restates it to $8.4M. Nobody on their side challenged your growth story or your pipeline — they just walked line by line through your add-backs and reclassified the ones they didn't believe. That $3.6M haircut isn't an accounting footnote. At the 10x you were negotiating, it just vaporized $36M of enterprise value, and it did it before lunch.

What changed is the burden of proof. The 2021 reflex — where buyers extended credit for "pro forma" savings and theoretical synergies — is gone. Diligence teams now treat every adjustment as a claim you have to substantiate with operational evidence, and the leverage in that argument runs heavily their way. SRS Acquiom's M&A Claims Insights Report found that in disputes over post-closing purchase price adjustments, the buyer's calculation prevails roughly 70% of the time. Read that as a probability, not a coin flip: when you push back on a rejected add-back, you are statistically the underdog. The only winning move is to never let the adjustment be rejectable in the first place.

Buyers pay for history, not hope. If you're claiming a pro forma cut, execute it two quarters before the LOI so it shows up in the run-rate. A clean $8M EBITDA beats a messy $10M on every dispute that matters.

The Three Add-Backs a QoE Team Kills First

Across services and tech-enabled firms preparing for a PE exit, the rejections cluster into the same three buckets. Knowing the order they get hit in tells you where to spend your prep dollars.

The "one-time" cost that shows up every year

You stripped $400K of "implementation consulting" out of OpEx as a non-recurring ERP project. The diligence team pulled the vendor ledger and found six-figure consulting fees in 2022, 2023, and 2024. The pattern is the tell. Three consecutive years of an expense isn't an event — it's a cost structure, and it gets reclassified straight back into operating expense. The fix isn't a better narrative; it's a general ledger that already separates true project costs from the consulting you quietly spend every year.

The software capitalization trap — the one most sellers never see coming

This is the add-back that's almost unique to software and tech-enabled services, and it's where the biggest single restatements happen. Say you've capitalized 40% of engineering salaries as development cost under ASC 985-20, which lifts EBITDA by pushing payroll below the line. A serious buyer pairs financial diligence with a technical review and audits the actual work: Git history, Jira tickets, sprint labels. If those "capitalized" hours were really maintenance, bug fixes, or technical-debt cleanup — work that fails the "technological feasibility" test — the capitalization gets reversed and the labor lands back in OpEx. Crowe's breakdown of the major hurdles in software-company financial diligence puts capitalized development costs near the top of the list for exactly this reason. When $2M of capitalized labor is forced back below the line, EBITDA doesn't bend — it drops in one move. We walk through the mechanics in our guide to real software EBITDA add-backs.

The synergy you described but never executed

"We'll close the Denver office for $500K." "We'll automate intake and cut five FTEs." If the lease is still active and those employees are still on payroll, the credit is denied on sight — most projected mid-market synergies never fully land post-close, and buyers price in that execution risk by refusing to pay for it up front. The flip side is the cleanest argument in the whole report: sellers who run their own sell-side QoE catch these rejections first. Middle Market Growth, citing GF Data, reports those sellers transact at roughly a 7.4x multiple versus 7.0x without one — because they fix the number or reframe the story before a buyer's analyst ever gets to swing.

What to do in the two quarters before you run a process

You don't win a QoE fight with a spreadsheet and a strong opinion. You win it by making each add-back un-rejectable before anyone looks. Three concrete moves, in priority order:

Execute the cut, then claim it. Drop pro forma savings entirely from your marketing materials. If vendor consolidation will save $500K, sign the new contracts and terminate the old ones one to two quarters before the bankers go out — so the savings sit in the trailing run-rate P&L as fact, not forecast. A buyer pays for what already happened far more readily than for what you promise it will.

Build the one-time evidence trail now. Don't let your controller bury transaction and migration costs inside "Professional Services." Stand up dedicated GL codes — "M&A / Transaction Costs," "System Migration – Non-Recurring" — so when diligence asks for detail you hand over a clean, pre-sorted ledger. Tidy books shrink the forensic discount a buyer applies the moment your data looks like it needs untangling.

Run the capitalization audit before the buyer does. If you're capitalizing development, audit it against ASC 985-20 yourself and reconcile what engineering logged as "new feature" versus what was actually maintenance. Tie the time-tracking to the Git and Jira reality. If the policy is loose, it is far better to mark your own EBITDA down $1M voluntarily than to let the buyer surface it and cut $3M — the second hit isn't just the dollars, it's the loss of trust that taxes every other number in the model. Pair this with a technical-debt audit so you're surfacing the cost on your own terms.

The whole game is leverage. Scrub your own add-backs and pre-validate the adjustments, and the diligence team has nothing left to "discover." In this market a defensible $8M beats a contested $10M, because what buyers actually pay a premium for is certainty.