The practical answer

- Short answer

- Use a 5-day operational assessment to pressure-test EBITDA quality, technical debt, team dependencies, and scalability before signing.

- Best fit

- Industry: Private Equity. Function: Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 5 Days Focused operating diligence window before LOI finalization

A 100-Page Diligence Deck Is Not Enough

If you are an Operating Partner at a PE firm in 2026, the deal funnel can move faster than your ability to vet the operating model. The market has shifted. Assets that look clean in the data room can still carry unresolved product, talent, systems, and go-to-market constraints that only appear after close.

Financial engineering alone is not enough when margin expansion depends on actually improving the business. The diligence question is no longer only, "Are the historical numbers accurate?" It is also, "Can this company execute the value creation plan we are underwriting?"

The Operating-Risk Gap

Traditional due diligence is designed for risk mitigation, not value creation. It tells you if the company is being sued, if the tax returns match the bank statements, and if the IP is registered. It does not always tell you whether engineering velocity is dependent on one architect, whether the sales forecast is based on stale opportunities, or whether the AI roadmap is backed by working product capability.

We see this pattern often: a firm acquires a software or tech-enabled services business with a convincing growth story, then discovers in the first month that technical debt, sales-process gaps, or founder dependency will consume the first year of the hold period. A focused operating assessment is meant to surface those constraints before they become post-close surprises.

You do not need another month of generic diligence. You need a concise operating readout that clarifies what has to be fixed, funded, and sequenced.

Financial diligence tells you what happened. Operational diligence tells you whether the company can execute the value creation plan after close.

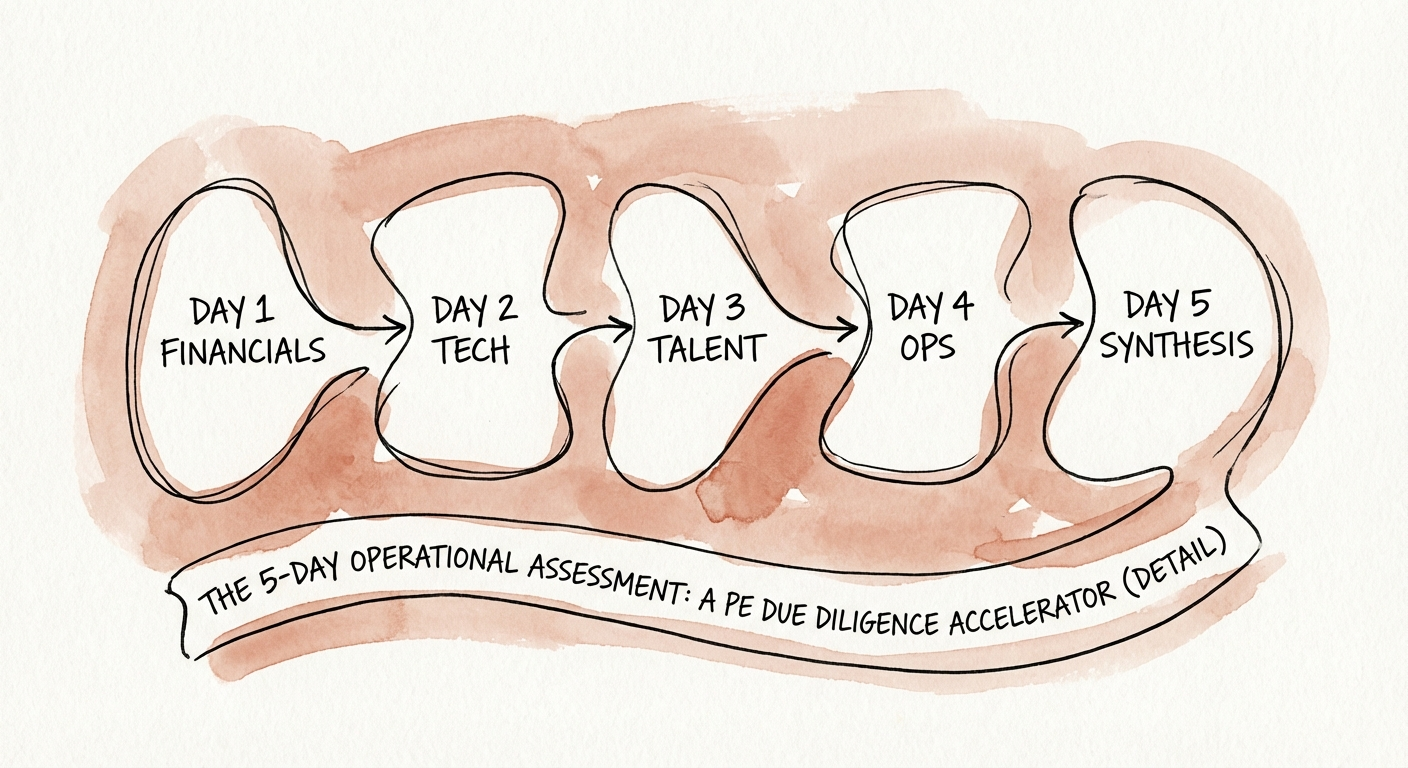

The 5-Day Operational Diagnostic Framework

At Human Renaissance, we use this framework to pressure-test the investment thesis quickly. It is not about producing a longer report; it is about identifying the operating constraints that change price, structure, timing, or the first 100 days of ownership.

This framework assumes you have data room access and key stakeholder interviews scheduled.

Day 1: Revenue Quality & EBITDA Context

Financial diligence checks the past; operational diligence checks the future. On Day 1, we look beyond the P&L and assess the quality of the revenue base.

- The Concentration Stress Test: We do not just look at the top 10 customers; we look at the relationship health of the top 3. Is the product essential, or is retention overly dependent on founder relationships?

- Pipeline Quality: We audit the verbal commits and late-stage opportunities. If you remove deals that have not moved a stage in 60 days, does the forecast still support the plan?

- The Discount Trap: Is growth being bought with unsustainable discounting?

Related Reading: The Revenue Quality Audit: What PE Firms Check Before Writing a Check

Day 2: Technical Scalability

Technical debt can materially change the first 100 days. Before a full code audit, the diligence team needs a velocity audit: how often the team ships, where release risk sits, and which systems constrain growth.

- Key-Person Dependency: If the lead architect leaves tomorrow, can the team still maintain and extend the core product?

- Deployment Frequency: If they deploy once a quarter, the operating model may not support a SaaS-style value creation plan.

- Security Debt: Are identity, backup, and incident-response controls mature enough for the target customer base?

Related Reading: How to Quantify Technical Debt in Due Diligence

Day 3: Talent and Decision Rights

We map the organization by output, not only by title. In founder-led businesses, senior titles often mask informal decision paths and unclear accountability.

- Critical Dependency Map: Which employees are carrying work that should be institutionalized? What happens if they leave after close?

- Management Span of Control: Are there 12 people reporting to the CEO? That is a bottleneck, not a scalable hierarchy.

Day 4: Operational Friction & GTM

Can this company scale 2x without adding 2x headcount? If the answer is no, the margin-expansion thesis needs to be adjusted.

- CAC Payback Reality: Is marketing spend producing qualified pipeline, or is the plan relying on broad awareness that cannot be tied to revenue?

- Sales Cycle Velocity: Is the sales cycle expanding or contracting? Longer cycles may require revised hiring, pricing, or cash assumptions.

Day 5: Synthesis & The Go/No-Go Memo

We do not produce a 100-page deck. We produce a concise memo with three sections:

- Red Lights: Findings that require price, structure, or thesis changes.

- Yellow Lights: Remediation items that belong in the 100-day plan.

- The 100-Day CapEx Requirement: The actual cash needed on Day 1 to address the highest-priority operating risks.

Execution: Speed as a Competitive Advantage

The market in 2026 rewards prepared buyers. Sellers are exhausted by slow diligence cycles that end in broad re-trading. A focused 5-day operational assessment signals that you are serious, operator-led, and specific about the risks you need to understand.

However, the real value is internal. It reduces the most common PE failure mode: the post-close discovery period.

Too many firms buy a company and spend the first two quarters figuring out what they bought. By the time they realize the technical roadmap is underfunded or the churn numbers require deeper analysis, the first year of the hold period is already slipping. The 5-day assessment helps ensure that the 100-day plan is ready before the wire hits.

The Operator's Mandate

You speak fluent EBITDA, but do you speak fluent DevOps? Do you know if the AI roadmap is real? If you cannot bridge that gap, you are underwriting assumptions you have not tested.

When you acquire a firm, you are buying an operating system. Financial diligence tells you how the company performed last year. Operational diligence tells you whether the system can support the plan you are about to fund.

Avoid the post-close surprise. Audit the operating system before you own it.

Related Reading: The PE Operator's Playbook for 100-Day Portfolio Turnarounds