The practical answer

- Short answer

- Your SaaS hit $10M because you closed every deal. Here are the 7 measurable signs that the same instinct is now capping growth — and the diagnostic to prove it.

- Best fit

- Industry: B2B SaaS. Function: Sales

- Operating path

- Founder Extraction → Operational Excellence → Interim Management

- Key metric

- 5.7 Months Avg. Sales Rep Ramp Time (2025)

The $10M wall has a tell: your reps close at half your rate

Here is the moment it usually breaks. A founder-CEO of a B2B SaaS company crosses $8M ARR, raises a Series B on the strength of a beautiful growth curve, and uses the money to hire three Account Executives so they can finally stop carrying every deal. Eighteen months later, revenue is up maybe 15%, two of the three AEs are gone, and the founder is back on the same number of closing calls they were on at $4M — except now they're also managing a VP of Sales and explaining the flat curve to a board that funded the opposite.

Nothing went wrong with the hiring. What went wrong is that the company crossed a revenue line that founder selling can't cross. The first $5-8M came from you knowing the product better than anyone alive, carrying personal credibility into every room, and bending the roadmap to win the deal in front of you. None of that is a process. It's you. And "you" does not have enough hours in the week to get a SaaS company from $10M to $30M.

The cost of finding this out late is concrete. Average B2B sales rep ramp time has stretched to 5.7 months in 2025 — up from 4.3 a few years ago — which means every rep you hire is a six-month cash bet before they return a dollar (SalesSo, "Sales Ramp-Up Statistics 2025"). Hire three on tribal knowledge and "shadow me," and you've spent a year and a seven-figure burn discovering that mimicry isn't training. There's a second bill waiting at the exit: a buyer who sees that revenue depends on the founder applies a founder-dependency discount of 30-50% to the valuation, because they're not buying a business — they're buying your calendar (Strategic Exit Advisors). The diagnostic below is how you catch it before either bill comes due.

If you are required to close every deal, you haven't built a sales team; you've built a lead generation team for yourself.

The 7 signs, ranked by how much they're costing you

Run your own numbers against each of these. If three or more land, your revenue engine is a single point of failure, and the board's growth assumptions are built on a person, not a system.

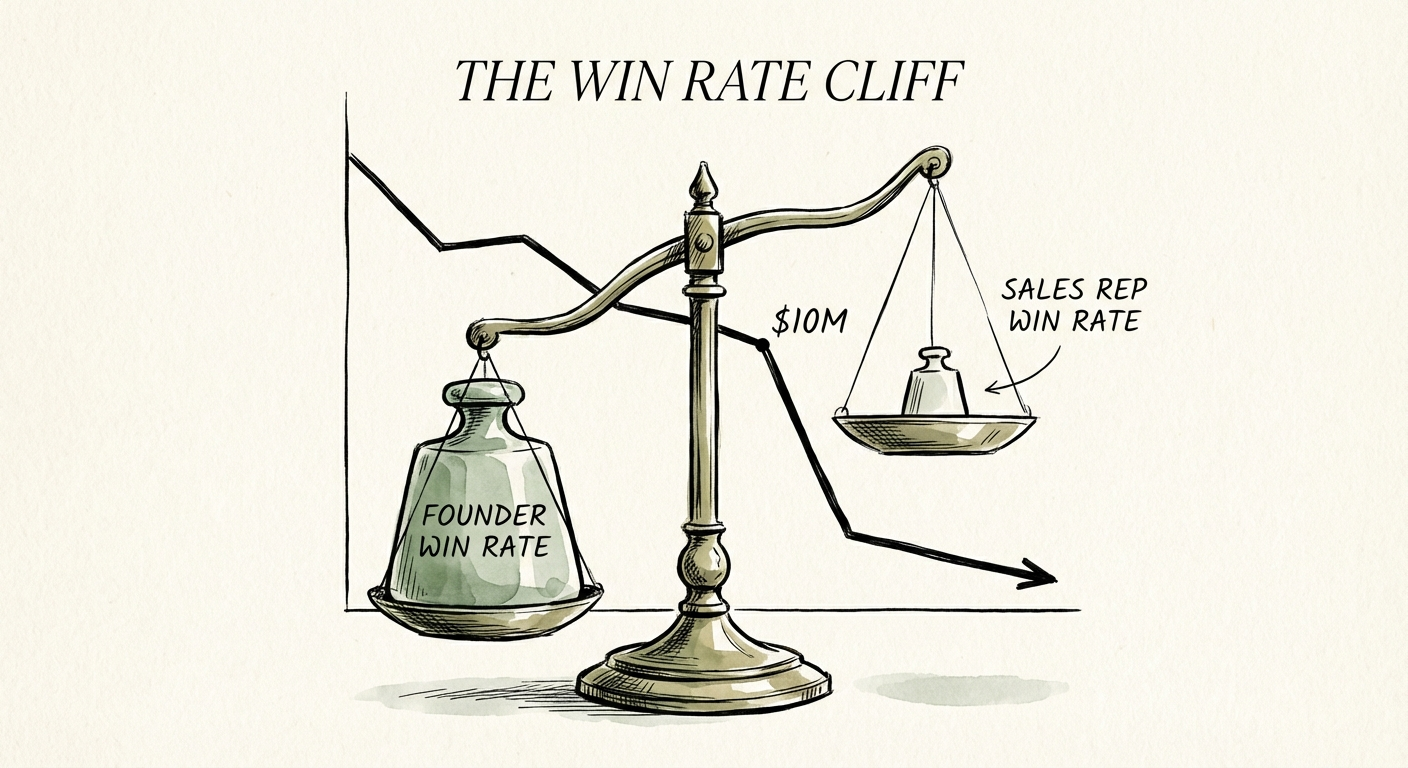

1. The win-rate cliff (the one that shows up in your CRM)

Pull two numbers: your personal close rate and your AEs' close rate on comparable deals. If you're at 40%+ and they're stuck near 15%, that gap is not a coaching problem — it's a credibility-transfer problem. Industry data shows deals with a warm, known contact close around 37% versus 19% for cold outreach (Development Corporate, "Win/Loss Rates for Enterprise SaaS"). You are the warm contact for every deal you touch. Until you've built case studies, reference customers, and structured pilots that let a rep borrow that authority, you've handed them the cold-outreach math and called it underperformance.

2. The "jump on for the last 15 minutes" close

If your VP of Sales routinely asks you to drop into the back half of a call to push it over the line, count those calls for a month. Each one is a deal the org cannot close without you. That isn't a sales team — it's a lead-gen team that hands you the close.

3. Onboarding that is "shadow me," not a curriculum

With ramp already at 5.7 months across B2B, "watch what I do on calls" doesn't shorten it — it removes the finish line entirely, because there's nothing for a rep to be measured against (SalesSo). If you can't point to a week-by-week onboarding plan with checkpoints, your new hires are guessing, and you're paying full salary for the guessing.

4. Roadmap hijacking to win one deal

You promise a feature that doesn't exist because the deal is worth $50K and you can walk over to engineering and say "build it." Your AEs can't do that. So you close the complex, custom outliers — stuffing the roadmap with bespoke debt — while your reps are left selling the standard product that actually ships. Every deal you win this way makes the next one harder for them.

5. Forecasting by feel

Ask your sales leader to forecast and listen to the verb. "I feel good about Acme" is optimism. A scalable forecast runs on exit criteria — verifiable buyer actions like "legal redlines returned" or "security review scheduled." If a deal can sit in late-stage on vibes alone, your forecast is fiction and your board planning is downstream of it.

6. Phantom pipeline

Pipeline coverage looks healthy, revenue is flat. That gap is usually "happy ears" — counting polite interest as qualified demand. Without a hard qualification bar (a known champion, a quantified pain, a confirmed budget owner, a real timeline), your pipeline is a list of conversations, not a forecast.

7. The revolving door of Sales VPs

You've hired and fired two in three years and concluded they weren't strategic enough. Here's the uncomfortable read: no sales leader can install process when the founder overrides it on the deals that matter most. You hired them to build a system and then refused to let the system govern your own calls. They didn't fail — the role was impossible.

The fix is three rules you enforce on yourself first

Founders escape this by reversing the instinct that built the company. The hard part isn't documentation or methodology — both are mechanical. The hard part is that every one of these rules constrains you before it constrains anyone on the team, and you're the one who can break them without anyone stopping you.

Rule 1: Document the why, not the what

Recording your calls is table stakes and nearly useless on its own. The asset is the annotation: at minute 14 you reframed the conversation from price to risk, and the rep needs to know why that moment and why that move. Tribal knowledge becomes a playbook only when you convert charisma into reusable logic — objection by objection, story by story.

Rule 2: One methodology, enforced in the CRM, including on you

Pick a single qualification framework and make stage progression depend on exit criteria, not optimism. No deal advances to late stage without a confirmed budget owner. The phrase that makes this real is "no exceptions, even for me" — because the day you advance your own deal without meeting the bar is the day your reps learn the bar is decorative.

Rule 3: Fire yourself from the closing call

Make your presence earned, not assumed. You join a call only if the AE submits a short brief 24 hours ahead naming exactly why you're needed and what your specific job on the call is. If they can't articulate it, you don't go — which forces them to own deal strategy instead of outsourcing it to you. Track how often you're actually needed once this rule exists; in most companies it drops fast, and that drop is the asset you're building.

Expect your blended win rate to dip for a quarter or two as the team takes over deals you used to carry. That dip is the price of converting a founder-dependent number into a transferable one — and it's the same number a future buyer will inspect first. For the full transition sequence, see the operator's guide to escaping founder-led sales, and to understand exactly how this dependency lands at exit, read the founder-dependency valuation impact. The goal isn't a smaller role for you. It's a company that grows past the limit of your week.