The practical answer

- Short answer

- Is your IT department reducing EBITDA? Check these 7 diagnostic signs backed by 2025 Gartner and McKinsey benchmarks. Learn how to pivot from cost center to value driver.

- Best fit

- Industry: B2B Tech. Function: Information Technology

- Operating path

- Technical Debt → Turnaround & Restructuring → Transaction Advisory Services

- Key metric

- 9.8% Projected Growth in 2025 Global IT Spend (Gartner)

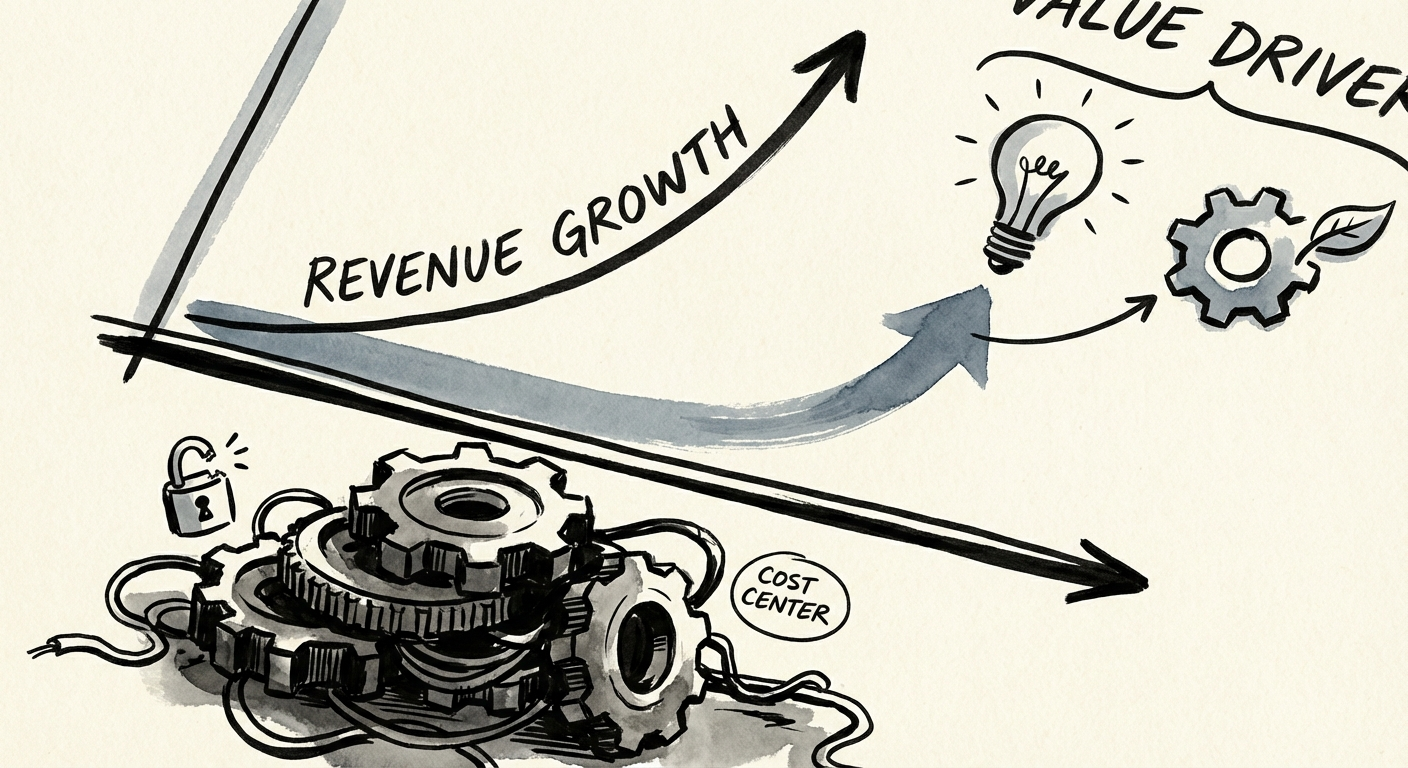

The Black Box on Your P&L

You’ve just acquired a mid-market B2B service firm. The thesis was simple: modernize the platform, improve margins, and expand the multiple. But six months in, the IT department remains a stubborn black box on your P&L.

You see the invoices—cloud costs rising, headcount increasing, licensing fees compounding—but you don’t see the output. New features are delayed. The sales team is complaining about system lag. And every time you ask for a roadmap update, you get a lecture on Kubernetes versions rather than a delivery date.

This is the classic symptom of an IT organization operating as a Cost Center rather than a Value Driver. In a cost center, IT is a utility bill—necessary, painful, and something to be minimized. In a value driver, IT is the engine of EBITDA expansion.

The distinction isn’t semantic; it’s valuation-critical. According to Gartner’s 2025 forecast, worldwide IT spending is projected to grow 9.8%, yet much of this surge is merely absorbing price hikes rather than fueling innovation. If your portfolio company falls into this trap, you aren't investing in growth; you're paying an inflation tax.

Here are the seven diagnostic signs that your IT organization is stuck in the cost center trap, and how to fix it before it drags down your exit multiple.

You don't care about Kubernetes versions; you care about why shipping a new pricing tier takes 6 months. Stop looking at IT as a utility bill.

The 7 Diagnostic Signs

1. The "Run" Ratio Is Above 70%

Every IT budget splits into "Run" (keeping the lights on) and "Grow/Transform" (innovation). In stagnant cost centers, the "Run" spend consumes 70-80% of the budget, leaving scraps for improvement. Elite organizations flip this ratio, driving maintenance costs below 50% to fund new capabilities. If you can't see this split clearly in your board deck, that's a red flag in itself.

2. Technical Debt Is an Invisible Liability

You diligenced the financials, but did you diligence the code? Forrester’s 2024 research estimates that technical debt costs the U.S. economy $2.41 trillion annually. More alarmingly, 50% of decision-makers see this debt rising to "moderate or high severity" in 2025. If your CIO cannot quantify technical debt in dollars (or days of delay), they are treating it as an engineering nuisance rather than a balance sheet liability.

3. The CIO Reports to the CFO

Reporting lines dictate priorities. When the CIO reports to the CFO, IT is managed like a line item to be cut. Deloitte benchmarks reveal that when CIOs report to Finance, they spend 60% of their budget on operations and significantly less on innovation. Value-driving CIOs typically report to the CEO, aligning technology with strategic growth rather than quarterly expense management.

4. Shadow IT Is Exploding

If Marketing is buying their own automation tools and Sales is hiring external consultants to configure the CRM, you have a trust problem. Shadow IT is a vote of no confidence in the central IT function. It signals that the business views IT as a blocker, not an enabler. While often cited as a security risk, for an Operating Partner, it’s a sign of inefficient spend and fragmented data architecture.

5. Developer Velocity Is Disconnected from Revenue

Can your CTO explain how faster code deployment translates to revenue? McKinsey’s Developer Velocity Index shows that top-quartile performers achieve 4-5x faster revenue growth and 20% higher operating margins than their peers. If your metrics stop at "uptime" and don't extend to "feature adoption" or "time-to-market," you lack the operating visibility to steer.

6. Security Is a Deal Blocker

In a cost center, security is the "Department of No." They slow down sales cycles with heavy-handed compliance questionnaires and block integrations. In a value-driving organization, security is a sales asset. Compliance (SOC 2, ISO 27001) is packaged into collateral that accelerates enterprise deals.

7. The "Green Dashboard" Illusion

Your weekly flash report shows IT SLAs are all green (99.9% uptime, tickets closed), yet revenue is down and customers are churning. This disconnection—the "watermelon effect" (green on the outside, red on the inside)—proves that IT is optimizing for its own comfort, not for business outcomes.

From Cost Center to Value Driver: The Action Plan

Recognizing these signs is step one. Fixing them requires a shift from financial engineering to operational engineering. You cannot cut your way to a high-performing IT organization; you must architect it.

The EBITDA Bridge Strategy

To flip the script, implement the "EBITDA Bridge" methodology:

- Audit the "Run" Spend: Aggressively consolidate vendors and legacy infrastructure to free up 15-20% of the budget.

- Quantify Tech Debt: Require a "debt service" line item in the budget. If we don't pay it down, what is the cost of delay?

- Align Incentives: Tie 20% of the CIO’s bonus to revenue targets or sales velocity, not just uptime.

Your goal is not just to reduce the IT line item. It is to ensure that every dollar spent on technology yields more than a dollar in enterprise value. In the current market, where multiples are compressed and buyers are scrutinized, a high-velocity, value-driving IT organization is often the difference between a mediocre exit and a market-leading return.

Stop accepting IT as a black box. Demand the same transparency and ROI rigor you expect from your sales and marketing teams. The tools exist, the data is available, and the clock on your hold period is ticking.