The practical answer

- Short answer

- 63% of buyers find material EBITDA discrepancies in diligence. Here's the tier-by-tier read on which add-backs hold under QofE and which cost you a turn of multiple.

- Best fit

- Industry: Private Equity. Function: Finance

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 63% Buyers finding material financial discrepancies in 2025 diligence

The retrade doesn't start with the number. It starts when the buyer stops believing you.

Picture the call you don't want to be on. Forty days into exclusivity, the buyer's Quality of Earnings provider sends over their "bridge" — the walk from your Adjusted EBITDA down to theirs. Your management number was $8.2M. Theirs is $7.1M. And the worst part isn't the $1.1M gap. It's the three lines in the schedule where the QofE team wrote "unsupported," because every other add-back you presented is now suspect by association. That is the moment a clean process turns into a 90-day war over price.

If you're an operating partner taking a portfolio company to market in 2026, the "Adjusted EBITDA" game you remember from 2021 is gone. Burying recurring operating costs under "one-time transformation expense" doesn't survive contact with a modern diligence team. Buyers got burned on the valuations of 2021 and 2022, and they've turned QofE from a confirmation exercise into a hunt. They are not just checking your math. They are looking for a defensible reason to pay less.

The arithmetic is what makes it dangerous. When a QofE provider strikes an add-back, the buyer doesn't subtract the dollars — they subtract the dollars times the multiple. A $200k add-back that gets cut at a 12x multiple is a $2.4M reduction in enterprise value. Recent 2025 analysis found that 63% of buyers discovered material financial discrepancies during diligence that weren't disclosed in the initial materials. The gap between "management adjusted" and "buyer adjusted" is exactly where the equity value you underwrote leaks out — and most of it leaks because someone built the schedule for a banker's pitch instead of a forensic accountant's red pen.

A $200k add-back that fails diligence at a 12x multiple isn't a $200k problem. It's a $2.4M hole in enterprise value, and the buyer will widen it once they stop trusting the rest of the schedule.

Read every add-back the way a QofE analyst will

The useful test isn't "is this a real cost savings." It's "can I hand the buyer a document that closes the question before they ask it." Sort your last twelve months of adjustments into three buckets, and be honest about which pile each one lands in. When we run a revenue quality audit ahead of a sale, this is the first sort we make.

Green — accepted, but still verified

These survive almost every time, provided the paper exists. Owner discretionary expenses — the leased car, the country-club membership, the family travel on the company card — come out cleanly, but only if you can prove the cost actually disappears post-close. One-time professional fees (a non-recurring legal settlement, the M&A advisory bill) are fine unless they're attached to ongoing litigation or routine compliance. Severance from a specific reduction-in-force is standard; severance that's really an annual pruning of the bottom of the sales roster is not. The condition is the whole game: a green add-back with no invoice behind it turns yellow the second a QofE analyst asks for support.

Yellow — defensible only with a hard data bridge

These get scrutiny, and they live or die on documentation. A pro forma synergy ("we put in the new ERP in Q4, so we're adding back the inefficiency of Q1 through Q3") reads to a buyer as your execution risk, not their economic fact. A new-hire ramp add-back — claiming the revenue a rep "would have" booked at full productivity — gets slashed unless you have historical ramp curves proving the number. An inventory write-down billed as a "one-time clean-up" stops being one-time the moment the buyer sees you took the same charge two years ago; then it's just a recurring cost of goods sold wearing a costume. The way to move a yellow into the green pile is to replace the narrative with arithmetic: pre- and post-implementation labor cost, a dated ramp model, an actual invoice.

Red — the ones that cost you the rest of the schedule

These don't just get cut. They tell the buyer your numbers were built to persuade rather than to be true, and they reprice everything downstream. Adding back the losses of an underperforming location you haven't closed yet. Claiming a weak quarter doesn't count because the CEO was distracted by a lawsuit. Adding back the profit you'd have earned if you'd hired that VP of Engineering sooner — phantom EBITDA on a role no one ever filled. Each of these is a tell, and a sharp diligence team will use one red flag as license to challenge ten green ones.

What to do in the 90 days before you go to market

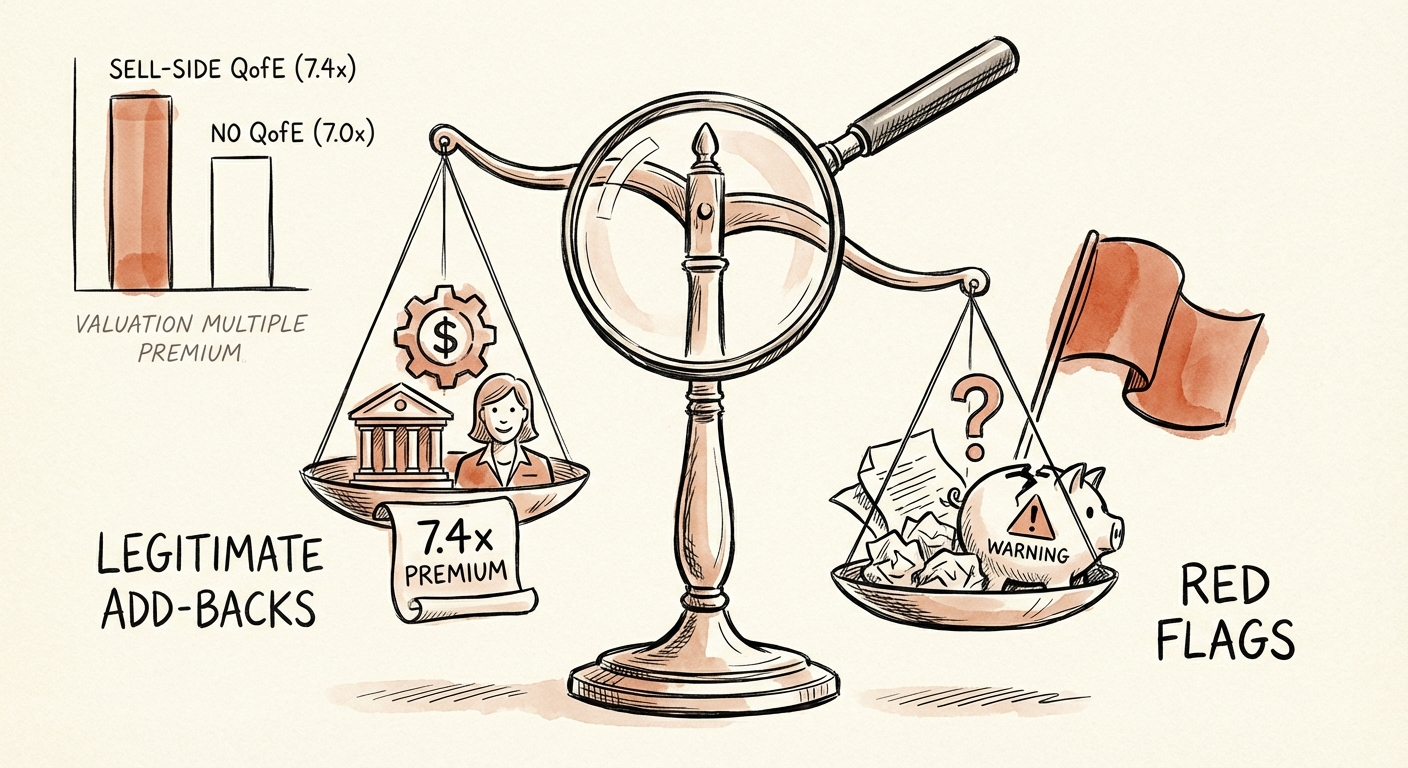

The strongest defense against price chipping is to do the buyer's work first. Sellers who commission a sell-side Quality of Earnings report have been clearing an average multiple of 7.4x against 7.0x for those who don't — a 0.4x turn of EBITDA earned purely by removing the surprises before the buyer can find them and use them as leverage. On a company doing $7M of EBITDA, that turn is worth roughly $2.8M, and it shows up in the deal dynamics Bain has been tracking across the current cycle: prepared sellers face shorter diligence and fewer retrades.

Three concrete moves before the banker ever sees the schedule:

- Audit the LTM adjustments yourself. Walk every add-back in the trailing twelve months. If one rests on a story instead of an invoice, pull it now — don't make a QofE analyst pull it for you in front of the buyer.

- Turn soft into hard. Take your "technology improvement" or "process efficiency" add-backs and stand them up with before-and-after labor cost or headcount data. An add-back you can prove with two payroll reports survives. One you can only narrate does not.

- Pre-kill the reds. If a toxic add-back is sitting on the books, remove it before anyone outside the building sees it. A cleaner, lower starting EBITDA beats an inflated one that gets shredded — because the shredding is what poisons the trust on the rest of the bridge.

Your credibility is an asset class. When a buyer trusts your numbers, they look for reasons to close. When they find a phantom add-back, they look for reasons to walk — or to walk the price down. Don't hand them the ammunition. Build the schedule a forensic accountant would sign, and the multiple you underwrote is the multiple you keep.