The practical answer

- Short answer

- A $2M-EBITDA tech firm exits for $10M or $24M depending on one thing: whether its monthly revenue is a managed service or subscription labor. Here's the line.

- Best fit

- Industry: Tech Services. Function: Finance

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- 9.8% Avg PS EBITDA (2025)

Two firms, same revenue, a $14M difference in the check

Picture two tech-services founders sitting across from the same private equity buyer. Both run firms doing roughly $2M in EBITDA. Both put "recurring revenue" at the top of the deck. One walks out with a term sheet around $24M. The other gets $10M, a longer earnout, and a diligence process that picks apart every "monthly" invoice line by line.

The difference wasn't the pitch. It was the P&L underneath it. In 2025, buyers drew the line hard: true managed-service providers with high-quality recurring revenue traded at roughly 8x to 12x EBITDA, while project-based professional-services firms struggled to clear 4x to 6x (2025 Business Valuation Multiples by Industry Guide). For a $2M-EBITDA business, that spread is the entire retirement plan.

The tell: is it a managed service, or subscription labor?

Here's the trap I watch founders fall into. They move a client from a project SOW onto a $12K/month retainer, see the revenue land on the same date every month, and start calling themselves an MSP. But ask one question: what does that $12K actually buy? If the answer is "about 80 hours of my team doing whatever the client needs this month," you haven't built a managed service. You've built subscription labor — project economics wearing a subscription costume.

The math gives it away. With subscription labor, doubling revenue means roughly doubling headcount, because the product is still hours. A real managed service breaks that link. The same compliance-monitoring stack or automated patch routine that covers 100 endpoints covers 10,000 with marginal extra cost. One firm's growth curve bends; the other's stays a straight 45-degree line that no buyer will pay a premium for. If you're stuck at $15M in revenue wondering why your "recurring" line isn't pulling a premium multiple, this is almost always why.

A buyer will pay you for revenue that survives you leaving. The moment your monthly fee is just a bucket of hours, it walks out the door every night with your engineers — and the multiple goes with it.

The numbers buyers are actually staring at in 2025

The multiple gap isn't a sentiment thing — it's downstream of two margin profiles that have pulled apart over the last few years. If you want to understand the valuation, follow the unit economics.

Margin: one model is capped by a calendar, the other isn't

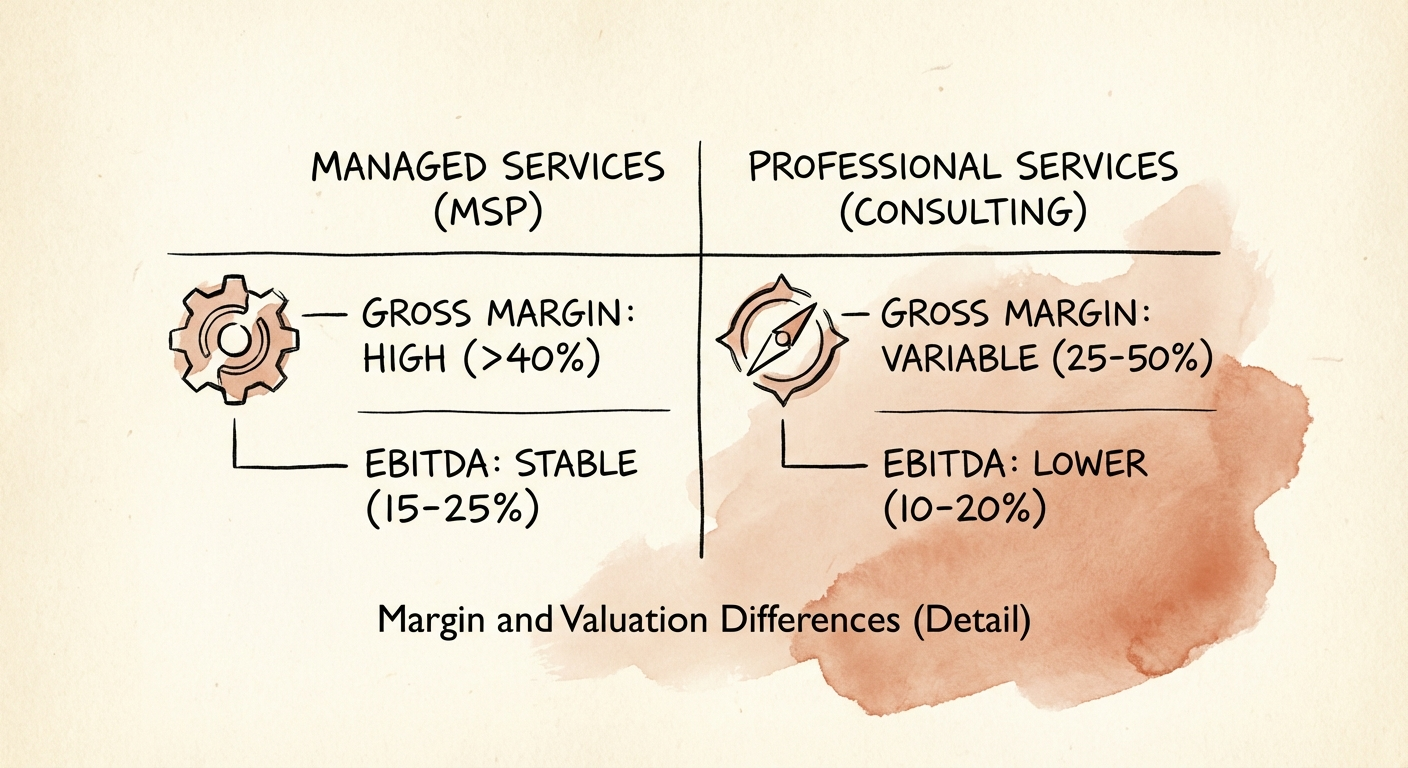

Best-in-class MSP service lines run gross margins of roughly 45–55%. Average professional-services project margins sit closer to 30–35%. The ceiling on the PS number is physics: a billable consultant has 2,080 hours in a year and realistically books maybe three-quarters of them. You cannot margin your way past a human's calendar. An MSP's automation has no such ceiling — which is the entire structural reason these firms separate so sharply in profitability.

The 2025 EBITDA story is genuinely ugly for PS

The number that should stop any consultancy founder cold: average professional-services EBITDA fell to 9.8% — a five-year low — while top-tier MSPs held adjusted EBITDA above 19%. Utilization slid to 68.9% as labor costs climbed and projects got slower to land (Deltek / SPI Research 2025 Professional Services Maturity Benchmark). As the Service Leadership Index 2025 report put it, the top-quartile solution provider earns about 2.5x the bottom-line profit of the median peer — and that 2.5x flows straight into cash flow and enterprise value.

Where the multiple actually lands

- Pure-play MSP (>70% recurring): ~10x–12x EBITDA

- Hybrid (roughly 50/50 mix): ~6x–8x EBITDA

- Project consultancy (<20% recurring): ~4x–5x EBITDA

One nuance most founders miss: buyers price the quality of recurring revenue, not just the percentage. A $20M firm split between $10M of project work and $10M of high-touch, low-margin "retainers" will get priced toward the PS multiple, not the MSP one. A buyer's job is to find cash flow that doesn't depend on your best people staying late, and they're very good at sniffing out "recurring" revenue that's really just labor on a payment plan. You can verify this yourself against role-level utilization benchmarks — high recurring revenue with utilization stuck in the high 60s is the signature of subscription labor.

How to engineer the mix before you go to market

You can't declare yourself an MSP the quarter before a sale and expect the multiple to follow. But you can deliberately re-shape the revenue mix so the P&L reads like the business buyers pay 11x for. Three moves, in order — and start now, because every quarter of clean recurring revenue you can show in diligence is worth real dollars.

1. Pick the one thing and make it boring

Stop selling capability ("we do cloud, security, and integration"). Pick the single problem you solve repeatedly — say, broken cloud migrations, or continuous compliance for a regulated vertical — and document it until it's a rigid SOP a new hire could run. If it's written down, it's transferable; if it's transferable, it scales; if it scales, it earns the MSP margin. The goal is to make your best work the least heroic thing you do.

2. Sell the outcome, not the hours

Rewrite the contracts. "20 hours of support a month" becomes "99.9% uptime guarantee" or "continuous compliance monitoring with a 4-hour remediation SLA." The instant the fee stops tracking hours worked, you've flipped the incentive: every hour you don't spend hitting the outcome becomes margin instead of a write-down. This is the single change that turns a 30% project margin into a 50% service margin over time.

3. Run the 3:1 mix rule on every salesperson

Give the team a hard ratio: for every $3 of project revenue booked, land $1 of genuine recurring revenue. Project work is fine — it throws off cash and funds the transition — but it builds almost no enterprise value, so don't let reps live on it because it closes faster. Track the recurring ratio on the same dashboard as bookings.

The decision you're actually making

The market has told you precisely what it rewards: systems, predictability, and leverage — not late nights, not infinite customization, not your personal heroics. You're allowed to run a great professional-services firm and enjoy the cash it spins off. Just don't take that firm to a buyer expecting an MSP check. If you want the 11x outcome, you have to build the 11x business first — and the work starts with the next contract you write, not the year you decide to sell. For how this maps to a full exit-readiness picture, see our professional-services valuation guide.