The practical answer

- Short answer

- A Series B founder reported $12M ARR. Diligence found $9.4M. Here is how SaaS revenue gets mislabeled and the 90-day fix before your next raise.

- Best fit

- Industry: B2B SaaS. Function: Finance

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- 31% Valuation premium for SaaS firms with audit-ready financial data

A $12M dashboard, dead in 48 hours

A Series B SaaS founder I worked with — details anonymized — walked into a $40M raise with a clean-looking story: $12M ARR, 80% year-over-year growth, a logo wall that made you want to sign the term sheet on the spot. By any narrative standard, money should have been chasing her.

The deal collapsed two days after the data room opened. Not because the company was bad. Because the $12M wasn't $12M.

Once we reconciled the contracts to the billing system, the headline broke into three piles: roughly $9.4M of signed, live, contractually committed subscriptions; $1.6M of "verbal commitments" from friendly pilots that had no order form; and about $1M of one-time implementation fees that had been smeared across twelve months to look recurring. Her gross churn, reported at 4%, was closer to 14% once you stopped letting the verbal-pilot revenue quietly backfill the accounts that had actually left.

Here is the part founders miss: the investors didn't pass because $9.4M is smaller than $12M. They'd have happily funded a clean $9.4M company growing fast. They passed because the CEO's single most important number was overstated by nearly 28% and she didn't know it. If the ARR figure shifts that much when a stranger reads it for an hour, the buyer now has to re-audit the pipeline, the churn math, the cohort retention, everything. You didn't lose a revenue argument. You lost the presumption that your numbers are real.

Why "bookings as revenue" stops being cute past $10M

At seed and Series A, investors forgive a little hand-waving — calling a signed contract "revenue" the day the ink dries, counting an annual prepay as instant ARR. The diligence is light and the bet is on the founder. Cross $10M ARR and that same shorthand reads as a control gap, not enthusiasm.

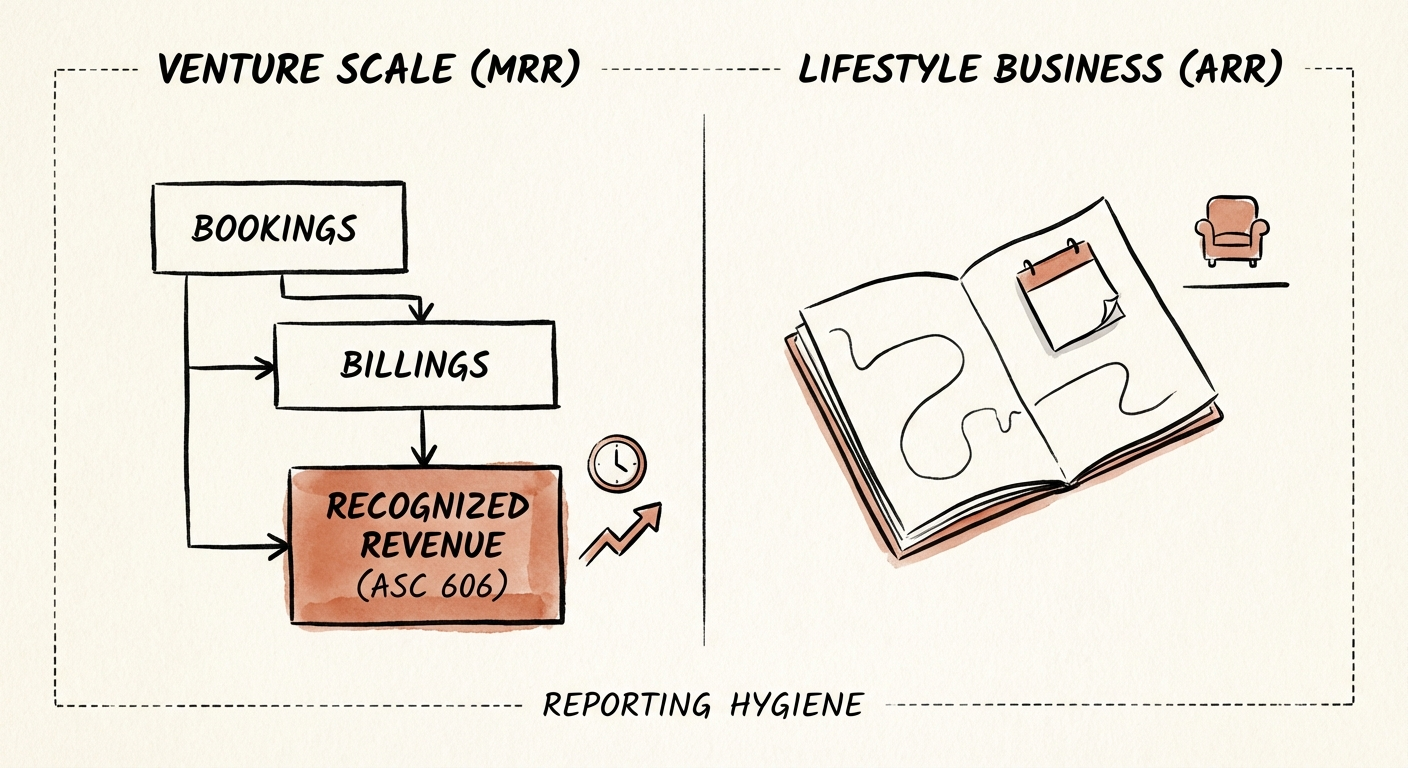

MRR versus ARR is not a multiply-by-twelve problem. MRR is the recurring revenue you are actually delivering this month; ARR is that monthly run-rate annualized — not the sum of every contract you've ever signed. The real damage happens one rung lower, when bookings (a signed contract) get treated as recurring revenue (a live, delivered subscription). A $200K deal signed in January with a March go-live is a January booking and zero January MRR. Report it as ARR and your run-rate looks healthy while your cash does the opposite.

An investor isn't discounting your revenue. They're discounting your ability to count. If the ARR number moves when a stranger reads it for an hour, every other number in the deck is now suspect too.

Three buckets a buyer will sort your revenue into anyway

You can either sort your revenue by quality before the raise, or let a diligence team do it for you and re-trade the price when they're done. Same buckets, very different outcomes. Here's how a PE operating partner or a sharp Series C lead actually reads a SaaS revenue base.

Bucket 1 — Live recurring revenue (the only thing in your headline ARR)

This number earns its place when all three are true: a signed MSA and order form (not an email, not a "we're good for it"), a recurring structure (auto-renewal or multi-year term), and live status — the customer has the environment and is being billed. Sign in January, go live in March, and you carry a booking for two months and recognize MRR starting in March. Nothing fuzzier than that belongs above the fold.

Bucket 2 — Committed-but-not-live (CARR), reported on its own line

Committed ARR — signed contracts that haven't gone live — is a legitimate sales-velocity signal. It becomes poison the moment it's blended into recognized ARR. The trap is implementation drag: a $200K deal stuck six months in onboarding keeps your CARR-inflated "ARR" flat while your burn climbs against revenue you can't yet recognize. Implementation slippage is the most common way ASC 606 revenue recognition quietly diverges from the slide. Show CARR as its own line, with an aging schedule, or don't show it at all.

Bucket 3 — Revenue wearing a recurring costume

Three things masquerade as ARR and shouldn't. Implementation and setup fees — non-recurring even if you amortize them across a year. Pilot revenue with a 90-day out clause — that's an option, not a subscription, until it auto-converts. And usage overages with no floor — variable revenue, not recurring, unless there's a take-or-pay minimum underneath it.

Then there's the mirror-image error on the cost side. Bury your Customer Success team in sales and marketing OpEx when they're really doing onboarding and support, and you've inflated gross margin on paper. FASB's ASC 606 governs how you recognize the revenue; basic cost classification governs whether your margin is honest. CSMs running implementation and support are cost of goods sold, full stop. A buyer finds that misclassification in the first margin bridge and re-prices to your true gross margin — which is exactly the kind of forensic cleanup that erases premiums. PitchBook's SaaS benchmarking ties the gap to roughly a 31% valuation premium for companies with audit-ready, GAAP-aligned books, because the acquirer doesn't have to budget for the cleanup themselves. Venura's work on the hidden cost of unreliable financial data lands in the same place from the other direction: messy metrics get discounted 20–40% to cover the uncertainty.

The 90-day move from founder math to CFO math

You don't need a finance org to fix this. You need three artifacts in place before your next board meeting.

Build the revenue waterfall. Retire the single top-line number. Bridge from bookings to recognized revenue every month: new bookings (ACV signed) → minus value still stuck in implementation → plus expansion and upsell on live accounts → minus churn and contraction, dated to the day service actually stops, not the day the cancellation email arrives → equals the MRR/ARR run-rate as it stands today. The day you count churn lets you fudge a quarter; the day service stops is the only one a buyer will accept.

Get revenue recognition out of the spreadsheet. If ASC 606 lives in a tab someone updates by hand, you've outgrown it and the fat-finger errors are already in your board deck. A billing engine — Chargebee, Maxio, Ordway, whichever fits — forces explicit start dates, end dates, and recognition schedules, which is most of the battle. This is the difference between numbers a board questions and numbers a board stops re-litigating.

Run the cash-vs-ARR variance test weekly. If your ARR implies $1M/month of collections and the bank account grows by $800K, there's a $200K leak every month — either collections drag (a DSO problem) or revenue on the slide that isn't real (a reporting problem). Put that single variance line on your weekly flash report and you'll find the leak before a diligence team turns it into a re-trade.

When you raise a Series C or run an exit, you're not selling software — you're selling the predictability of a cash machine. If the gauges read wrong, nobody buys the factory at full price. The fix isn't expensive. It's three artifacts and the discipline to date things honestly. Do it now, when it costs you a quarter of cleanup, instead of in the data room, when it costs you 20–40% of the price.