The practical answer

- Short answer

- Post-acquisition attrition benchmarks for PE operators: what turnover is normal, what becomes dangerous, and which roles put deal value at risk.

- Best fit

- Industry: Cross-Industry. Function: Human Capital

- Operating path

- Team & Hiring → Operational Excellence → Transaction Execution Services

- Key metric

- 47% of key employees leave within 12 months of an acquisition

The "Synergy" Spreadsheet vs. Reality

You have the model built. You’ve calculated the EBITDA expansion based on cross-selling into the acquired customer base and rationalizing back-office overlap. The investment committee signed off on a thesis that relies heavily on the target company’s engineering team shipping the next version of the platform by Q3.

Then the resignations start.

It’s not just the underperformers you planned to exit. It’s the VP of Engineering who holds the institutional knowledge of the legacy code. It’s the top two enterprise sales reps who control 40% of the revenue pipeline. Suddenly, your 100-day plan shifts from "value creation" to "triage."

This isn’t bad luck; it’s a statistical probability that most PE firms chronically underestimate. Data from MIT Sloan indicates that 33% of acquired workers leave within the first year of an acquisition. That is more than double the standard voluntary turnover rate of ~13% seen in the broader U.S. labor market for 2024-2025.

Defining "Dangerous" Attrition

Operating Partners often console themselves with the idea that turnover is natural during integration. "We’re shaking things up," they say. "The weak players are opting out." This is dangerous complacency.

There are two types of post-acquisition attrition:

- Structural Attrition (Normal): 10-15% turnover resulting from redundant roles (e.g., duplicate Finance/HR functions) or low performers who can’t adapt to the new pace. This is modeled in your deal costs.

- Regrettable Attrition (Dangerous): The unplanned exit of value-drivers—developers, rainmakers, and operational leaders. EY data suggests that 47% of key employees leave within 12 months of a transaction.

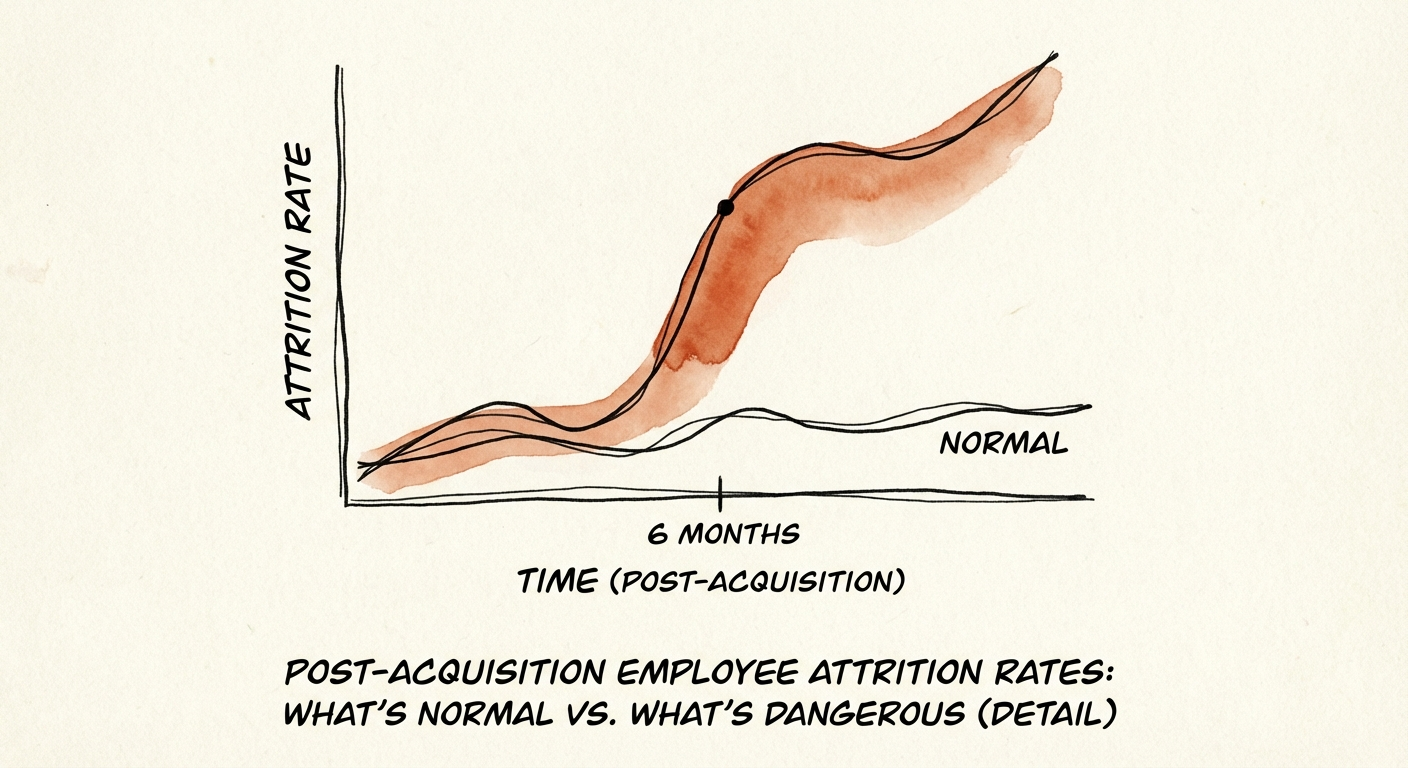

If your post-close attrition crosses 20% in the first 6 months, you aren’t just losing people; you are losing the asset you just bought. Culture clashes are the silent killer of these deals, often invisible until the exit interviews pile up.

The heart always leaves before the body. If you wait until the resignation letter hits your desk, you lost that employee three months ago.

The 2025 Attrition Benchmarks

To diagnose whether your portfolio company is bleeding talent or simply trimming fat, you need to measure against specific M&A benchmarks, not general industry averages. The dynamics of a transaction—uncertainty, new reporting lines, and equity washouts—create a unique pressure cooker.

The 3-Year Danger Zone

Research confirms that the risk doesn't end after the 100-day plan. While the first year sees a sharp spike (33%), the bleeding often continues if integration is botched. 75% of key employees leave within the first three years if proactive retention measures aren't taken. This correlates directly with the typical PE hold period, meaning you might be selling a hollowed-out shell to the next buyer.

Cost of Replacement: The EBITDA Impact

When a key engineer or sales leader leaves, the cost isn’t just the recruiter fee. It’s the stalled product roadmap and the slipped deals. The real cost of bad hiring and turnover is significant:

- Technical Talent: Replacement cost is 100-150% of annual salary due to ramp time and lost IP.

- Leadership: Replacement cost hits 200% of annual salary.

- Sales: The hidden cost is "empty territory time," which directly reduces revenue and EBITDA.

The "Valley of Uncertainty"

Attrition spikes at two specific moments:

- Day 1 to Day 30: The "Shock" phase. Employees who were already wavering use the acquisition as a trigger to leave.

- Month 6 to Month 9: The "Reality" phase. Retention bonuses (if poorly structured) start to feel less motivating compared to the daily friction of new systems, new bosses, and lost autonomy.

If you are seeing a spike at Month 6, it means your integration failed to win hearts and minds. You bought the body, but failed to retain the capability.

The Retention Playbook: Beyond "Pay-to-Stay"

Most PE firms rely on retention bonuses (stay bonuses) as their primary defense. While necessary, they are insufficient. A check keeps a body in a seat; it does not keep a mind engaged. If an engineer is miserable, they will wait for the vesting date and walk out the door the next morning.

1. Re-Recruit Your "Keepers"

Don't assume your new employees are happy just because they haven't quit yet. Treat the top 20% of the acquired workforce as active prospects. In the first week, the acquiring CEO or Operating Partner should sit down with key talent—not to talk about synergies, but to talk about their career path. Zero unwanted turnover requires a personalized offensive strategy.

2. Fix the "Us vs. Them" Narrative

Data shows that acquired employees are 15% more likely to leave than regular hires even three years later. This is often due to permanent "second-class citizen" status. Stop referring to them as "the [Target Company] team." Integrate teams functionally, not just on an org chart. If the acquired CTO becomes a subordinate to the acquirer's CIO without a clear mandate, they will leave.

3. Measure Sentiment, Not Just Headcount

Don't wait for the monthly HR report to spot a trend. Use pulse surveys during the first 100 days to measure sentiment. Ask blunt questions: "Do you have the tools to do your job?" "Do you understand the vision?" A dip in these leading indicators predicts resignation letters by about 4 weeks.

Summary

Attrition of 33% in Year 1 is the default outcome of a passive integration. It destroys deal value and creates a drag on EBITDA that financial engineering cannot fix. To beat the benchmark, you must operationalize retention with the same rigor you apply to cost synergies.