The practical answer

- Short answer

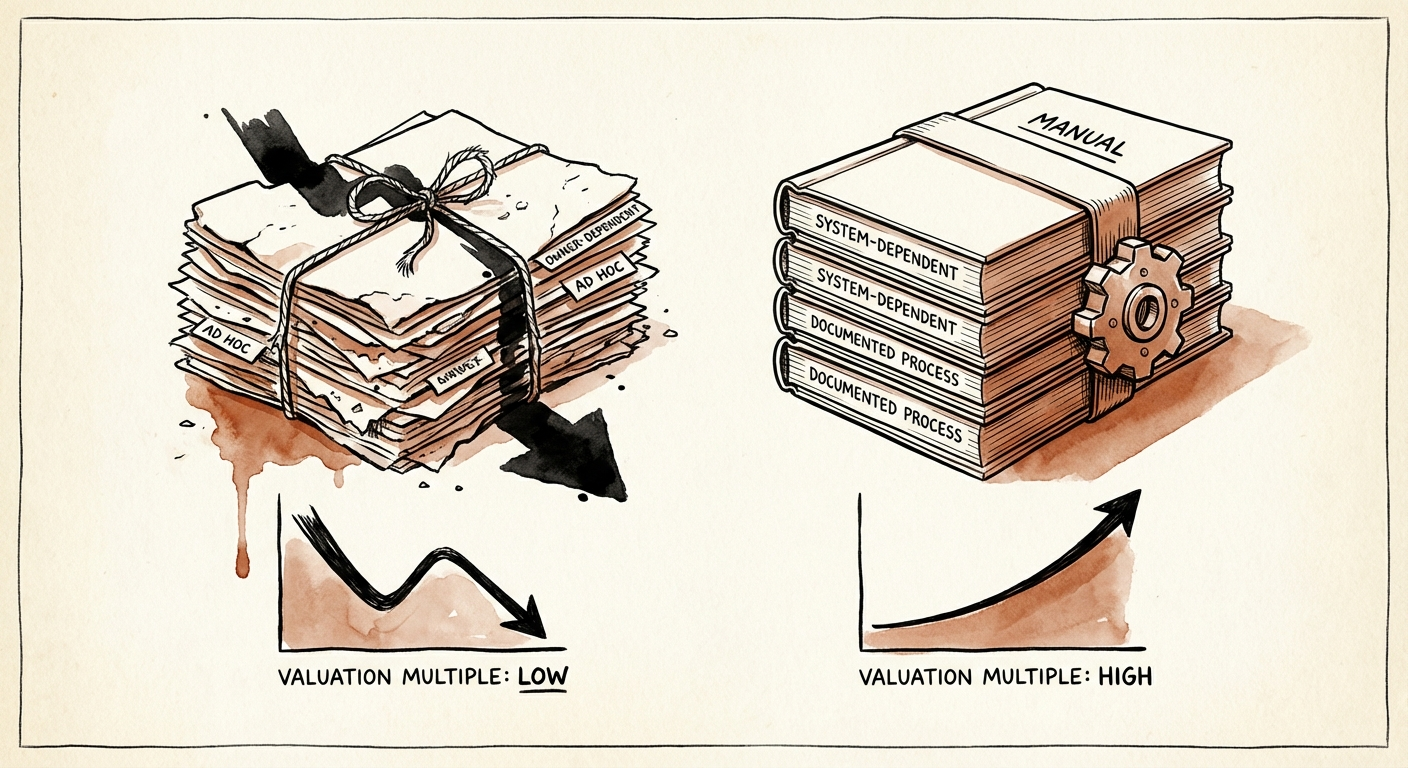

- A buyer's analyst can erase 15-25% of your valuation in one afternoon of diligence. Here are the documentation failures they hunt for in founder-led tech firms.

- Best fit

- Industry: B2B Tech & Services. Function: Operations

- Operating path

- Process Documentation → Operational Excellence → Transaction Execution Services

- Key metric

- 15-25% Valuation discount applied to firms with high "Key Person Risk."

The afternoon a 26-year-old analyst repriced my friend's company

Picture a $22M software-services deal, week three of diligence. The founder is in the conference room feeling good — revenue is up, the team is solid, the LOI looked generous. Then the buyer's associate, maybe two years out of business school, asks to interview a mid-level account manager alone. Twenty minutes later she walks out, opens her laptop, and the offer quietly drops by four points. Nobody yells. The model just changes.

What happened in that room? She asked the account manager a single question: "Walk me through how a renewal gets handled. Where's that written down?" And the answer was, "Oh, I just check with the founder." That sentence is worth millions, and not in the direction the founder wants.

This is the part of exit math that founders of B2B tech and services firms consistently underweight. The acquirer isn't buying your trailing revenue — they're buying the probability that the revenue repeats without you in the building. When the machine only runs because you hand-crank it every morning, you're not selling an asset, you're selling a job, and nobody pays an asset multiple for a job. Valuation specialists put a number on this: undocumented dependence on a single person's tribal knowledge routinely triggers a key person discount of 15-25%. On a $22M deal, that's roughly a Tesla showroom's worth of value erased because nobody wrote things down.

Here's the cruel timing: roughly 70% of M&A deals stall or collapse in diligence, and operational fragility is one of the recurring culprits. The P&L gets you the LOI. The processes and systems — what diligence teams quietly call the "P&S" — decide whether the LOI survives contact with reality.

If the magic that drives your profit walks out the door with you, you don't have a transferable business—you have a high-paying job you're trying to sell.

The ten things a buyer's analyst is actually trained to find

I've sat on both sides of this table. Diligence teams aren't reading your operations manual for the prose. They're hunting for tells — small signals that your business is rented from you rather than owned as a standalone thing. In founder-led tech and services shops, the same ten tells show up again and again.

1. The video graveyard

Someone bought Loom, told the team to "record everything," and now there are 800 clips titled "Tuesday update" and "fixing the thing." Unsearchable, undateable, unverifiable. No analyst is watching 40 hours of screen recordings, so to diligence it functionally doesn't exist. Video is a training aid, not a system of record.

2. Only the happy path is written down

Your SOP covers what happens when everything works. It says nothing about the failed payment, the API outage, the client who threatens to churn on a Friday. Buyers don't pay for optimism; they pay for exception handling. The bug, not the demo, proves maturity.

3. The "last updated: Feb 2022" wiki

Nothing collapses confidence faster than a Confluence timestamp two years stale. It's hard proof your team doesn't actually use the docs to do the work — your process is a museum piece, not a living system.

4. The one big PDF

A 300-page operations manual looks impressive on a shelf and gets referenced by exactly no one before doing a task. Monolithic documents are where knowledge goes to die quietly.

5. The pass-through founder

You documented the process, but step four is still "send to CEO for approval." Congratulations — you documented your own bottleneck. Real founder extraction means writing down the decision criteria so someone else can say yes without you.

6. Policy that the software doesn't enforce

The SOP says "update the CRM immediately," but the CRM fields are optional. The gap between what you wrote and what your tooling permits is exactly where data integrity rots — and analysts test it by pulling the actual records.

7. "Marketing handles it" — which person in marketing?

Role-ambiguous docs make everyone responsible, which means no one is. Buyers want to see a named role attached to each step, not a department.

8. The shadow process

The official workflow lives in SharePoint. The real work happens in Slack DMs. Diligence teams are very good at catching this: they interview your junior staff, who haven't been media-trained, and ask "how do you know what to do?" When the answer is "I ask Sarah," your documentation just got exposed as fiction.

9. Nobody owns the docs

If everyone owns the knowledge base, it rots. Firms that survive diligence assign one accountable owner — a RevOps lead, a chief of staff — responsible for freshness.

10. The 2FA code goes to your phone

You documented every step, but the login still pings a code to the founder's cell. It feels trivial. To a buyer it's a flashing sign that says "this is an owner-operator, not a standalone enterprise."

The 90-day fix you start before the banker calls

You can't retroactively undo years of process debt in the two weeks between LOI and close — and trying to fake it under diligence pressure is how founders get caught. But you don't need to document the whole company. You need to win three interviews.

Triage to the critical 20%. Don't boil the ocean. In a B2B tech or services firm, three workflows carry most of the revenue and most of the risk: the sales-to-onboarding handoff, customer onboarding itself, and major incident response. Document those cold. Leave the expense-report process for later — no buyer reprices a deal over expense reports.

Move to a system of record that keeps a log. Get out of scattered Google Docs and into something versioned and auditable (Notion, Guru, Trainual — the specific tool matters less than the audit trail). The goal isn't a prettier doc. It's being able to tell the analyst, "Here's the process, and here's the log proving we ran it 400 times last quarter," which converts a soft claim into the kind of operational evidence that defends EBITDA quality and the multiple on top of it.

Run the fire drill. The only test that matters: can a new hire execute the critical process without talking to you? Go dark for a week — no Slack, no calls — and watch what breaks. Acquirers pay a premium for that independence precisely because so few founder-led firms can pass it. If the machine seizes up, you've found exactly what diligence will find, except you found it first and on your own timeline.

Do this and the 26-year-old analyst walks out of that conference room with nothing to reprice. That's the whole game: the difference between selling a business and selling a prayer is whether the answer to "who knows this besides you?" is a document instead of a name.