The practical answer

- Short answer

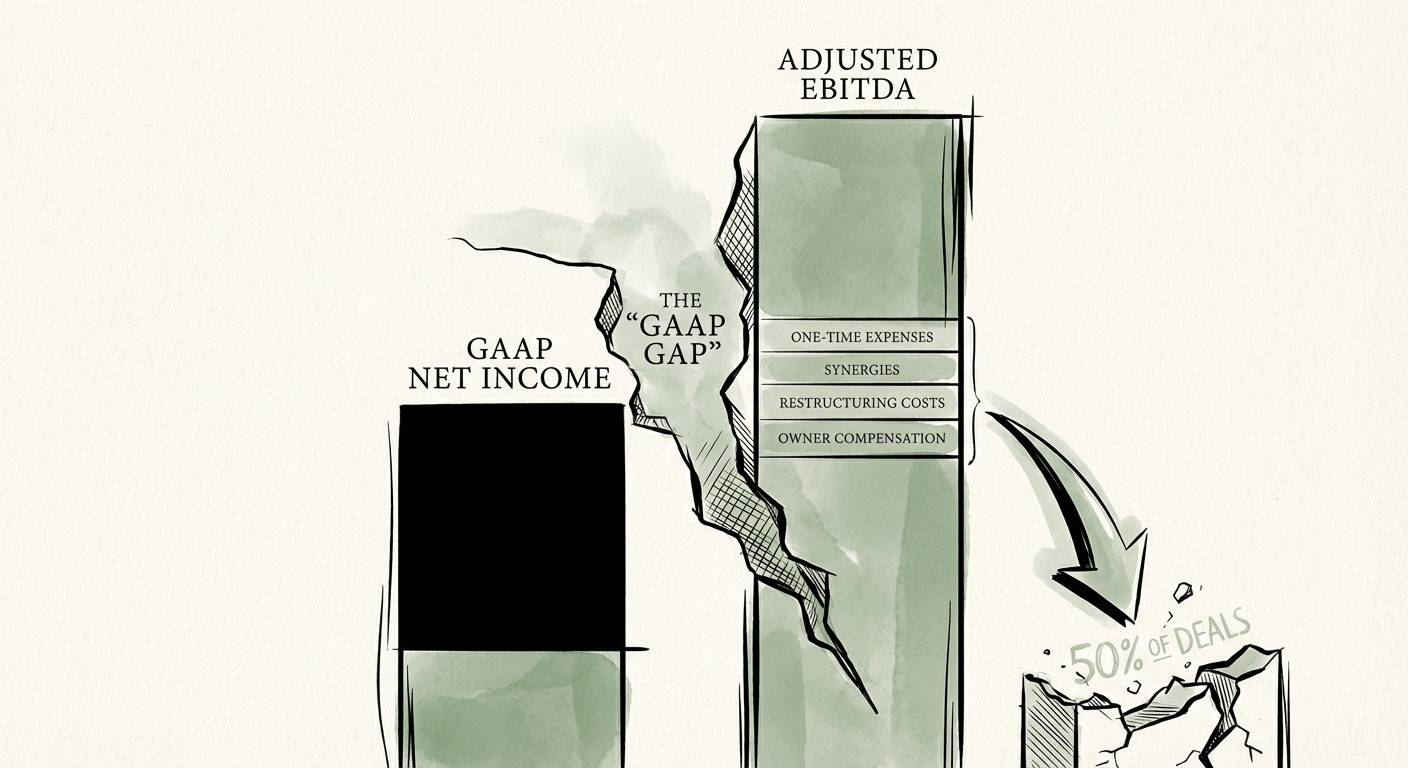

- An audit confirms the numbers are real. A Quality of Earnings report asks if they survive new ownership. Why ~50% of lower-middle-market deals break here.

- Best fit

- Industry: Private Equity. Function: Finance

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 50% M&A deals that fail during due diligence (2025)

A clean audit and a dead deal are not mutually exclusive

Picture a $40M-revenue managed-services company. Three years of audited financials, no qualifications, a Big-Four-adjacent regional firm's signature on every page. The founder hands the package across the table like a passport. The letter of intent goes out at 8x. Everyone shakes hands.

Then the buy-side Quality of Earnings team opens the same books with a different question. Not "are these numbers true?" — the auditor already answered that — but "do these numbers survive a change of ownership?" Three weeks later the picture has moved: a chunk of last year's revenue traced to one client whose contract auto-terminates on a change of control, software costs booked as capitalized development that were really keeping-the-lights-on maintenance, and a year-end cash balance fattened by a few weeks of deliberately stalled vendor payments. None of it is fraud. All of it passed the audit. And all of it walks straight out of the EBITDA line the moment a real operator prices the business.

That gap is where deals go to die. Roughly half of M&A transactions collapse during due diligence, and the financial reconciliation is one of the most common breaking points — the audited story and the operating reality stop agreeing (Rapid Diligence, 2025). The audit and the QoE answer two completely different questions, and confusing them is how a founder talks themselves into an 8x they will never see.

An audit tells you the money came in. A QoE tells you whether it comes back next year, and whether it shows up as cash or as a receivable you'll never collect.

Three places the audited number and the buyable number part ways

An audit is a compliance exercise pointed backward: did the financials follow GAAP, do the bank statements tie out, are the disclosures complete. A QoE is an investment exercise pointed forward: strip the past down to the earnings a new owner actually inherits. As one practitioner put it, audits focus on net income and annual results while a QoE focuses on adjusted EBITDA and reads the monthly cadence underneath it (The Bonadio Group, 2024). Here is where the two numbers split in practice.

The add-back fight, priced in enterprise value

Add-backs are where the seller and the diligence team argue line by line. The founder's leased SUV and conference junkets, fine. But buy-side teams reverse the more creative moves — aggressive capitalization, one-time costs that recur suspiciously often, "owner compensation normalization" that quietly assumes you'll never hire a real replacement. The reason this fight is brutal in the lower middle market is the multiplier. Deals in the $10M–$25M total-enterprise-value band traded around 6.4x trailing EBITDA in 2024 (Middle Market Growth, 2025). At that multiple, every $100K of EBITDA you can't defend isn't a $100K haircut — it's $640K of enterprise value erased. A single contested add-back can move the price more than a month of negotiation.

The working capital peg the audit never looks for

An audit confirms the balance sheet balances on December 31. It says nothing about the other 364 days. A QoE builds a working-capital peg — the normal level of cash a business needs to run on a Tuesday in a slow month, not the dressed-up snapshot at year-end. If a target routinely sits on vendor invoices in December to flatter the cash line, the audit waves it through; the QoE catches the rhythm in the monthly data and resets the peg, forcing more cash to stay in the business at close. That's a real dollar-for-dollar reduction in proceeds the founder never saw coming.

Revenue that's accurate but hollow

Auditors match invoices to deposits. They do not call the customer to ask if they're renewing. A QoE runs concentration and churn analysis to separate durable revenue from revenue that's technically booked and quietly leaving. A perfectly auditable contract with a 60%-likely-to-churn counterparty is exactly the kind of "hollow revenue" that survives the audit and detonates in year one of the hold.

If you're the seller, commission the QoE before the buyer does

Most founders wait for the buyer's QoE and then play defense for six weeks. That's backwards. When the buy-side team writes the first version of your earnings, they own the narrative — every adjustment starts as their assumption, and you spend exclusivity arguing your own numbers back up the hill. The fix is a sell-side QoE done before the data room opens.

Concretely, here's what that buys you on a lower-middle-market exit. You document add-backs while the evidence still exists — the receipts, the board minutes, the rationale — instead of reconstructing them under deadline pressure. You set the working-capital peg off a favorable trailing-twelve-month average rather than letting the buyer anchor it to your weakest month. And you hand the buyer a credible report on day one, which compresses diligence and shrinks the window where deal fatigue, financing wobbles, or a competing target can pull a buyer's attention away. A faster, cleaner process protects the multiple as surely as the numbers do.

So if you're 12–18 months from a sale, do one thing this quarter: pull your own monthly P&L and balance sheet for the trailing three years and look at them the way a buyer's QoE team will — revenue concentration, the real cash-conversion cadence, every add-back you'd have to defend out loud. The audit is the compliance document that proves the past happened. The QoE is the commercial document that decides what the future is worth. Don't show up to the table holding only the first one. For more on separating durable revenue from the booked-but-leaving kind, see our revenue quality audit checklist, and on why entry data dictates the hold, our breakdown of why so many value-creation plans stall in year one.