The practical answer

- Short answer

- Why 22% of professional services EBITDA evaporates in due diligence. A diagnostic guide to ASC 606, WIP traps, and input method failures for PE sponsors.

- Best fit

- Industry: Professional Services. Function: Finance

- Operating path

- Process Documentation → Operational Excellence → Transaction Execution Services

- Key metric

- 22% Average EBITDA reduction in services firms during buy-side QofE due to revenue recognition adjustments.

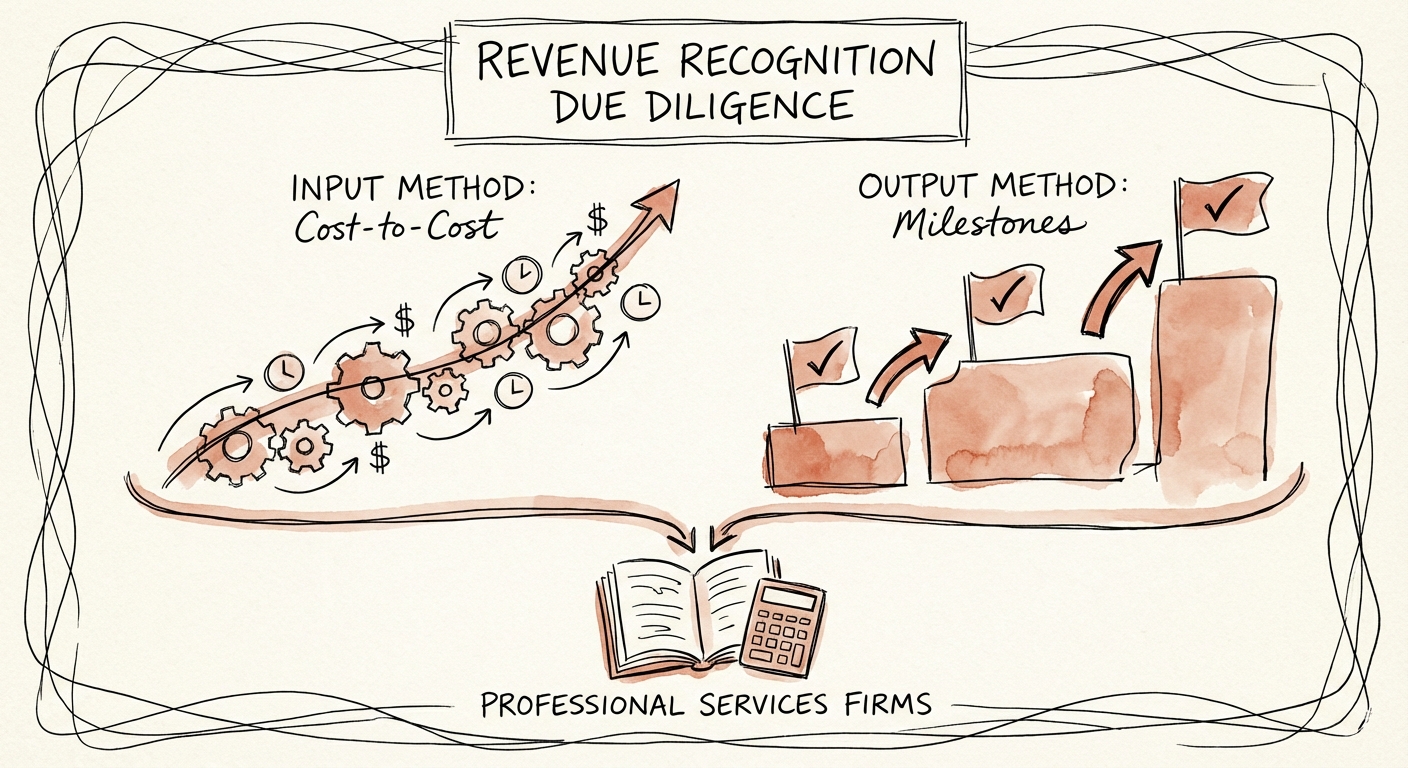

The 'Input Method' Illusion in Lower Middle Market Deals

In the high-stakes theater of lower middle market M&A, few metrics are as malleable—and dangerous—as revenue recognition in professional services firms. While SaaS revenue recognition (ARR) garners the most headlines, services revenue recognition (specifically under ASC 606) is where the deepest due diligence graveyards are located. Our analysis of sell-side Quality of Earnings (QofE) reports reveals that professional services firms see an average 22% reduction in EBITDA during buy-side diligence, primarily driven by aggressive interpretations of "percent complete" accounting.

The core mechanism of this value destruction is the misuse of the Input Method for recognizing revenue. Under ASC 606, firms can recognize revenue over time based on inputs (costs incurred, hours worked) or outputs (milestones achieved, deliverables accepted). In the absence of rigorous process documentation, founder-led firms overwhelmingly default to the Input Method using a "cost-to-cost" approach. This creates a perverse financial incentive: inefficiency looks like revenue growth.

The Mechanism of the Trap

Consider a fixed-price implementation project sold for $100,000 with a budgeted cost of $50,000 (50% margin). If the delivery team is inefficient and burns through $40,000 of labor while only completing 40% of the actual deliverables, the Input Method allows the finance team to claim the project is 80% complete ($40k/$50k costs). They recognize $80,000 in revenue.

However, when a PE sponsor's diligence team applies an Output Method test—verifying actual milestones delivered—they find the project is only 40% complete. The realizable revenue is only $40,000. The $40,000 gap is not just a timing difference; it is an EBITDA hallucination that evaporates precisely when you try to acquire the asset. This "phantom margin" sits on the balance sheet as "Costs in Excess of Billings" (CIE) or unbilled receivables—effectively, a "Inactive WIP" asset that will never convert to cash.

Inefficiency looks like revenue growth under the 'cost-to-cost' method. If you burn 80% of the budget to complete 40% of the work, the P&L says you're 80% complete. The customer says you're failing.

The Diagnostic: 3 Signs of 'Inactive WIP' on the Balance Sheet

For private equity sponsors and operating partners, spotting revenue recognition risks requires looking beyond the P&L and scrutinizing the relationship between Work in Progress (WIP) and Deferred Revenue. A healthy services firm maintains a delicate equilibrium; a distressed asset hides its operational failures in the balance sheet.

1. The CIE/Deferred Ratio Inversion

In a healthy services model, Billings in Excess of Costs (Deferred Revenue) should consistently exceed Costs in Excess of Billings (Unbilled Receivables/WIP). This indicates the firm is billing ahead of work, maintaining positive working capital. When this ratio inverts—and Unbilled Receivables begin to climb faster than revenue growth—it is a leading indicator that the firm is recognizing revenue aggressively on "inputs" without securing the corresponding "outputs" (customer acceptance/invoices). This is often explained away as "administrative billing delays," but in 70% of cases, it represents scope creep that the customer has not agreed to pay for.

2. The 'Milestone Mirage'

Review the firm's process documentation for milestone acceptance. In many IT consulting valuation scenarios, firms tie billing triggers to calendar dates (e.g., "payment due on Month 3") rather than performance obligations. Under ASC 606, simply reaching a date does not necessarily transfer control of a service to the customer. If revenue is recognized based on the billing schedule, but the project is delayed, the firm has effectively borrowed revenue from the future. Diligence must map Revenue Recognition Policy vs. Billing Terms vs. Actual Delivery Evidence. Gaps here lead to massive retrospective adjustments.

3. The Gross vs. Net Trap (Principal vs. Agent)

Many digital agencies and IT consultancies pass through third-party costs—media spend, software licenses, or hosting fees—and recognize the gross amount as revenue. While this inflates the top line, it crushes the valuation multiple. If a firm books $10M in gross revenue but $4M is pass-through ad spend, they are essentially a $6M agency trading at a $10M valuation. The litmus test in diligence is control: Does the firm have inventory risk? Do they have discretion in establishing the price? If not, ASC 606 requires net presentation. Reclassifying from gross to net doesn't change EBITDA dollars, but it radically alters the EBITDA margin %, often revealing that a "high-growth" firm is actually a low-margin pass-through entity.

Auditing the 'Transfer of Control' Documentation

The ultimate defense against revenue recognition surprises is not financial analysis, but process documentation. Financial figures are merely the downstream output of operational events. To validate revenue quality, you must audit the operational artifacts that prove control was transferred.

The 'Evidence of Arrangement' Checklist

Before signing an LOI, request a sample audit of the top 5 largest active contracts. You are looking for the "Golden Thread" that connects the initial SOW to the final revenue entry:

- Signed Change Orders: Are over-budget hours supported by a signed Change Order (CO)? If hours are booked to revenue without a CO, that is not revenue; it is a cost overrun.

- Technical Acceptance Records: For milestone-based revenue, does the firm possess a distinct "Client Acceptance Form" or email confirmation? Auto-approval clauses are weak evidence in a Quality of Earnings audit.

- Stand-Alone Selling Price (SSP) Analysis: For bundled services (e.g., implementation + managed services), has the firm documented the SSP for each component? Allocating too much value to the upfront implementation (recognized immediately) vs. the ongoing support (recognized over time) is a common manipulation tactic to pull revenue forward.

Converting Findings to Valuation Adjustments

When these gaps are identified, they should not necessarily change the deal, but they must re-price it. Moving a target from Input Method (Cost-to-Cost) to Output Method (Milestones) often results in a one-time "revenue deferral" adjustment. While this hurts the TTM (Trailing Twelve Months) revenue, it builds a deferred revenue backlog that the buyer will benefit from post-close. Savvy PE sponsors use this revenue recognition trap to negotiate a lower multiple on the entry, knowing the revenue is simply shifted, not lost.