The practical answer

- Short answer

- 75% of founders regret their exit within one year. This diagnostic guide prepares you for the operational and psychological shift of life after the deal.

- Best fit

- Industry: B2B Tech. Function: CEO/Founder

- Operating path

- Founder Extraction → Operational Excellence → Interim Management

- Key metric

- 75% Founders who regret their exit within 1 year (Source: EPI)

The Silence After the Wire

You have spent the last seven years optimizing for a single moment: the wire transfer. You have visualized the notification. You have calculated the net proceeds. You have already mentally spent the capital on a beach house or an angel portfolio.

But you haven't optimized for the morning after.

According to the Exit Planning Institute and PwC, 75% of business owners profoundly regret their exit within 12 months. They don't regret the money; they regret the void. For a founder, the business is not just an asset; it is the primary architecture of their existence. It dictates their schedule, their social circle, their dopamine loops, and their sense of utility.

When that architecture is removed overnight, the result is not relief. It is vertigo.

The market tells you to focus on transferable value and EBITDA multiples. That is correct, but incomplete. If you do not engineer your own extraction—operationally and psychologically—before the Letter of Intent (LOI) is signed, you are not just risking your mental health. You are risking the deal itself.

Buyers smell founder dependency. They quantify it as "Key Person Risk," and they price it rigorously. If you are the only one who can close the big deals or fix the server outage, you are not an asset. You are a liability that needs to be hedged.

If you are the only one who can close the big deals or fix the server outage, you are not an asset. You are a liability that needs to be hedged.

The Math of Dependency

Let’s put a price on your inability to let go. In lower middle-market M&A, "Key Person Risk" typically triggers a 10% to 25% valuation discount. On a $20M exit, your heroics are costing you $2M to $5M in enterprise value.

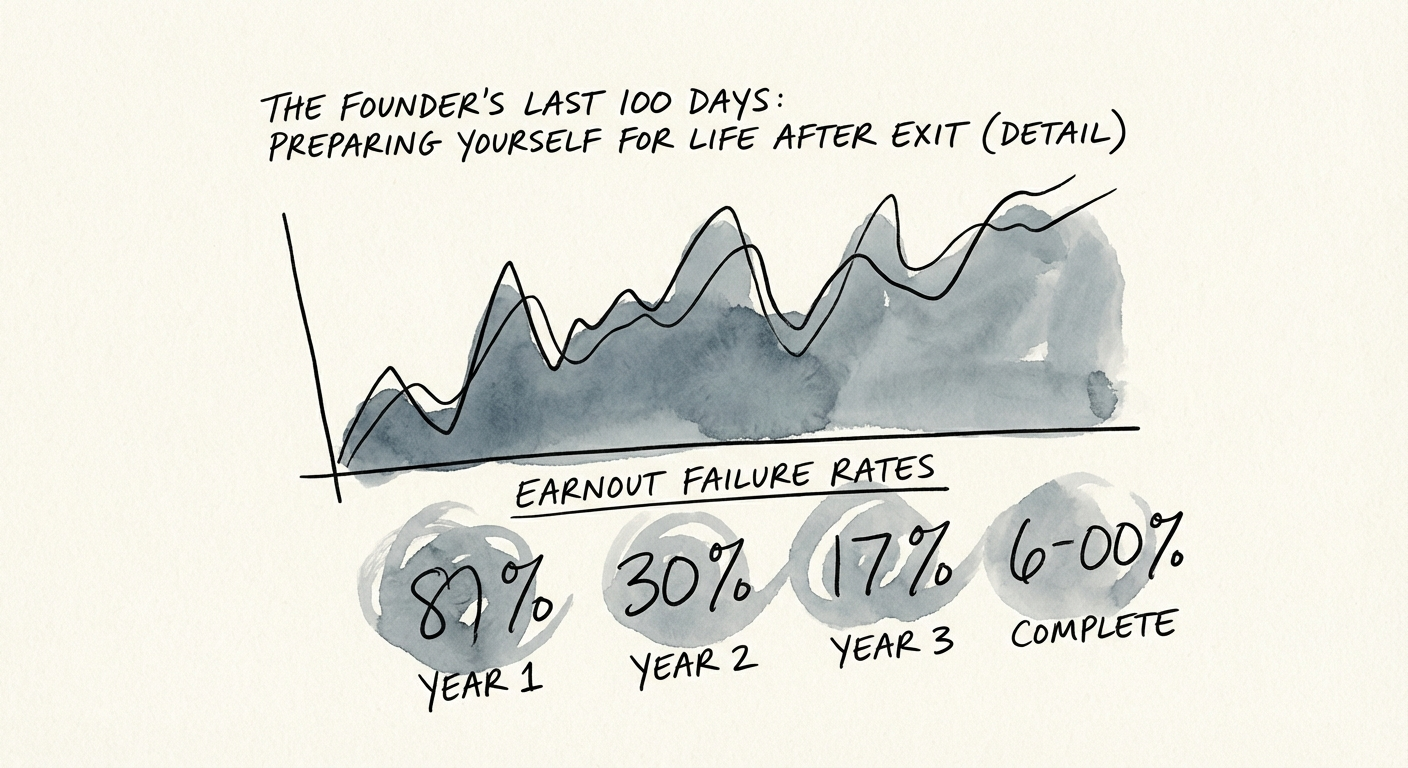

But the real carnage happens in the earnout.

Most founders assume the earnout is just "delayed cash." They believe that if they stay on for two years, they will hit the targets and collect the full check. The data says otherwise. A 2024 study by SRS Acquiom revealed that across private M&A deals, only 21% of the aggregate maximum earnout potential was actually paid out.

Why is the failure rate so high? Because the skills required to start a company are diametrically opposed to the skills required to integrate one. You are used to speed, autonomy, and gut instinct. The acquirer values compliance, governance, and consensus. This culture clash leads to identity crisis, friction, and ultimately, missed targets.

You are not just fighting for a multiple; you are fighting against a statistical probability of failure. If you haven't documented your processes and delegated your decision-making authority before the 100-day countdown begins, you are handing the acquirer the leverage to withhold 30% of your purchase price.

The 100-Day Extraction Protocol

You cannot solve this problem after the close. The last 100 days before an exit are your final window to operationalize your absence. Here is the protocol:

- Days 100-60: The Calendar Audit. Look at your last 90 days of calendar data. Identify every meeting where you were the primary decision-maker. Your goal is to reduce this by 50% in the next 30 days. If you are in the room, you are training your team to defer to you. Leave the room.

- Days 60-30: The SOP Sprint. Tribal knowledge is value leakage. Every process that lives in your head is a dollar subtracted from your exit. Document the "unwritten rules" of your sales motion and product roadmap. Buyers pay a premium for systems, not geniuses.

- Days 30-0: The Identity Hedge. This is the hardest part. You must begin to build a life outside the P&L. Reconnect with the interests you starved to feed the business. If your entire self-worth is tied to your earnout performance, you will micromanage the integration and destroy the value you built.

The successful exit is not defined by the wire transfer. It is defined by the sustainability of the company without you, and the sustainability of you without the company. Build a machine that runs itself, so you can finally be the operator of your own life.