The practical answer

- Short answer

- The average earnout pays 21 cents on the dollar. For founders selling a B2B tech company, here is how the metric, the term, and three clauses decide your check.

- Best fit

- Industry: B2B Tech. Function: M&A Negotiation

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 28% Dispute rate for M&A earnouts

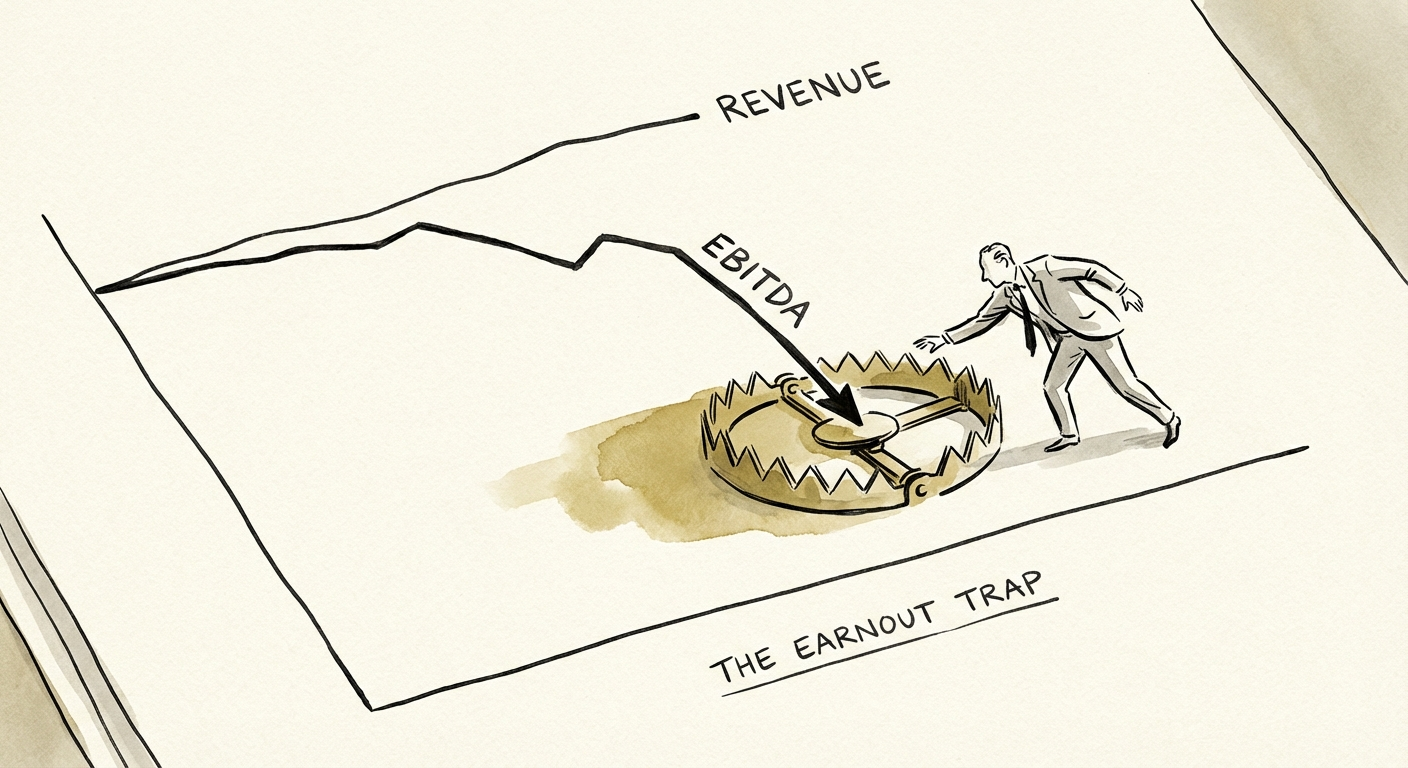

You sold for $50M. You'll probably collect $35M.

Picture the LOI on your screen: $50M for your B2B software company, $35M at close and $15M in an earnout tied to next year's numbers. You run the growth curve in your head — 40% last year, pipeline is full — and the $15M feels like money you've already earned. That confidence is exactly the reaction the structure was designed to produce.

Here is the part the banker skips. SRS Acquiom's 2024 M&A Claims Insights Report found the average earnout pays just 21 cents on the dollar. On your $15M, that's roughly $3M. Even in the deals that do trigger a payment, sellers typically land around half the maximum. And 28% of these arrangements don't end in a wire transfer at all — they end in a dispute.

The reason is mechanical, not malicious. The day before close, the buyer wants your revenue to compound. The day after, they want your costs absorbed into their org chart. Those are opposite goals, and your earnout sits on the wrong side of the switch. The buyer is no longer running your growth plan; they're running their integration plan, and your targets are now line items someone else gets graded on cutting.

For a founder who built a company on recurring revenue and clean retention math, accepting a payout you can't model and can't control is a worse trade than a discount you can bank. The fix isn't refusing the earnout — buyers use them to bridge a real valuation gap. The fix is engineering the terms so the gap closes in your favor. Womble Bond Dickinson notes these structures spike whenever the market gets uncertain — which means more founders are walking into this exact trap right now.

An earnout isn't a bonus. It's a deferred payment the buyer is hoping the integration plan quietly kills before it ever comes due.

The metric is the whole negotiation

Before you argue about the dollar amount, win the argument about what gets measured. That single word — revenue or EBITDA — decides more about your check than the headline price does.

Buyers will lobby hard for EBITDA. The pitch sounds principled: "Let's align on profitable growth, not vanity revenue." Do not accept it. Once you've sold, you no longer control the cost line — and EBITDA is the line they control. They can allocate corporate overhead onto your P&L, book "integration costs" against your unit, charge you for shared services you never asked for, and freeze the key hire your plan depended on. Each of those is a defensible accounting choice that quietly makes your target unreachable. Revenue is a number a customer paid. EBITDA is a number an accountant chose. That's why 62% of 2024 earnouts measured on revenue versus roughly 22% on EBITDA — sellers learned which one the buyer can't quietly redefine.

Time is the buyer's other lever

The median earnout now runs 24 months, and every extra month is a coin flip you didn't ask to take — a re-org, a budget freeze, a strategic pivot that retires your product line. Anchor the period at 12 to 18 months. If the buyer insists on longer, attach a catch-up: miss Year 1, crush Year 2, and you still collect the full amount. Without it, a single soft quarter on their watch can zero out a payment your trailing performance fully earned.

Then nail down the baseline. Write into the agreement what "normal operations" looks like — current headcount, the marketing budget, the roadmap, the sales coverage that produced your numbers. If you can't point to a documented operating plan, the buyer gets to argue you failed to execute rather than admit they failed to resource the business. The founder who can show "this is the engine you bought, and you turned it down to idle" wins that fight. The one working from memory and a verbal promise does not.

Three clauses that decide whether the wire ever clears

The dollar figure is the easy part of the term sheet. The governance language is where the 21-cent average gets made — or unmade. A "commercially reasonable efforts" clause sounds protective and means almost nothing when a dispute actually lands in front of a judge. You need covenants with teeth. White & Case walks through how the best current earnout drafting builds protection directly into the operating mechanics — push to put yours there too.

- Budget protection that floats your targets. If the buyer cuts the spending that drives the metric, the metric resets. Say they slash your demand-gen budget 50% to fund a different priority — your revenue target should ratchet down with it. Without this, they can defund your number and then blame you for missing it.

- Change-of-control acceleration. If your acquirer sells the company again 18 months in — a flip, a roll-up, a recap — your earnout pays out at 100%, immediately. You negotiated against this buyer's behavior, not a stranger's. This shows up in only about a fifth of first drafts, so you will have to add it yourself.

- Anti-cannibalization credit. When the buyer cross-sells your product to their existing base, that revenue counts toward your target even though their rep closed it. Otherwise "synergy" becomes the polite word for a buyer absorbing your growth and crediting it to themselves.

One more test, and run it before you sign the LOI, not after: figure out why they're buying you. Acquirers chasing your growth engine will give on these clauses, because they intend to hit the numbers anyway. Acquirers buying you for cost takeout will fight every one — and that resistance is your signal that the earnout is decorative paper. Make the metric revenue, cap the term, and write the three covenants in plain English. Get paid for the company you built, not for subsidizing the risk the buyer didn't want to carry alone.