The practical answer

- Short answer

- PE-backed CFO total cash runs $325k–$420k at $10–50M revenue up to $525k–$720k at $100–250M, plus ~1–1.25% equity. How to structure the grant.

- Best fit

- Industry: Private Equity. Function: Finance

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- $525k Avg. Total Cash Comp ($100M-$250M Rev)

The Candidate Profile That Makes You Flinch

Closing week on a founder-led $40M ARR platform. Product is real, churn is fine, and the books are held together with a controller, a part-time bookkeeper, and a QuickBooks file the founder's cousin set up in 2018. You know the next hire is a finance leader who can build a 13-week cash model, hold the line in a lender call, and tell you which of the founder's three pricing experiments is actually losing money. So you call a search firm.

The first profile lands at $375,000 base, a 50% bonus target, and 1.5% of fully diluted equity. If you anchored on a 2019 corporate band, that number reads like a typo. The reflex is to counter at $250k and "make it up on the upside."

Resist it. At the lower revenue bands, the underpriced CFO is the line item that quietly compounds into a write-down. Heidrick & Struggles' PE-backed CFO compensation survey shows total packages for genuinely sponsor-ready finance leaders sitting well above what a generalist controller commands — and the gap exists for one reason. A controller reconciles what already happened. A portfolio CFO tells you, in February, that you will trip a leverage covenant in Q3 unless you pull two levers now. You are not paying for bookkeeping. You are paying for the eight months of warning.

At a $60M company, the CFO you can afford and the CFO who survives a covenant breach are two different people. Pay for the second one — the first one will restate your numbers in year two.

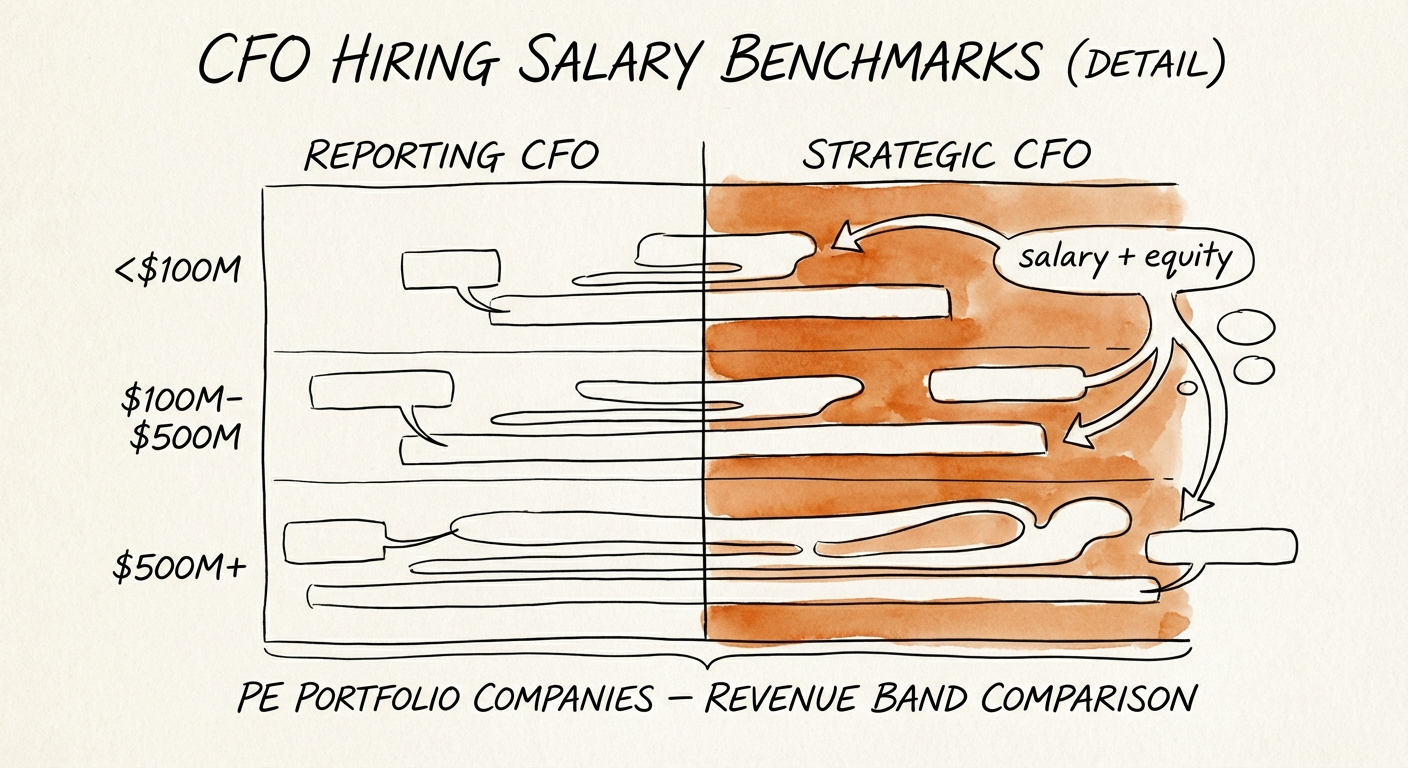

The Numbers, Banded — and Why Each Band Buys a Different Person

The figures below aggregate 2025-2026 placement data from search firms that live in the middle market — Heidrick & Struggles, Charles Aris, and JM Search — cross-checked against Conexus Recruiting's portfolio benchmarks. These are total cash (base plus target bonus) for candidates who have actually done a PE hold before. The band you are in does not just move the number — it changes the job.

$10M - $50M revenue: you are buying a player-coach

Base $250k-$300k, bonus 30-40%, total cash roughly $325k-$420k. At this size there is no FP&A team to hide behind. The same person who presents the board deck on Thursday is rebuilding the chart of accounts on Tuesday and chasing a late vendor payment on Friday. Budget below $300k here and be honest with yourself: you are hiring a VP of Finance and calling it a CFO. That is a defensible choice — just don't expect the title to do work the comp didn't pay for.

$50M - $100M revenue: the band where lowballing breaks you

Base $300k-$375k, bonus 40-50%, total cash $420k-$560k. This is the unforgiving zone. The company is now complex enough that a backward-looking finance leader will drown — multiple entities, real debt, a board that wants a 90-day rolling forecast — but small enough that you feel the cash. Pay below median and you get someone who reports the miss instead of one who saw it coming. The $50k you "save" on base reappears as a restatement, a blown lender relationship, or a diligence finding that knocks a turn off your exit multiple.

$100M - $250M revenue: the CFO is the de facto COO

Base $350k-$450k, bonus 50-60%, total cash $525k-$720k. At this scale the finance seat owns far more than finance — pricing, M&A integration, the systems roadmap. You are paying COO-grade compensation for the title that says CFO.

One pattern worth more than the bands themselves, per JM Search's read of the market: experience drives comp harder than revenue does. A first-time CFO might sign at $300k; a finance leader with 6-10 years and a clean exit on the résumé clears $350k regardless of company size. You are not buying years. You are buying the pattern recognition that turns a looming liquidity crisis into a Tuesday problem instead of a board emergency.

How to Structure the Offer So They Close — and Stay

Cash keeps the seat warm; equity gets the candidate to the finish line. For a PE CFO the grant is the real compensation, and it behaves nothing like the liquid RSUs they may have left at a public company. Your equity is locked for three to five years, so candidates rationally demand a premium for the illiquidity. Standard grants run 0.75%-1.5% of fully diluted; the market clears around 1.0%-1.25% for a non-founder CFO joining at the start of a hold. Increasingly that grant splits 50% time-based and 50% tied to a MOIC or EBITDA hurdle, which aligns the CFO to your return — not to a calendar.

Three moves that actually land the hire:

Sell the equity math, not the base. If a candidate grinds you for $20k more in base but shrugs at the vesting terms, treat it as a signal — they are taking a job, not buying into an exit. Walk a strong candidate through the concrete path to a seven-figure payout at close. That conversation closes the deal; a base negotiation rarely does.

Bridge the gap with a milestone bonus, not a higher salary. When candidate expectation outruns your budget, offer a one-time $25k-$50k bonus tied to specific first-six-months outcomes: pulling DSO down by 10 days, standing up the forecast that survives a board, clearing a clean revenue quality audit, or finishing the first-time CFO installation. You pay for value delivered, not for time served.

Match the band to the mandate before you write the JD. A $40M player-coach and a $200M de facto COO are different hires with different price tags; advertising one and budgeting for the other wastes the 30-day window strong candidates are actually on the market. In 2026, financial engineering alone won't carry an exit — you need operational financial leadership, and the ROI on a CFO who prevents a single write-down dwarfs the delta you were tempted to save on base. More on building exit-ready finance leadership →