The practical answer

- Short answer

- Why "lift and shift" Azure partners trade at 7x EBITDA while modernization specialists command 13x. A diagnostic guide for PE Operating Partners.

- Best fit

- Industry: Cloud Services / Private Equity. Function: M&A / Corporate Development

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 13.0x Median EBITDA multiple for Specialized Modernization Partners (AKS/AI) in US markets.

The 'Lift and Shift' Hangover Is Killing Your Exit

In 2021, the Private Equity playbook for cloud services was simple: buy a generalist Managed Service Provider (MSP), acquire a few smaller Azure migration shops, consolidate the EBITDA, and sell the 'platform' at 12x. The value driver was consumption growth. If your portfolio company could move on-premise servers to Azure (Lift and Shift) and resell the consumption (CSP), you were winning.

That playbook is now high-risk.

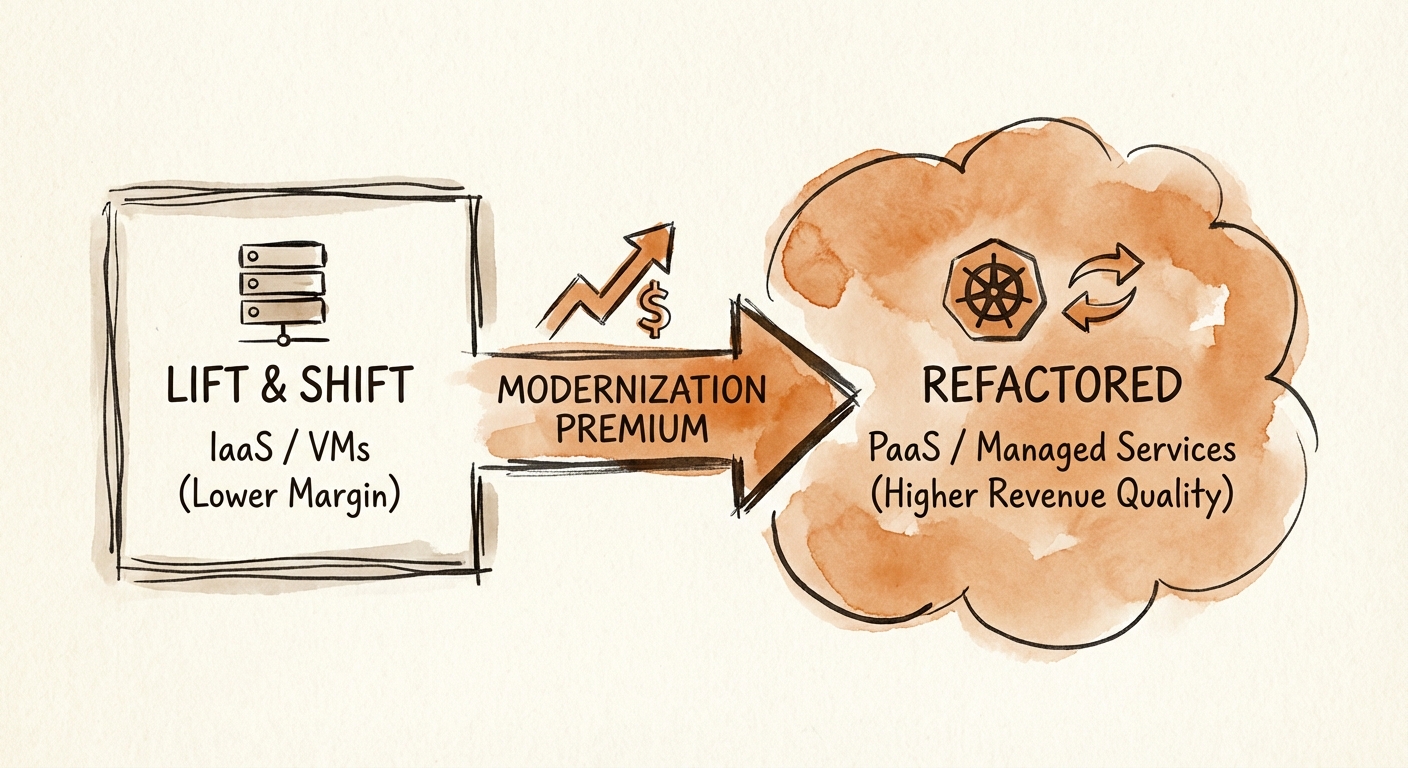

In 2026, "Lift and Shift" is no longer a value-add; it is a commodity. Our data from Q4 2025 M&A transactions shows a stark bifurcation in the market. Generalist Azure MSPs—those primarily focused on IaaS resell and basic VM management—are seeing valuations compress to 6.5x – 8x EBITDA. Buyers view these revenue streams as "low quality" because they are prone to margin erosion from Microsoft's partner program changes and aggressive competition from Global Systems Integrators (GSIs).

Worse, the "Lift and Shift" model has created a massive technical debt burden for customers. Portfolio companies that migrated servers without modernizing applications are now drowning in Azure consumption costs without seeing the promised agility. Consequently, retention rates for these generalist partners are slipping.

For PE Operating Partners, this presents a critical risk. If your IT services asset is positioned as a "Cloud Migration Partner" but lacks deep modernization capabilities, you are bringing a commodity asset to a specialist market. You aren't selling a digital transformation enabler; you're selling a utility company.

In 2026, you either speak fluent Kubernetes or you speak the language of a commodity. The 5-turn valuation gap between the two is the cost of refusing to modernize.

The Anatomy of the 13x Premium: What Buyers Actually Want

While generalists struggle to clear 8x, a specific subset of Azure partners is commanding 12x – 14x EBITDA multiples. These are the Infrastructure Modernization Specialists.

The valuation gap isn't random. It reflects the market's pivot from "Cloud Adoption" to "Cloud Optimization and AI Readiness." Strategic acquirers (IBM, Accenture, and specialized PE platforms) are paying premiums for firms that solve the problems created by the first wave of cloud migration.

1. The "Refactor" Premium (Kubernetes/AKS)

Partners who specialize in moving workloads from Virtual Machines (IaaS) to Azure Kubernetes Service (AKS) and PaaS are trading at the top of the range. Why? Because containerization creates "sticky" engineering relationships. A VM is easy to move to another provider; a fully refactored microservices architecture managed via Terraform is deeply entrenched. Buyers pay for the switching costs you impose on your customers.

2. The AI Infrastructure Wedge

You cannot run Azure OpenAI Service on a legacy SQL Server running on a VM. You need modern data estates (Fabric, Cosmos DB) and scalable inference infrastructure. Partners who frame their services as "Building the AI Foundation"—rather than just "Cloud Management"—are seeing a 3-turn EBITDA expansion. They aren't selling IT support; they are selling the prerequisite for the customer's future strategy.

3. FinOps as a Service

The number one complaint from PE-backed enterprises is Azure cost overrun. Partners offering proprietary FinOps methodologies—guaranteeing, for example, a 20% reduction in spend through reserved instance orchestration and spot fleet automation—are valued as software-enabled services. Their revenue is viewed as "high value" because it is self-funding.

The Pivot: Turning a Generalist into a Specialist

If you are holding a generalist Azure MSP, you cannot simply "rebrand" to capture this premium. You must re-engineer the revenue mix over the next 18 months. The goal is to shift your narrative from "We manage servers" to "We modernize infrastructure."

Step 1: The Revenue Quality Audit. Look at your revenue mix. If >60% is CSP Resell and pure IaaS management, you are in the danger zone. You need to aggressively cross-sell "Modernization Assessments" to your existing base. This isn't just about revenue; it's about demonstrating to a future buyer that you have the permission to do high-value work.

Step 2: Productize the "Fix." Don't sell hourly consulting. Package a "Kubernetes Migration Accelerator" or a "Data Estate Modernization Sprint." Productized services with defined outcomes and fixed prices trade at higher multiples because they imply scalable IP rather than just headcount.

Step 3: Certify for Capability, Not Capacity. Stop chasing generic "Solutions Partner" designations. Focus on the Azure Kubernetes Service (AKS) and AI & Machine Learning specializations. In due diligence, we see buyers discounting "Gold" badges but paying premiums for "Advanced Specializations" that align with their thesis.

The window to exit a "Lift and Shift" shop closed in 2024. The window to exit a Modernization Specialist is wide open. You don't need to change your entire business, but you do need to change the story your EBITDA tells.