The practical answer

- Short answer

- ServiceNow Elite partners command 2.8x+ revenue multiples while generalists stall at 1x. Learn the valuation drivers: IP, managed services, and workflow specialization.

- Best fit

- Industry: Professional Services / Tech-Enabled Services. Function: M&A / Corporate Development

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 2.8x Revenue multiple for specialized ServiceNow partners with >30% recurring revenue.

The Great Bifurcation: Body Shops vs. Transformation Partners

If you own a ServiceNow partner doing $20M in revenue, you might think you’re sitting on a $40M–$60M asset. You’re likely wrong.

The ServiceNow ecosystem has bifurcated. On one side, you have the capacity players—firms that essentially rent out certified bodies to fill seats on massive GSI implementations. These firms trade like traditional staffing agencies: 0.8x to 1.2x revenue (or 6x–8x EBITDA).

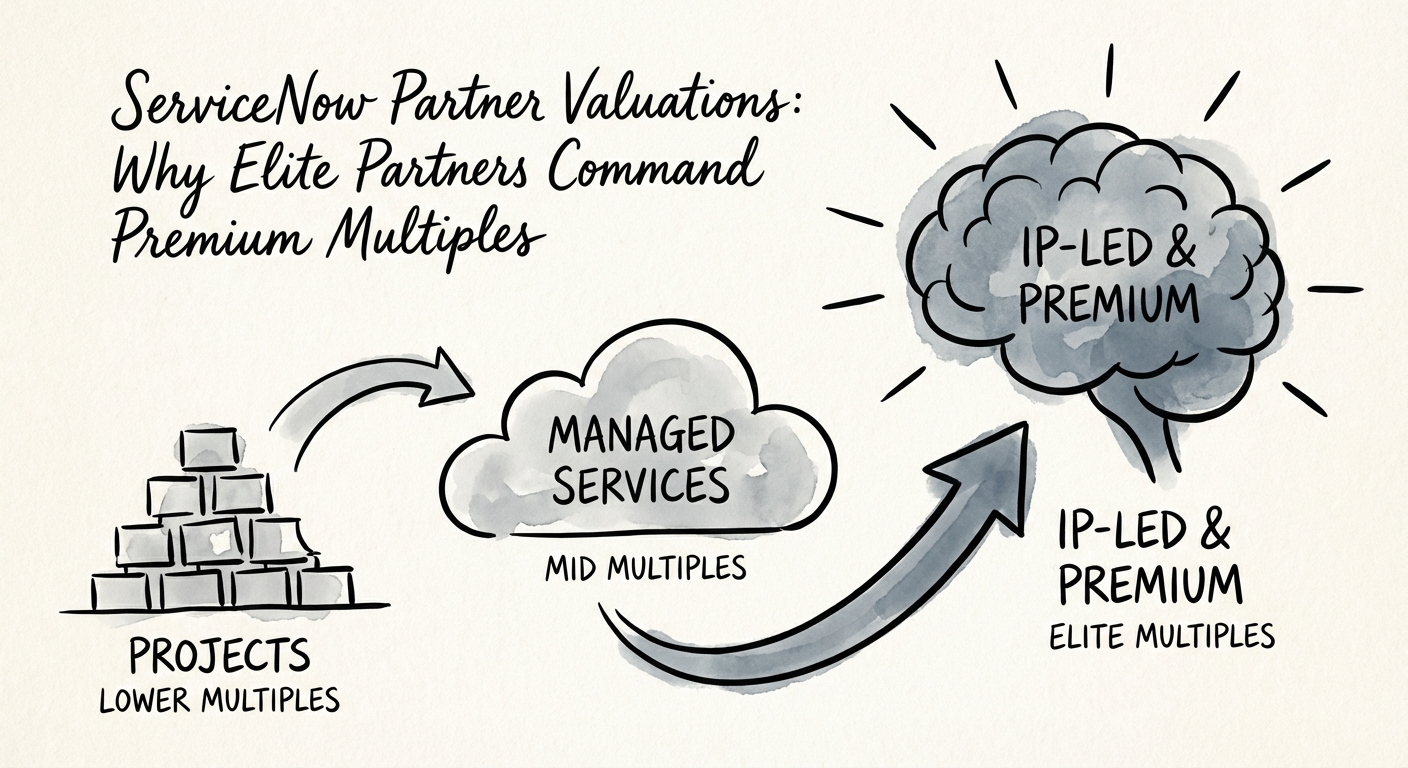

On the other side, you have the capability players. These are the Elite and Global Elite partners who don’t just implement; they own the outcome. They have proprietary IP on the ServiceNow Store, they lead with high-value workflows like CSM (Customer Service Management) and HRSD (HR Service Delivery), and they have wrapped their delivery in managed services contracts. These firms command 2.5x to 3.5x revenue (or 12x–15x EBITDA).

As a PE Operating Partner, your job is to identify which one you just bought—and if it’s the former, how to engineer it into the latter before the hold period expires.

The Valuation Matrix

We see a consistent pattern in deal terms for 2024-2025. The market pays a premium for "revenue quality," not just revenue quantity.

- Commodity Partner: 80% ITSM focus, largely time-and-materials (T&M) contracts, heavy reliance on sub-contractors. Valuation: ~1.0x Revenue.

- Elite Specialist: 50% non-ITSM revenue (CSM, Creator, SecOps), 20%+ Managed Services (recurring), <10% contractor usage. Valuation: ~2.5x Revenue.

You don't get paid 15x EBITDA for implementing Incident Management. You get paid for owning the customer's digital nervous system through proprietary workflows and managed innovation.

The "Badge" Trap: Why Elite Status Isn't Enough

Many founders believe that reaching "Elite" or "Global Elite" status is the golden ticket to a high multiple. It is necessary, but it is not sufficient. The badge gets you into the room; your revenue mix gets you the deal.

Acquirers in 2025—whether strategic buyers like Accenture and Deloitte or financial sponsors—have grown sophisticated. They know that ITSM (IT Service Management) is a mature, commoditized market. It's the "dial tone" of the enterprise. There is no alpha in setting up Incident Management for the 1,000th time.

Where the Premium Lives: High-Value Workflows

The valuation premium has shifted to the emerging workflows where supply of talent is low and business impact is high:

- Customer Workflows (CSM): Directly impacts the client's revenue retention. High strategic value.

- Employee Workflows (HRSD): Critical for enterprise efficiency and employee experience.

- Creator Workflows (App Engine): Building custom apps on the Now Platform. This creates "sticky" dependencies that prevent churn.

If your portfolio company is 90% ITSM, you are selling a utility. If you can shift that mix to 40% CSM/HRSD/Creator over the next 18 months, you fundamentally change the valuation profile from "IT Services" to "Digital Transformation."

The "SaaS-Like" Service Model

The holy grail for a services firm exit is to look as much like a software company as possible without actually being one. In the ServiceNow ecosystem, this means two things: IP and Managed Services.

1. Intellectual Property (The "Store" Play)

Does the firm have apps listed on the ServiceNow Store? Real IP isn't just a marketing slide; it's a licensable asset that accelerates implementation or solves a niche vertical problem (e.g., "University Housing Management on Now"). Buyers pay for IP because it improves gross margins (write code once, sell it 100 times) and creates a competitive moat.

2. Managed Services vs. Projects

Project revenue is lumpy. It requires you to resell the firm every January 1st. Managed Services revenue—specifically "Managed Innovation" or "Platform Sustainment" contracts—is recurring. A firm with 30% recurring revenue commands a significantly higher multiple than one with 5%. Warning: "Staff Augmentation" retainers do not count as high-quality recurring revenue. That is just T&M in disguise.

The Diagnostic: Is Your Asset Ready?

To prepare a ServiceNow partner for a premium exit, audit these three metrics immediately:

- Certified Master Architect (CMA) Count: The scarcest resource in the ecosystem. Do you have them?

- Revenue per Head: If it's under $200k, you're a body shop. Elite firms push $250k–$300k.

- Churn: Not just customer churn, but talent churn. In this ecosystem, the assets go down the elevator every night.