The practical answer

- Short answer

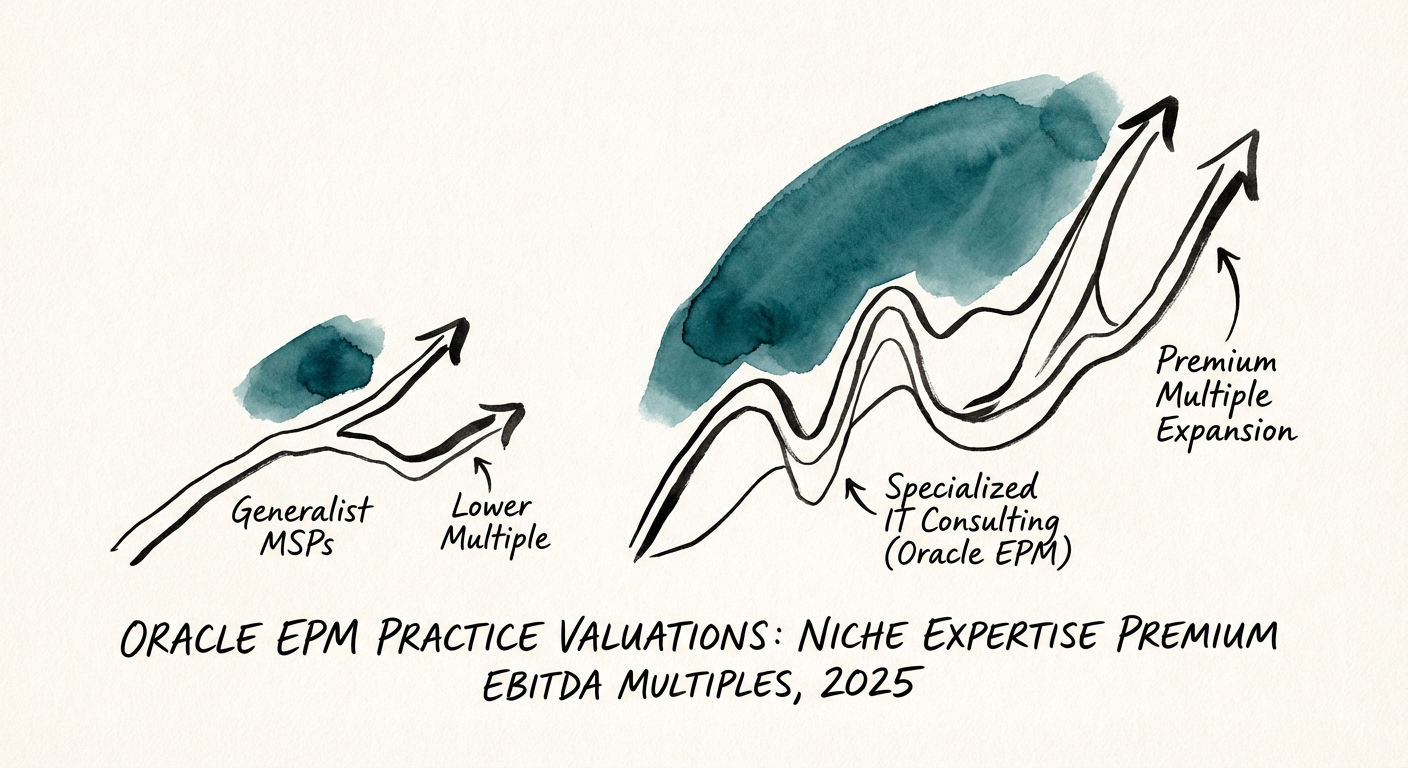

- Why Oracle EPM practices trade at 12x+ EBITDA while generic IT services stall at 6x. Benchmarks, valuation drivers, and the specialization premium explained.

- Best fit

- Industry: Professional Services / Tech Enabled Services. Function: M&A / Corporate Development

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 13.6x Median EBITDA multiple for specialized IT consulting firms in 2025, outpacing generalist peers.

The Valuation Delta: Generalist vs. Specialist

If you are holding a generic IT Managed Services Provider (MSP) or a broad-spectrum digital transformation shop, you are likely staring at a 6x to 8x EBITDA multiple. This is the "commodity canyon" where competition is fierce, margins are compressed by labor arbitrage, and customer switching costs are low.

However, if you own a specialized Oracle Enterprise Performance Management (EPM) practice, the math changes materially. According to 2025 M&A transaction data, specialized IT consulting firms are trading at a median of 13.6x EBITDA, significantly outpacing generalist software development firms (12.0x) and standard MSPs.

Why the massive delta? It comes down to the Specialization Premium. Acquirers—specifically Private Equity sponsors—are no longer paying for "capacity." They are paying for capability that is hard to replicate. An Oracle EPM practice doesn't just install software; it engineers the financial brain of the CFO. This creates a defensive moat that generalist firms cannot cross.

The Multiplier Effect of the "Office of the CFO"

When you sell to the CIO, you are often a line item in a cost center. When you sell to the CFO (as EPM practices do), you are a strategic partner in value creation. This distinction drives three key valuation levers:

- Higher Bill Rates: Specialized EPM consultants command $250-$400/hour, compared to $125-$175 for generalist developers.

- Stickiness (NRR): Once an EPM system is installed, it becomes the system of record for financial truth. Replacing it is open-heart surgery. This leads to Net Revenue Retention (NRR) benchmarks of 110-120% for top-tier practices.

- Recession Resilience: In a downturn, companies cut R&D (generic dev) but they increase spend on forecasting and scenario planning (EPM).

For a deeper dive on how to position these financials during an exit, review our guide on 15 EBITDA Add-Backs PE Firms Will Actually Accept.

You aren't selling code. You are selling the CFO's ability to sleep at night during earnings season. That is why this expertise commands a 13x multiple while generic dev shops fight for 7x.

The "Moat" Metrics: What Buyers Are Actually Buying

You might think buyers are acquiring your client list. They aren't. In the Oracle EPM space, they are acquiring Intellectual Property and Process Maturity. The difference between a 10x exit and a 14x exit usually comes down to whether your revenue is tied to people or platforms.

1. The Accelerator Advantage

Top-quartile EPM practices don't start from scratch. They bring proprietary "accelerators"—pre-built modules for industry-specific financial modeling (e.g., "Oil & Gas Capex Planning" or "Retail Store Labor Forecasting"). These assets reduce delivery risk and improve margins. If your firm can demonstrate that 30% of project delivery is automated via proprietary IP, you move from a "Services" valuation bucket toward a "Tech-Enabled" bucket, creating immediate multiple expansion.

2. The Retention Reality

In 2025, Oracle was once again named a Leader in the Gartner Magic Quadrant for Financial Planning Software, with 99% of customers willing to recommend. This ecosystem stability allows EPM practices to forecast revenue with high accuracy. Buyers scrutinize your Revenue Quality: Is it one-off implementations, or have you successfully attached high-margin Managed Services contracts post-go-live?

Firms that convert implementation projects into multi-year "EPM Managed Support" contracts (trading at 50%+ gross margins) are the ones hitting the 13x+ multiples. This shift from "hunting" to "farming" is critical. To prove this transferability to a buyer, you must have your delivery processes locked down. See why in our analysis: The Transferability Premium: Why Acquirers Pay 2x More for Documented Processes.

The Deal Killers: Why EPM Deals Fail in Diligence

Despite the high demand, I see Oracle EPM deals fall apart in Quality of Earnings (QofE) due to specific, avoidable red flags. The premium valuation comes with premium scrutiny.

1. The Contractor Concentration Trap

Many EPM shops run lean, relying on a bench of high-priced independent contractors (1099s) to flex up for big projects. While this protects margins in the short term, it destroys Enterprise Value. PE buyers view 1099 revenue as high-risk. If 40% of your delivery capability walks out the door the day after the deal closes, your multiple will be haircut accordingly. Rule of Thumb: You need a W-2 to 1099 ratio of at least 3:1 to defend a premium multiple.

2. Customer Concentration (The "Whale" Problem)

Because EPM projects are expensive ($500k-$2M+), it is common for a small firm to have one client representing 30-40% of revenue. In generic IT, this is a problem. In niche EPM, it is a disaster. If that client is dependent on a single partner (you), the buyer will structure the deal with a heavy earnout, transferring the risk back to you. You must diversify your revenue base 12-18 months before going to market.

3. The "Hero" Dependency

If the founder is the only one who can architect the solution or close the sale, the business is unsellable. EPM is technical; buyers need to know the brain trust extends beyond the C-suite. For more on preparing your financials for this level of scrutiny, read Why Your EBITDA Adjustments Will Get Rejected in Due Diligence.

The Bottom Line: The market for Oracle EPM practices is hot, but it is discerning. You are selling the "CFO's Peace of Mind." Ensure your metrics, your team structure, and your IP reflect that value proposition.