The practical answer

- Short answer

- Why Databricks partners with MLOps and GenAI capabilities trade at 14x EBITDA while generalist migration shops stall at 8x. A 2026 valuation diagnostic for PE sponsors.

- Best fit

- Industry: Private Equity / Technology Services. Function: M&A / Corporate Development

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 14x Average EBITDA multiple for Databricks partners with >40% MLOps revenue mix (2026).

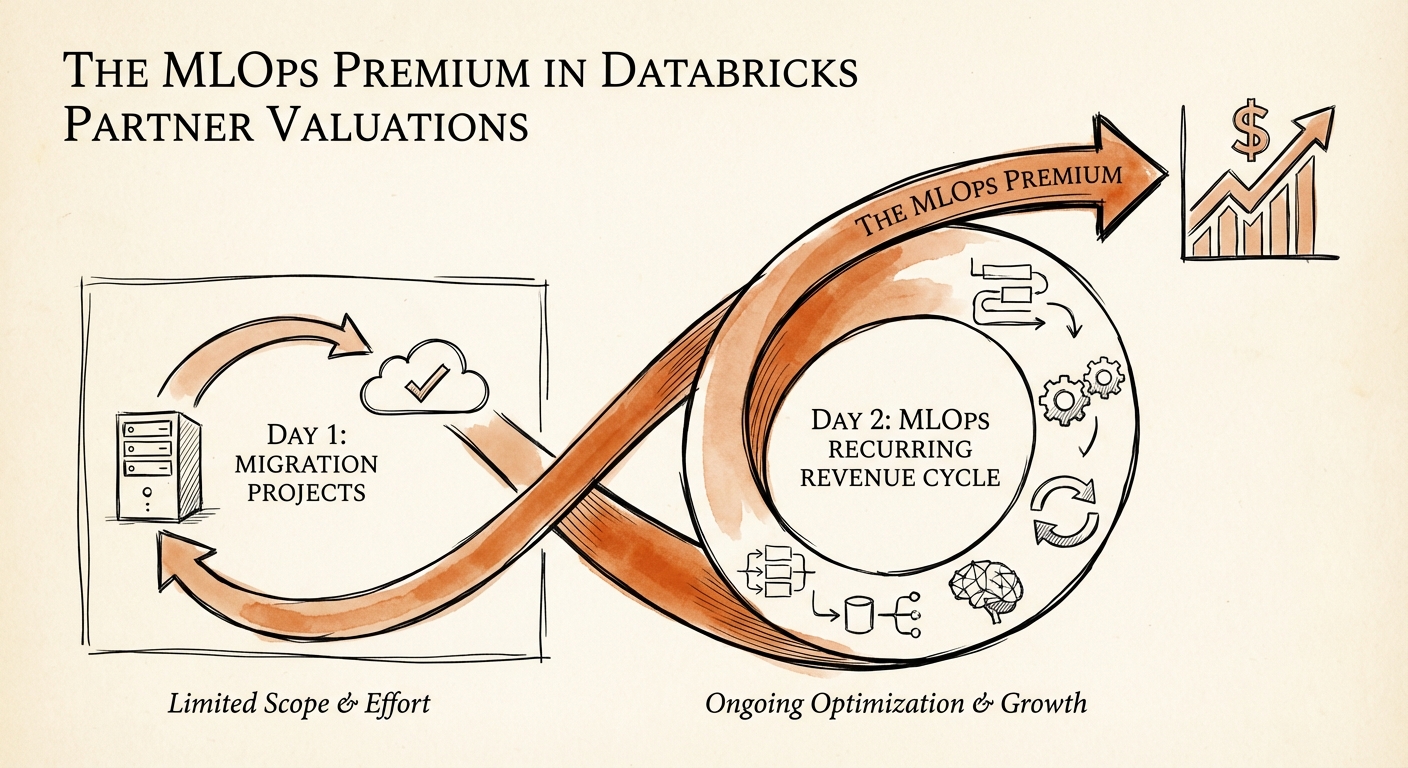

The Great Bifurcation: Migration Shops vs. Model Operators

In 2024, the Databricks partner ecosystem was a rising tide that lifted all boats. If you could migrate a legacy Hadoop cluster to the Lakehouse or implement Unity Catalog, you were growing at 40% year-over-year. Private Equity firms paid 10x-12x EBITDA for these "modern data stack" facilitators, betting that the migration wave would last a decade.

By early 2026, that wave crested. With Databricks hitting $4.8B in revenue and a $134B valuation (Series L), the ecosystem has matured—and bifurcated. The market no longer pays a premium for "lift and shift" services. Migration is now a commodity, automated by tools and low-cost delivery centers. The premium has shifted entirely to the "AI" side of "Data + AI."

Our Q1 2026 valuation analysis reveals a stark divide. Generalist Databricks partners—those focused on ETL, pipeline migration, and core data engineering—are trading at 6x-8x EBITDA. They are viewed as "body shops" with project-based revenue that resets every January 1st. In contrast, MLOps-specialized partners—firms that operationalize MosaicML models, manage "Day 2" generative AI lifecycles, and own the production serving layer—are commanding 12x-16x EBITDA.

The reason is "Revenue Quality." A migration project has a definitive end date. An MLOps contract involves continuous model monitoring, drift detection (using tools like MLflow), and retraining pipelines. It is sticky, recurring, and technically defensive. Acquirers aren't buying the one-time implementation; they are buying the long-tail operational dependence of the Global 2000.

In 2026, nobody pays 14x for a firm that just moves tables from on-prem to the cloud. The premium is for the team that keeps the GenAI models from hallucinating in production.

The "Day 2" Problem: Why GenAI PoCs Don't Drive Exit Value

In 2025, every Databricks partner claimed to have a Generative AI practice. They built RAG (Retrieval-Augmented Generation) chatbots and fine-tuned Llama models for clients. But 90% of these projects were "Day 1" builds—Professional Services revenue that looked great on the P&L but failed to create lasting enterprise value.

The valuation premium exists only for partners who solve the "Day 2" problem. Day 2 is when the model breaks. It is when data drift degrades performance, when vector indices need re-indexing, and when governance policies in Unity Catalog need to be enforced on model inference endpoints.

Partners who have productized this operational layer—often through proprietary IP built on top of the Databricks Data Intelligence Platform—are seeing a distinct shift in their revenue mix. The "Model-to-Engineer Ratio" has become a key due diligence metric:

- Low Valuation (6x): 10 Data Engineers for every 1 ML Engineer. Revenue is driven by cleaning data.

- High Valuation (14x): 3 Data Engineers for every 1 ML Engineer. Revenue is driven by keeping models alive in production.

We are seeing "Brickbuilder" solutions focused on industry-specific GenAI operations (e.g., "Clinical Trial Protocol Generation" or "Manufacturing Predictive Maintenance") trading at the highest multiples. These aren't just services; they are verticalized platforms that use Databricks as the underlying engine.

The 2026 Diagnostic: Is Your Databricks Practice "Exit Ready"?

For Private Equity sponsors holding Databricks service partners, the goal is to pivot from "Capacity" to "Capability" before the exit process begins. A high-revenue practice with low strategic value is a prime candidate for a multiple compression during Quality of Earnings (QofE).

Use this diagnostic to assess your portfolio company's positioning:

1. The MLOps Revenue Threshold

Metric: What percentage of revenue is derived from post-deployment model management (MLOps)?

Benchmark: <15% signals a project-based shop (8x EBITDA). >40% signals a recurring-revenue operational partner (14x EBITDA).

2. The MosaicML / GenAI Certifications

Metric: Ratio of "Generative AI" accredited consultants to generic "Data Engineer Associate" certifications.

Benchmark: A healthy premium practice maintains a 1:4 ratio. If your team is 95% generic Spark engineers, you are competing in a race to the bottom on rate cards.

3. The "Brickbuilder" IP Factor

Metric: Do you have a validated Databricks Brickbuilder Solution for AI/ML (not just migration)?

Analysis: Acquirers in 2026 are paying for speed-to-revenue. A validated accelerator that reduces GenAI deployment time by 50% validates the "Tech-Enabled" narrative and defends against the "Staff Augmentation" discount.