The practical answer

- Short answer

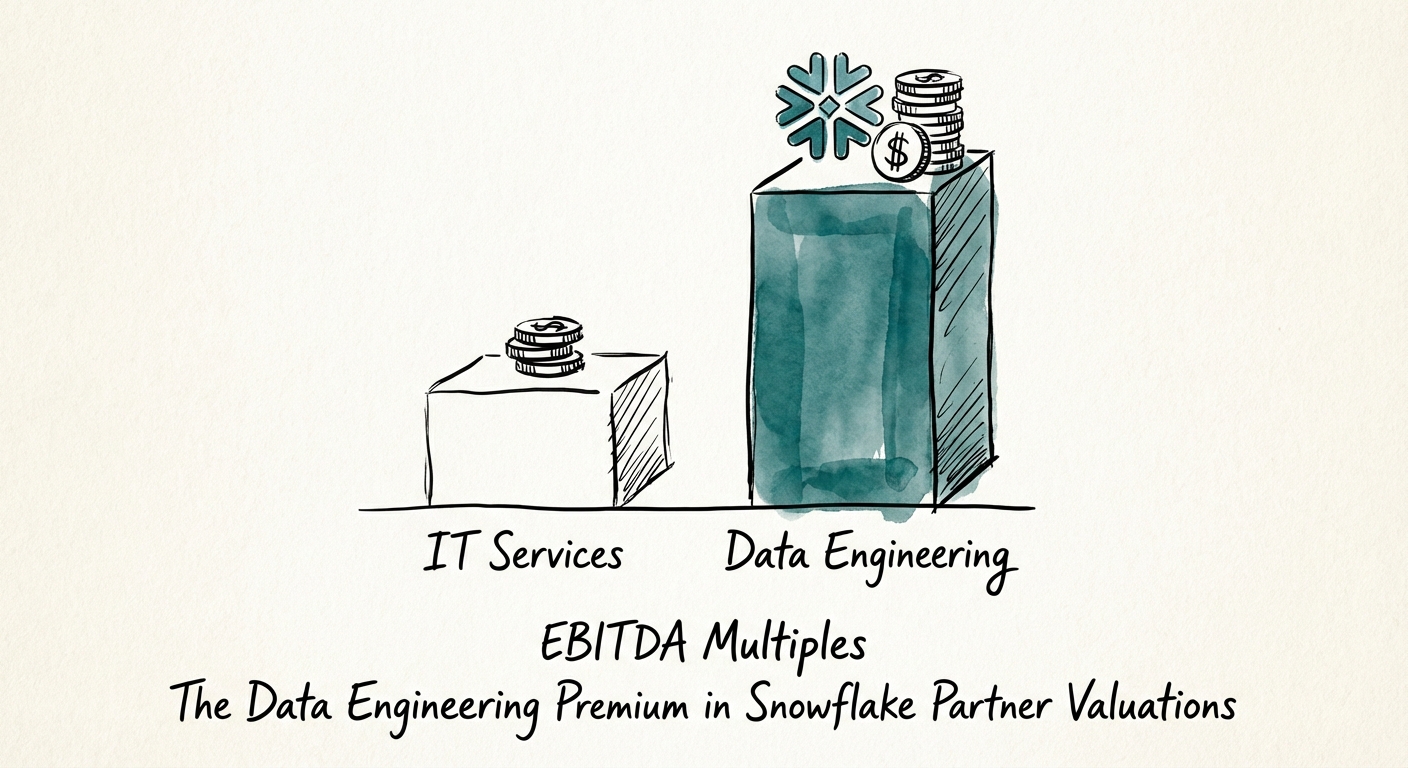

- Why specialized data engineering firms command 14x EBITDA multiples while generalist analytics shops stall at 8x. A valuation diagnostic for PE investors.

- Best fit

- Industry: Private Equity / Technology Services. Function: M&A Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 14x Average EBITDA multiple for specialized Data Engineering firms in 2026, driven by GenAI infrastructure demand.

The Valuation Bifurcation: Analysts vs. Architects

In the 2024-2025 vintage of professional services roll-ups, private equity firms learned a painful lesson: not all "data" revenue is created equal. The market has bifurcated. On one side, we see generalist "Data & Analytics" consultancies—firms primarily focused on building PowerBI dashboards, Tableau visualizations, and ad-hoc SQL reporting—struggling to break the 8x EBITDA ceiling. On the other, specialized Data Engineering firms—those building the underlying Snowflake infrastructure, data pipelines, and "clean core" required for GenAI—are commanding multiples in the 12x to 14x range.

This premium exists because the "Analyst" model is fundamentally a staff augmentation business with low barriers to entry. A dashboard is a deliverable; it expires the moment the business logic changes. A data pipeline is infrastructure; it is the plumbing that powers the enterprise. Snowflake partner valuations are now driven entirely by this distinction. Buyers are no longer paying for the ability to visualize data; they are paying for the technical capability to move, clean, and govern it at scale.

The Commoditization of the Dashboard

The rise of Large Language Models (LLMs) has accelerated the commoditization of the "Data Analyst" role. AI agents can now write SQL queries and generate visualizations faster than a junior consultant. Consequently, firms built around "insights as a service" are seeing margin compression as clients refuse to pay $175/hour for work that Copilot can do in seconds. In contrast, the engineering required to feed those models—the complex orchestration of dbt, Airflow, and Snowflake Snowpark—has become significantly more valuable. This is the "Engineering Moat."

A dashboard is a deliverable; it expires the moment the business logic changes. A data pipeline is infrastructure; it is the plumbing that powers the enterprise. Buyers pay for the plumbing.

The Engineering Moat: Why Infrastructure Commands a Premium

Valuation is a proxy for replaceability. A dashboard shop can be replaced by a new vendor in 30 days. Replacing a firm that designed and manages your core data warehouse architecture is a multi-year, high-risk endeavor. This stickiness drives the Snowflake consumption model, where the service provider effectively owns the client's ability to operate.

Our analysis of 2025 deal data highlights three key drivers of the Data Engineering Premium:

- Revenue Quality: Engineering projects typically have 12-24 month roadmaps (migration, modernization, GenAI readiness) versus the 3-6 month cycles typical of analytics projects.

- Talent Scarcity: The billing rate differential is widening. Senior Data Engineers with Python/Spark/Snowpark expertise now command bill rates of $225-$300/hour, compared to $150-$185/hour for Senior Data Analysts. This translates directly to higher gross margins per head.

- The GenAI Wedge: You cannot deploy Agentic AI on dirty data. PE buyers know that every portfolio company needs a "data foundation" before they can leverage AI. Data Engineering firms are the gatekeepers of this foundation.

The "Body Shop" Discount

Many PE-backed platforms mistakenly believe they are buying engineering capabilities when they are actually acquiring low-margin staffing ops. If your target firm's primary revenue source is "resources" governed by client managers, you are buying a body shop. True data cloud value comes from "managed outcomes"—where the firm owns the architecture and the delivery risk. Body shops trade at 6x-8x; Outcome-based engineering firms trade at 12x+.

The Diagnostic: Do You Own a Pipe Builder or a Dashboard Builder?

For Operating Partners and PE Sponsors, distinguishing between these two profiles during due diligence or value creation planning is critical. Use this diagnostic framework to assess your portfolio's position.

1. The Ratios

- Engineer-to-Analyst Ratio: High-value firms maintain a ratio of at least 2:1 (Engineers to Analysts). If your firm has 50 analysts and 10 engineers, you are an analytics shop, not an engineering firm.

- Revenue per Delivery Head: Engineering-led firms should generate $280k - $320k annually per delivery employee. Analytics shops typically stall at $220k due to lower bill rates and higher bench time between short projects.

2. The Tech Stack

Audit the toolchain. If the team's primary tools are PowerBI, Tableau, and Excel, you have a visualization firm. If the primary tools include dbt (data build tool), Terraform, Python, and Airflow, you have an engineering asset. The presence of technical debt remediation services is also a strong indicator of engineering maturity.

3. The "Consumption" Metric

Ask: "Do our projects directly drive Snowflake credit consumption?" Engineering projects (ingestion, transformation) drive consumption. Analytics projects merely read what has already been consumed. In the Snowflake ecosystem, partners who drive consumption (ACR) are rewarded with better leads, higher tier status, and ultimately, higher exit multiples.