The practical answer

- Short answer

- Why UiPath Diamond partners trade at 6x EBITDA while specialized 'Agentic' automation firms command 14x. A 2026 diagnostic for founders and PE sponsors.

- Best fit

- Industry: Intelligent Automation / RPA. Function: M&A Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 12.8x Median EBITDA multiple for PE-backed Tech Services deals in North America (2025), significantly higher than the 8.6x paid by corporate acquirers.

The 'Diamond' Trap: Why Volume Doesn't Equal Value

In the UiPath ecosystem, 'Diamond' status is the visible badge of honor. It signals scale, technical competency, and—crucially for UiPath's sales leadership—revenue volume. But for a Private Equity buyer looking at your firm in 2026, Diamond status is a double-edged sword. While it proves you have a seat at the table, it often masks a business model built on the wrong kind of revenue.

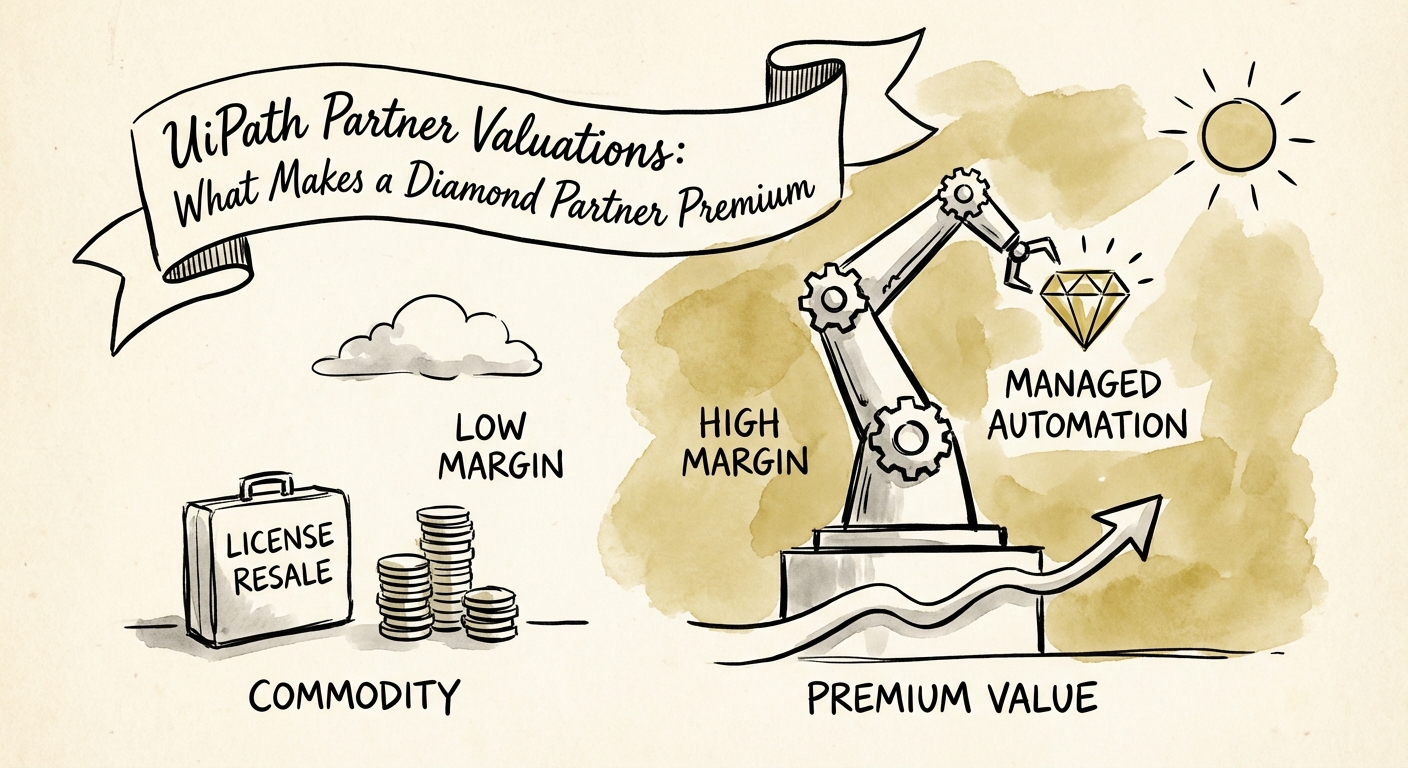

The trap lies in the requirements. To maintain Diamond status, partners often over-rotate on license resale to hit top-line targets. While this pleases the vendor, it poisons your valuation. License resale is a low-margin (8-15%), non-differentiated game. If 40% of your revenue comes from passing through UiPath licenses, your blended gross margin is likely sitting below 35%. In the eyes of an acquirer, you aren't a high-value consultancy; you're a low-margin distributor with a services arm.

We see a stark bifurcation in 2026 valuations:

- The 'Reseller' Diamond: High revenue ($20M+), low gross margins (<40%), and heavy reliance on license renewals. These firms trade at 5x–7x EBITDA.

- The 'Platform' Diamond: Moderate revenue ($10M–$15M), high gross margins (55%+), and a revenue mix dominated by high-end advisory and proprietary IP. These firms trade at 12x–14x EBITDA.

The lesson for founders is clear: Don't let the pursuit of the badge destroy the quality of your earnings.

Diamond status is a volume game. Premium valuation is a value game. If you confuse the two, you'll build a $30M company that sells for $10M.

The 'Agentic' Premium: The New 14x Standard

The automation market has shifted dramatically from 'Robotic Process Automation' (RPA) to 'Agentic Automation.' In 2024, a bot that moved data from Excel to SAP was valuable. In 2026, that is a commodity. The premium valuation now belongs to partners deploying GenAI Agents that make decisions, handle exceptions, and navigate unstructured data.

Our research into 2025/2026 deal flow indicates that acquirers are paying a massive premium for 'Agentic DNA.' This means partners who have moved beyond 'lift and shift' implementation and have built proprietary Industry Accelerators—pre-packaged agentic workflows for specific verticals like Healthcare Claims Processing or FinTech KYC.

The Valuation Hierarchy

Where does your firm sit on the ladder?

- Level 1: Body Shop (4x-6x EBITDA). You sell hours. Your developers build basic bots. You compete on rate card.

- Level 2: Managed Automation (8x-10x EBITDA). You sell outcomes. You have long-term 'Automation-as-a-Service' contracts. You manage the bots you build.

- Level 3: IP-Led Agentic (12x-14x EBITDA). You sell a platform. You have the UiPath 'Fast Track' badge for Agentic Automation. You own intellectual property that accelerates deployment by 50%.

The 'Agentic Premium' is real because it breaks the linear relationship between revenue and headcount. If you can deploy a $500k ARR project with a team of three because your IP does the heavy lifting, your margins—and your multiple—expand significantly.

The 'Service Mix' Diagnostic: Resale vs. Recurring

To determine if you are ready for a premium exit, you must audit your revenue quality. PE firms are scrutinizing the 'Service Mix' more than ever. The most dangerous metric for a UiPath partner is a high License-to-Service Ratio that isn't backed by Managed Services.

If you sell $1M in licenses, you should be generating at least $3M in services. But the type of service matters.

Project Revenue (One-Time): 'We built the bot.' This is lumpy, unpredictable, and creates a 'hamster wheel' sales motion. It is valued at ~1x Revenue or 6x EBITDA.

Managed Services (Recurring): 'We keep the automation running, secure, and optimized.' This is sticky, high-margin, and predictable. It is valued at ~2.5x Revenue or 10x-12x EBITDA.

To unlock the 14x exit, your revenue mix needs to look like this:

- License Resale: < 20% of Gross Profit (Pass-through only)

- Strategic Consulting: 30% of Gross Profit (High rates, tip of the spear)

- Managed Services / IP: > 50% of Gross Profit (The valuation driver)

Diamond status gets you the meeting. Your Service Mix gets you the check. Stop optimizing for the vendor's tier requirements and start optimizing for the buyer's P&L.