The practical answer

- Short answer

- New data on Databricks partner valuations. Why 'Brickbuilder' specialists command 14x EBITDA while generalist SIs stall at 6x. 2026 growth benchmarks.

- Best fit

- Industry: Data & AI Consulting. Function: M&A Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 13.6x Average EBITDA multiple for Databricks partners with validated Brickbuilder IP and >40% managed services mix.

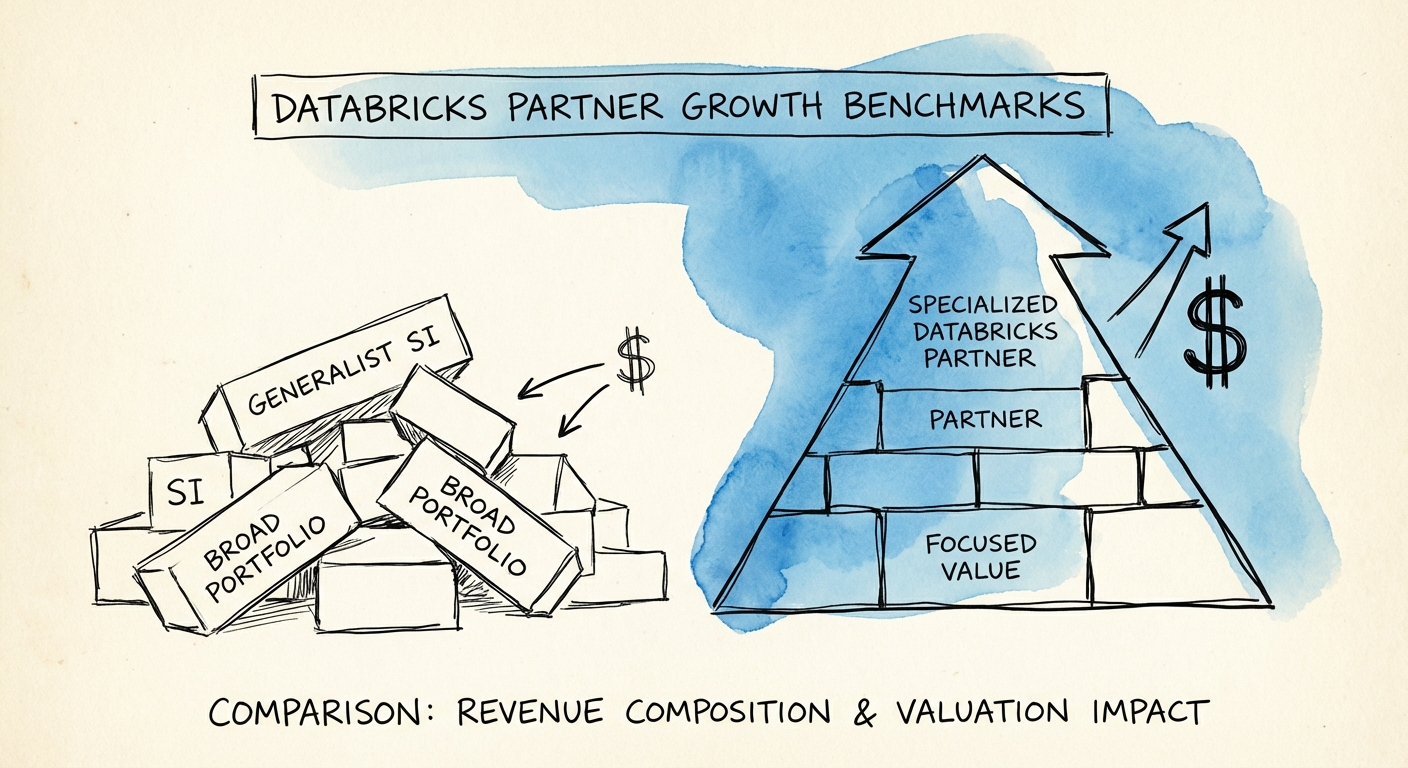

The 'Generalist' Discount vs. The 'Lakehouse' Premium

The 2026 valuation landscape for Databricks partners has bifurcated into two distinct asset classes: Capacity Providers and Data Intelligence Platforms. Our analysis of Q4 2025 deal flow reveals a stark reality: generalist systems integrators (SIs) that treat Databricks as just another distinct endpoint in a broader cloud practice are trading at a significantly compressed multiple compared to specialized firms.

The Valuation Bifurcation

While Databricks itself grows at 55%+ annually (reaching $4.8B ARR), the partner ecosystem is experiencing a 'winner-take-most' dynamic. Generalist firms are seeing EBITDA multiples compress to 6x-8x, driven by the commoditization of basic pipeline engineering. In contrast, partners with Brickbuilder solutions and deep vertical IP are commanding 12x-14x EBITDA multiples.

The market is signaling that access to talent is no longer a differentiator; acceleration of time-to-value is. Private equity buyers are specifically screening for partners who have moved beyond 'billable hours' to 'billable outcomes,' utilizing the Databricks Data Intelligence Platform to own entire vertical workflows rather than just the underlying infrastructure.

In 2026, 'Certified' is the floor. 'Specialized' is the ladder. But 'integrated IP' is the only elevator to a premium exit.

The $10M to $50M Scaling Trap

Data from the 2025 ecosystem expansion shows that 50% of Databricks partners still have fewer than 100 employees. This fragmentation highlights a critical ceiling: the $15M-$20M revenue mark where founder-led sales and 'hero architect' delivery models break.

Why Partners Stall at $20M

Scaling beyond $20M requires a fundamental shift in the operating model. The firms that successfully cross this chasm share three specific characteristics:

- Specialization over Generalization: They don't just 'do Databricks'; they own 'Financial Services Risk Modeling on Lakehouse' or 'Retail Demand Forecasting with Mosaic AI.'

- Brickbuilder as a GTM Motion: They use validated Brickbuilder solutions not just for delivery efficiency, but as the primary wedge for customer acquisition, reducing CAC by 40%.

- Managed Services Transition: They have successfully pivoted from 80% project revenue to a 40/60 split, launching 'Data Estate as a Service' offerings that secure the 140% NRR investors crave.

Without these structural pivots, partners find themselves in the 'Generalist Trap': competing on rate cards against Global SIs while lacking the scale to win prime vendor status.

Exit Readiness: The 'Asset' Test

For founders looking to exit in the 2026-2027 window, the definition of 'quality revenue' has tightened. Acquirers are scrutinizing the Unity Catalog adoption within your client base as a proxy for account stickiness. A partner whose clients use Databricks merely for ETL is viewed as replaceable. A partner whose clients rely on the firm's IP to govern AI models via Unity Catalog is viewed as critical infrastructure.

The New Due Diligence Checklist

To command the 13.6x premium, your data room must demonstrate:

- IP Attribution: What % of revenue is attached to proprietary Brickbuilder solutions? (Target: >30%)

- Consumption Influence: Can you prove your managed services drive underlying DBU (Databricks Unit) consumption growth?

- Vertical Depth: Do you have referenceable logos in a single high-value vertical (e.g., HLS, Finserv) that proves dominance?

The era of the 'generalized data shop' is over. The next wave of capital is flowing exclusively to partners building the intelligence layer on top of the Lakehouse.