The practical answer

- Short answer

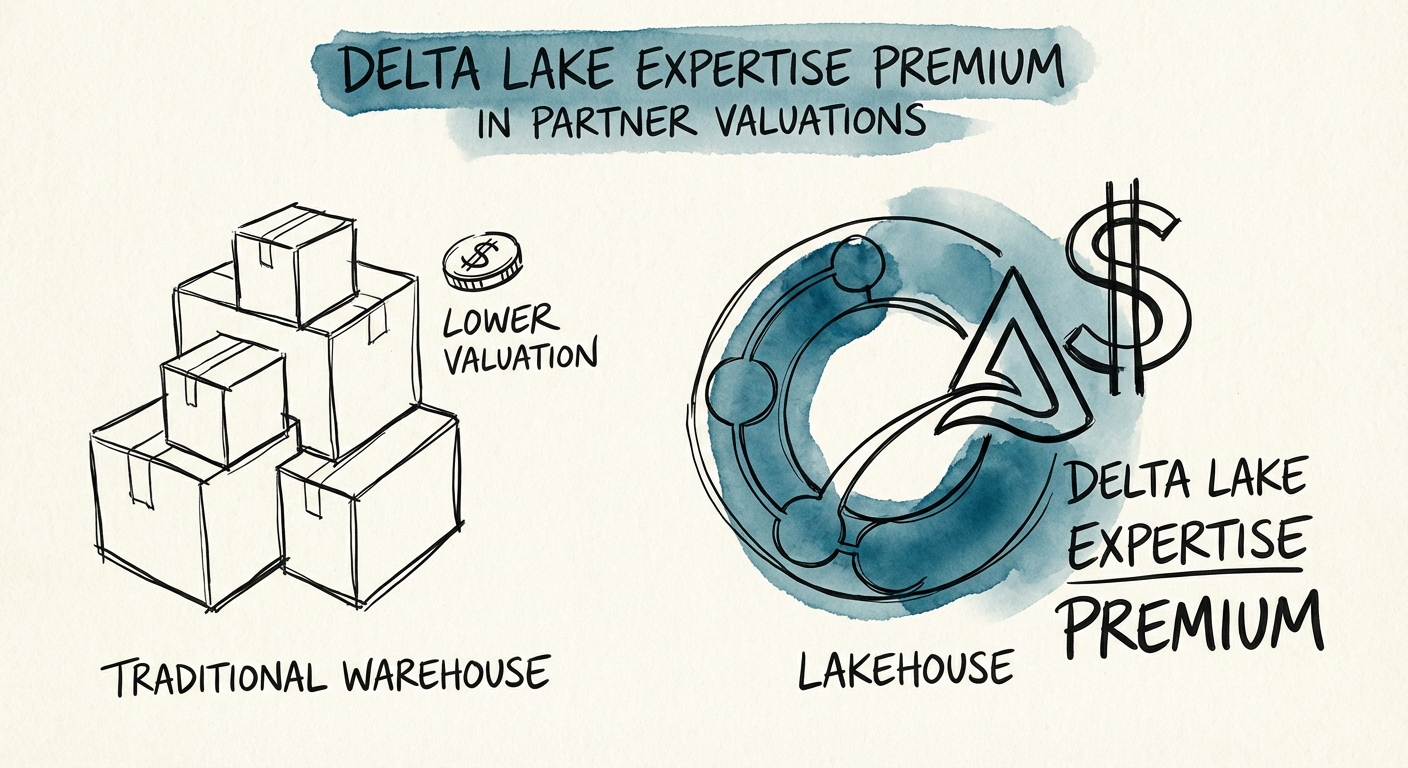

- Why Databricks and Delta Lake partners trade at 14x EBITDA while generalist data firms stall at 8x. M&A benchmarks and exit strategy for data consultancies.

- Best fit

- Industry: Technology Services. Function: M&A Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- Premium Average EBITDA multiple for specialized 'Lakehouse' data consultancies in 2025/26.

The 'Open Format' Arbitrage: Why the Market Pivoted

For the last decade, the data services valuation playbook was simple: migrate customers from on-premise servers to cloud data warehouses (Snowflake, Redshift, BigQuery). Partners who did this efficiently traded at healthy 10-12x EBITDA multiples. But in 2026, that trade is crowded, and the "lift and shift" arbitrage is dead.

The market has bifurcated. On one side, you have generalist systems integrators (SIs) pushing SQL-based migrations. These firms are seeing bill rates compress as AI automates code conversion. On the other side, you have "Lakehouse-Native" consultancies specializing in open table formats like Delta Lake and Apache Iceberg.

Why the premium? Because enterprise buyers—and the PE firms acquiring them—have realized that proprietary data warehouses are the new "mainframe" lock-in. The smart money is moving to open architectures where data sits in low-cost object storage (S3/ADLS) but behaves like a structured warehouse. Partners who possess the complex engineering talent to build this "Zero-Copy" architecture are solving a solvency-level problem for CIOs: how to enable GenAI on unstructured data without duplicating it into an expensive warehouse.

The Valuation Gap

Our analysis of 2024-2025 transaction data reveals a widening chasm. Generalist data shops are trading at 8.1x EBITDA, dragged down by commoditized ETL work. Meanwhile, firms with verifiable IP and certified expertise in Databricks/Delta Lake architectures are commanding premium EBITDA multiples. This isn't just a "growth" premium; it's a "scarcity" premium.

The valuation gap between genuine AI infrastructure and cosmetic AI features has widened dramatically. Companies with real machine learning moats are commanding 8–12x revenue multiples. Those with ChatGPT wrappers are lucky to get 4x.

The Technical Moat: SQL vs. Spark

The primary driver of this valuation delta is the barrier to entry for talent. Generalist data practices rely heavily on SQL skills—a talent pool that is deep, global, and increasingly commoditized by LLMs that can write SQL queries faster than humans.

Delta Lake expertise, however, requires a fundamental shift from "Database Administration" to "Data Engineering." It demands proficiency in Apache Spark, Scala, or Python, and a deep understanding of file compaction, Z-ordering, and partition pruning. You cannot "bootcamp" a junior SQL analyst into a Spark optimization expert in six weeks.

This talent scarcity creates a defensible moat. PE buyers know that acquiring a 50-person Databricks partner is effectively buying a high-performance engineering team that would take 24 months to recruit organically.

Revenue Quality: Managed Governance vs. Migration

The second valuation driver is the nature of the revenue. Generalist migrations are "one-and-done" projects. Once the data is in Snowflake, the partner's job is often finished.

In a Lakehouse architecture, the partner often installs the "control plane"—the Unity Catalog or governance layer that manages access across the entire data estate. This positions the partner as the guardian of the Data & AI Platform, not just the movers of the data. This stickiness converts volatile project revenue into "quasi-recurring" managed services revenue, which acquirers value at 2x-3x revenue (vs. 1x for project services).

Strategic Action: Positioning for the Exit

If you are a mid-market data consultancy looking to capture this premium, you must pivot your narrative in the CIM (Confidential Information Memorandum) from "Migration" to "Modernization."

- Audit Your Revenue Mix: Separate "Legacy ETL" revenue from "Modern Data Platform" revenue. Buyers will blend your multiple if you don't clearly demarcate the high-value work.

- Quantify the "AI Readiness" Impact: Show how your Delta Lake implementations are the direct precursor to your clients' GenAI initiatives. In 2026, "Data Infrastructure" is valued as "AI Infrastructure" if the story connects.

- Document the IP: Do you have accelerators for ingesting data into Delta Lake? Do you have a framework for Unity Catalog implementation? Productizing your service delivery methodology is the fastest way to move from a 6x "body shop" valuation to a 12x "platform" valuation.

The window to claim this premium is open, but closing. As the Global Systems Integrators (GSIs) aggressively acquire specialized boutiques to fill their own skill gaps, the scarcity premium will eventually normalize. For now, owning the "Lakehouse" is the most profitable real estate in the data ecosystem.