The practical answer

- Short answer

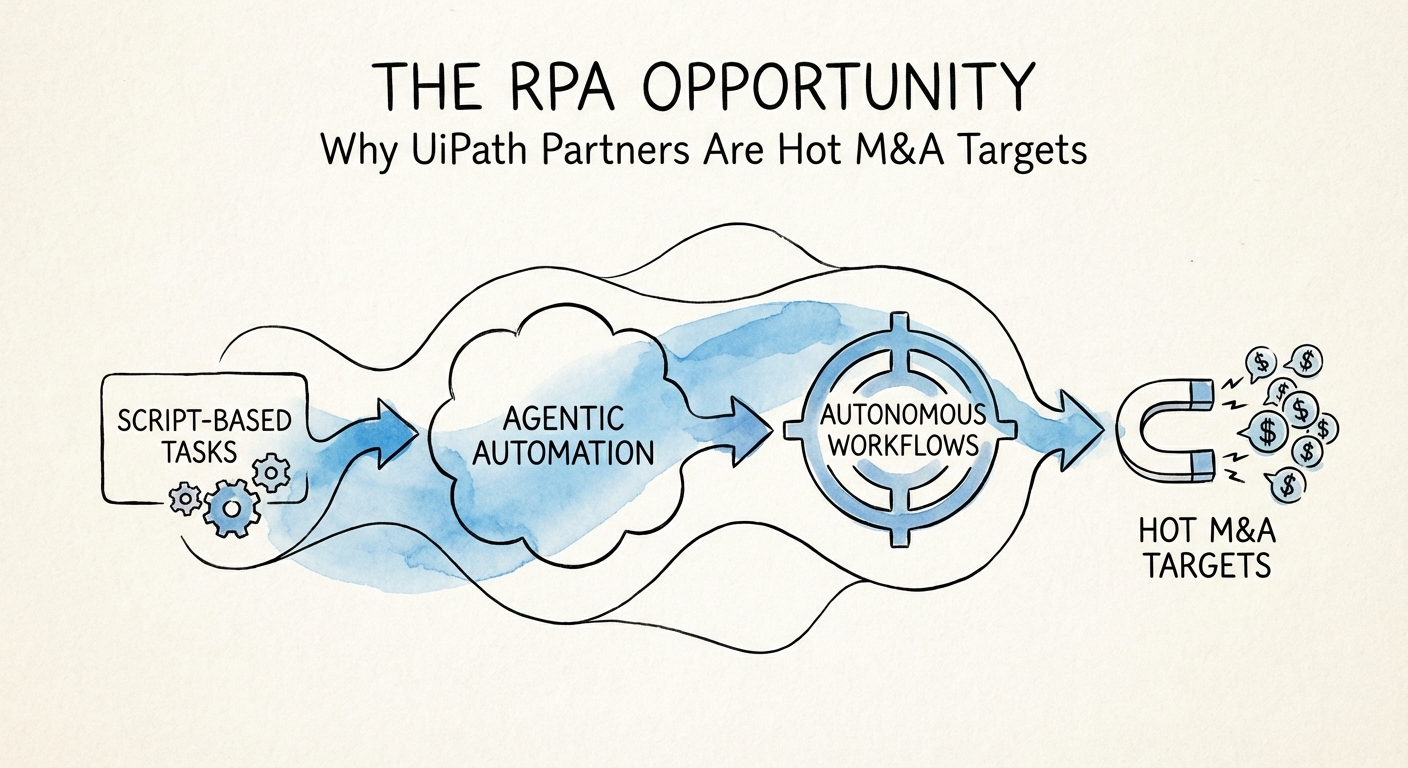

- Two UiPath partners, same revenue. One sells at 6x, the other at 14x. The difference isn't bot count — it's who owns the exception logic. Here's the diligence test.

- Best fit

- Industry: Intelligent Automation. Function: M&A Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 55% Gross Margins for 'Agentic' IP-led projects vs. 35% for standard implementation.

The screen-scraping math finally stopped working

For years the RPA services playbook was the same trade everywhere: hire a developer at $60 an hour, bill them at $180, and point them at someone's accounts-payable screen to automate a login and a copy-paste loop. It threw off real cash. It also produced nothing you could sell twice. Every bot was a custom artifact wired to one client's exact UI, and the day SAP repainted a button or a vendor changed its invoice template, that bot threw an exception and someone's billable hour came back to fix it. In 2026, buyers have figured out that this isn't a software business with margins — it's a staffing business with a logo. They're pricing it that way: 5x to 6x EBITDA.

What changed underneath is specific to where UiPath took the platform. With Autopilot and the agentic capabilities layered into the Business Automation Platform, the unit of value stopped being a script that follows a fixed path and became an agent that decides what to do when the path doesn't exist. A traditional bot processing invoices needs every exception pre-mapped — wrong PO number, missing tax line, duplicate submission — or it kicks the case to a human. An agent reads the messy invoice, reasons about which exception it is, and resolves it. That single difference is what separates a maintenance cost center from something a private equity firm will pay a premium to own.

The partners capturing that premium aren't the ones with the most bots in production. They're the ones who turned hard-won exception logic into reusable property — a pre-built claims-adjudication agent, a KYC remediation workflow, a revenue-cycle agent tuned for one vertical — and sell it again to the next client without rebuilding from zero. That's where the AI/ML expertise that buyers underwrite as a moat actually lives. Those firms post gross margins north of 55% against the roughly 35% a body-shop integrator earns reselling configured hours.

A bot that breaks every time a vendor changes an invoice layout is a maintenance liability you've labeled an asset. A buyer's diligence team finds that in the support tickets, not the pitch deck.

Same revenue line, eight turns apart

Put two UiPath partners side by side. Both did $8M last year. Both are profitable. One sells at 6x, the other at 14x, and the gap has almost nothing to do with the top line. It's about what a diligence team finds when it opens the books and the ticket queue.

The 6x firm bills by the project. Revenue is lumpy, it tracks headcount almost perfectly, and growth means recruiting — every new dollar requires a new warm body to deliver it. The support backlog is full of "bot broke after the client's system update" tickets, which means the install base is a liability disguised as recurring work. That profile gets priced against staffing-grade comps, not software comps — the same trap the industry-multiple data shows separating information services from labor businesses.

The 14x firm reads differently in three specific places:

- The revenue is metered, not invoiced. A healthcare payer doesn't buy "an implementation." It pays a monthly fee tied to claims processed, and that fee renews because pulling the agent out means rebuilding the workflow internally. Revenue you can forecast 12 months out underwrites a multiple that lumpy project revenue never will.

- The vertical is narrow on purpose. This firm doesn't "automate finance." It runs revenue-cycle management for mid-market dental DSOs, and it knows every payer rejection code in that niche. A generalist would need six months of unpaid learning to compete for that account — which is exactly the switching cost a buyer pays up for.

- The exception logic is theirs. When the source system changes, the agent adapts instead of failing, so net retention holds well above the churn levels that drag generalists down. The install base compounds value instead of generating tickets.

Why the fund pays more than the math seems to justify

There's a second buyer motive that pure cash flow doesn't capture, and Bain's read on AI in the PE portfolio names it plainly. A fund acquiring a specialized UiPath partner isn't only buying a consultancy — it's buying a deployable capability it can push across 30 other portfolio companies. The agent-architect team that built a dental-DSO revenue-cycle workflow can stand up an equivalent for the fund's manufacturing or logistics holdings. That portfolio-wide leverage is what justifies a number financial engineering alone can't reach.

The diligence question that sorts you into a bucket

With debt expensive and multiple expansion off the table, the returns funds chase in 2026 come from operating efficiency — which has pushed operational due diligence from a checkbox to a deciding factor. For a UiPath partner, that diligence converges on one uncomfortable question: when a client's underlying system changes, what happens to your automations and who pays for it?

If the honest answer is "they break and we bill to fix them," you're a staffing business with recurring maintenance, and the model will price you at 6x no matter how good last year looked. If the answer is "the agents adapt, and the workflow IP is ours," you're a strategic asset — useful standalone in the $24B+ hyperautomation market, and more useful still as a tool the fund can deploy across its other holdings to move EBITDA margins.

You don't have to wait for a banker to tell you which one you are. Pull your support tickets for the last 90 days and sort them: how many are exception-handling and break-fix versus genuine new scope? Then list what you'd ship to a brand-new client on day one — reusable agents and workflow IP, or a blank UiPath Studio project and a statement of work. If the first answer is "mostly break-fix" and the second is "blank project," you have a roadmap, and roughly eight turns of EBITDA riding on whether you execute it before you sell. Founders who keep selling hours and scripts are building a comfortable lifestyle business. Founders who package agentic workflows and vertical IP are building something a buyer competes to own.