The practical answer

- Short answer

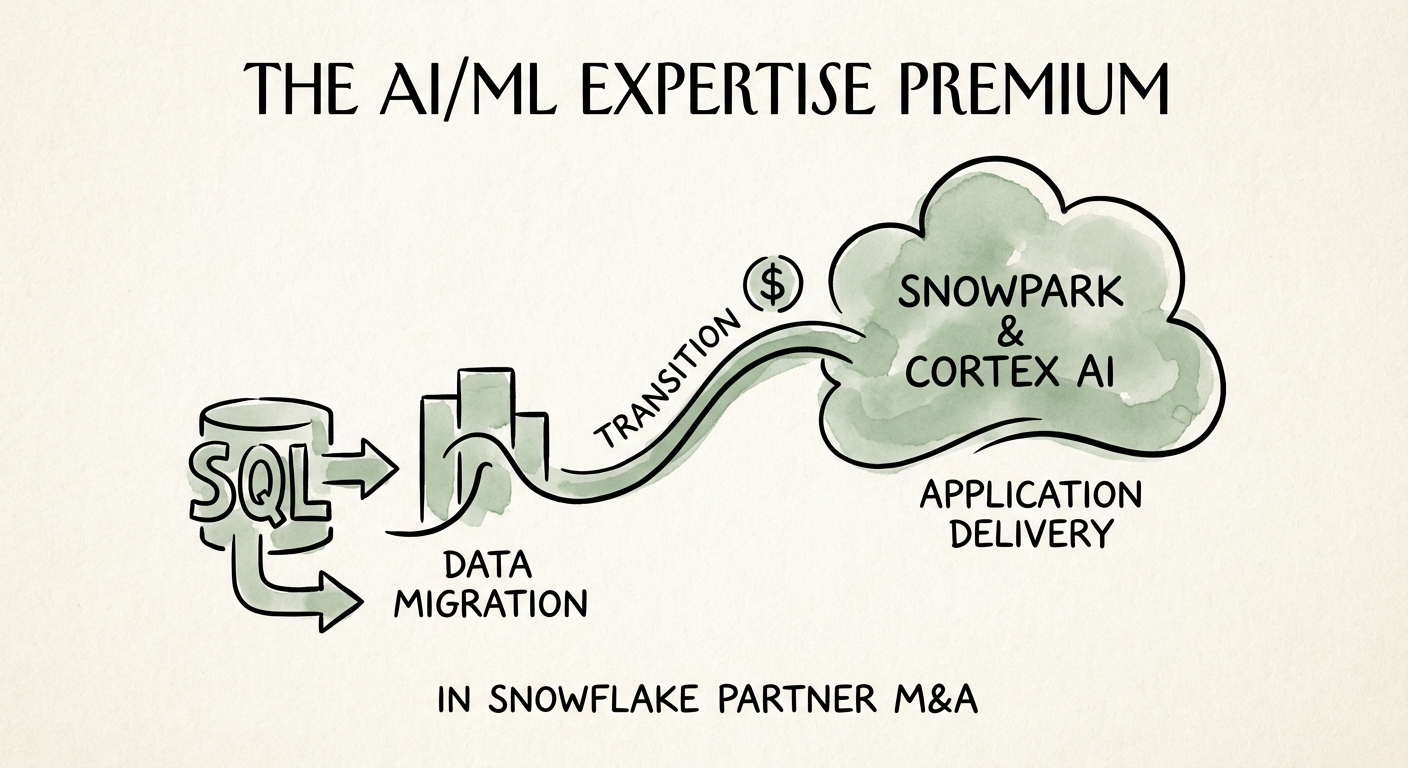

- Generalist Snowflake partners trade at 8x EBITDA while AI/ML specialists command 16x. Here is the valuation diagnostic for PE sponsors and founders.

- Best fit

- Industry: Technology Services. Function: Mergers & Acquisitions

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 16x Average EBITDA multiple for Snowflake partners with production-grade Snowpark & Cortex expertise (2026).

The Great Bifurcation: Pipeline Operators vs. Intelligence Architects

In 2023, the Snowflake partner ecosystem was a volume game. If you could migrate terabytes from on-premise Netezza or Teradata boxes to the Data Cloud, you had a business. Private equity buyers paid 10x-12x EBITDA for these "lift and shift" shops because the total addressable market (TAM) for cloud migration seemed infinite.

By 2026, that thesis has collapsed. The "migration arbitrage" is dead, commoditized by automation and hyperscaler incentives. Today, a generalist Snowflake partner focused on SQL migration and basic warehousing trades at 6x-8x EBITDA—a valuation "danger zone" that barely covers the risk of customer churn.

The capital has moved up the stack. A new class of partners—those specializing in Snowpark, Cortex, and Native Apps—is trading at 14x-16x EBITDA. These firms aren't just moving data; they are building intelligence products on top of it. They don't sell "hours" of data engineering; they sell "outcomes" via agentic workflows and predictive models. For PE Operating Partners, the distinction is binary: you are either owning the AI layer (and the premium) or you are competing on commodity rate cards.

The migration arbitrage is dead. Buyers today aren't paying for firms that move data; they're paying 16x for firms that turn that data into autonomous business decisions.

The "Cortex" Factor: What Drives the 8-Turn Gap?

Why is a Snowpark-native shop worth double a SQL-native shop? The answer lies in the stickiness of the workload and the scarcity of the talent.

Traditional data warehousing (EDW) is sticky, but it is a cost center. AI/ML workloads powered by Snowflake Cortex and Snowpark Container Services are revenue generators for the end client. When a partner implements a Generative AI solution that automates 40% of a client's customer support inquiries using Cortex Analyst, they aren't just a vendor; they are a strategic partner embedded in the P&L. This creates higher Net Revenue Retention (NRR), often exceeding 125% for AI specialists compared to 105% for generalists.

Furthermore, the supply/demand imbalance for Snowpark-certified engineers is acute. While thousands of consultants can write SQL, fewer than 5% of the ecosystem has production-grade experience with Python-based Snowpark pipelines or deploying LLMs via Container Services. Acquirers are not buying your backlog; they are buying your ability to execute on the "AI Data Cloud" roadmap that every Global 2000 CIO is funding in 2026. If your CIM (Confidential Information Memorandum) highlights "ETL jobs" instead of "Agentic AI," you have already lost the valuation war.

The Pivot: From Service Bureau to Data Product Studio

For PE sponsors holding a generalist Snowflake asset, the path to a 16x exit requires a radical 18-month pivot. You cannot "hiring freeze" your way to this premium; you must re-engineer the delivery model.

1. Productize via Native Apps

Stop hand-coding a bespoke build for every client. Package your most common industry-specific workflows (e.g., "Retail Demand Forecasting" or "Healthcare Claims Adjudication") into Snowflake Native Apps. This shifts revenue quality from non-recurring project work to quasi-recurring IP licensing, a key driver of the 16x multiple.

2. Audit Your "Data Gravity"

Generalists focus on storage; specialists focus on compute. Audit your customer base: what percentage of their consumption comes from Snowpark vs. standard warehouse compute? If Snowpark is under 10% of your managed spend, you are a legacy vendor. Set a KPI to drive 30% of client consumption via AI/ML workloads within 12 months.

3. The "Agentic" Talent Upgrade

Replace your bottom 20% of "SQL-only" engineers with Full-Stack Data Applications engineers who understand Streamlit and LLM orchestration. The market pays for the ability to build interfaces (apps), not just infrastructure (pipes). Your ability to demonstrate a "Cortex-First" methodology in due diligence will determine whether you exit at 8x or 16x.