The practical answer

- Short answer

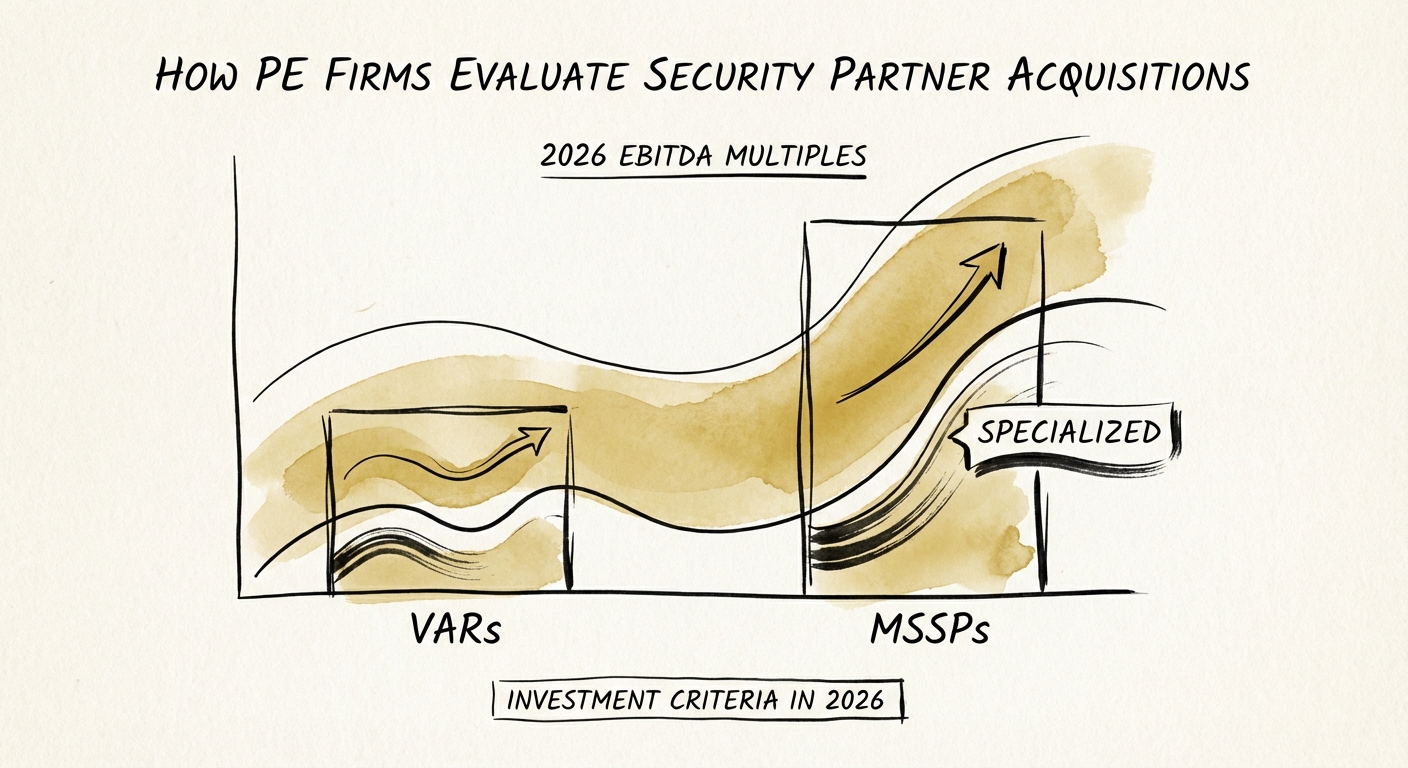

- Private Equity firms are paying 13.6x EBITDA for elite security partners while generalist VARs stall at 5x. Here is the 2026 due diligence framework for MSSP valuation.

- Best fit

- Industry: Private Equity. Function: Mergers & Acquisitions

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 13.6x Median EBITDA multiple for specialized, IP-led Security Partners in 2026.

The Valuation Bifurcation: Box Pushers vs. Risk Partners

In 2026, the Private Equity view of the cybersecurity channel has bifurcated into two distinct asset classes. On one side are the Value-Added Resellers (VARs), entities that primarily transact third-party hardware and software. Despite rebranding as "solutions providers," their revenue quality remains tied to vendor margins and renewal cycles. These firms are currently trading at 4x to 6x EBITDA, viewed largely as low-margin distribution endpoints with minimal intellectual property.

On the other side are the Specialized Managed Security Service Providers (MSSPs). These are not merely help desks with a security badge; they own the outcome of risk reduction. They command 13.6x EBITDA multiples because they have successfully transitioned from selling tools to selling "sleep insurance"—managed detection, response, and remediation (MDR) underpinned by proprietary workflows or technology. For Private Equity sponsors, the thesis is simple: hardware eventually commoditizes, but the complexity of managing threat landscapes only compounds. Consequently, capital is aggressively flowing toward partners who can demonstrate they are "Compliance-Ready" and capable of managing risk for the mid-market, rather than just reselling the tools to do so.

In 2026, we stopped buying 'resellers with a SOC.' If your revenue is 80% pass-through software, you're a bank, not a security company. We pay premiums for proprietary remediation workflows, not alert forwarding.

The "Quality of Revenue" Diagnostic: Three Tests That Kill Deals

When our team advises PE sponsors on security acquisitions, we apply a "Quality of Revenue" filter that goes beyond standard financial due diligence. The goal is to strip away the "managed services" marketing veneer and expose the operational reality.

1. The "Alert Factory" Test

We analyze the ratio of Events-to-Tickets-to-Remediations. Low-value MSSPs act as "alert factories," simply forwarding vendor alerts to the client’s internal IT team. This is a churn-prone model valued at roughly 6x EBITDA. High-value MSSPs filter 99% of noise and only escalate validated threats with specific remediation context—or handle the remediation themselves. If your analysts are just forwarding emails from CrowdStrike or SentinelOne, you are a reseller with a dashboard, not an MSSP.

2. The Gross Margin Stress Test

True MSSP revenue carries 50%+ gross margins. If we see "Managed Services" revenue lines with 25% margins, it indicates the firm is overly reliant on expensive senior talent to solve routine problems (staff augmentation) or is burying low-margin software resale costs within their services bundles. PE buyers punish this "blended margin" obscurity with a valuation discount.

3. The Concentration of Competency

In 60% of lower-middle-market security firms, the "proprietary process" actually lives in the head of a single CISO or Lead Architect. If that individual leaves post-close, the asset's value collapses. We measure this by the "Key Person Dependency" of the SOC: Can a Level 1 analyst execute a containment playbook without escalating to the founder? If the answer is no, the multiple contracts significantly.

The "Security Debt" Paradox: Auditing the Watchman

Perhaps the most ironic deal-killer in 2026 is the target's own security posture. PE firms are increasingly conducting "Inception-Level" Cyber Due Diligence—auditing the security of the security firm. We frequently find MSSPs running flat networks, sharing admin credentials, or lacking 2FA on their own internal management consoles.

This is not just a technical risk; it is an existential valuation risk. A security partner that gets breached is an asset that goes to zero overnight. Buyers are now pricing in a "Remediation Escrow"—often holding back 10-15% of the deal value until the target firm achieves SOC 2 Type II or ISO 27001 certification itself. The assumption that "we are secure because we are security pros" is no longer accepted in the data room.

For founders looking to exit, the path to a 13.6x multiple requires documenting "the machine": a standardized, defensible, and secure platform for service delivery that exists independently of any single "hero" employee.