The practical answer

- Short answer

- A private equity guide to valuing Workday partners in 2026. Analysis of 14.5x EBITDA multiples, AMS revenue mix benchmarks, and the specific due diligence risks that kill deals.

- Best fit

- Industry: Private Equity. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

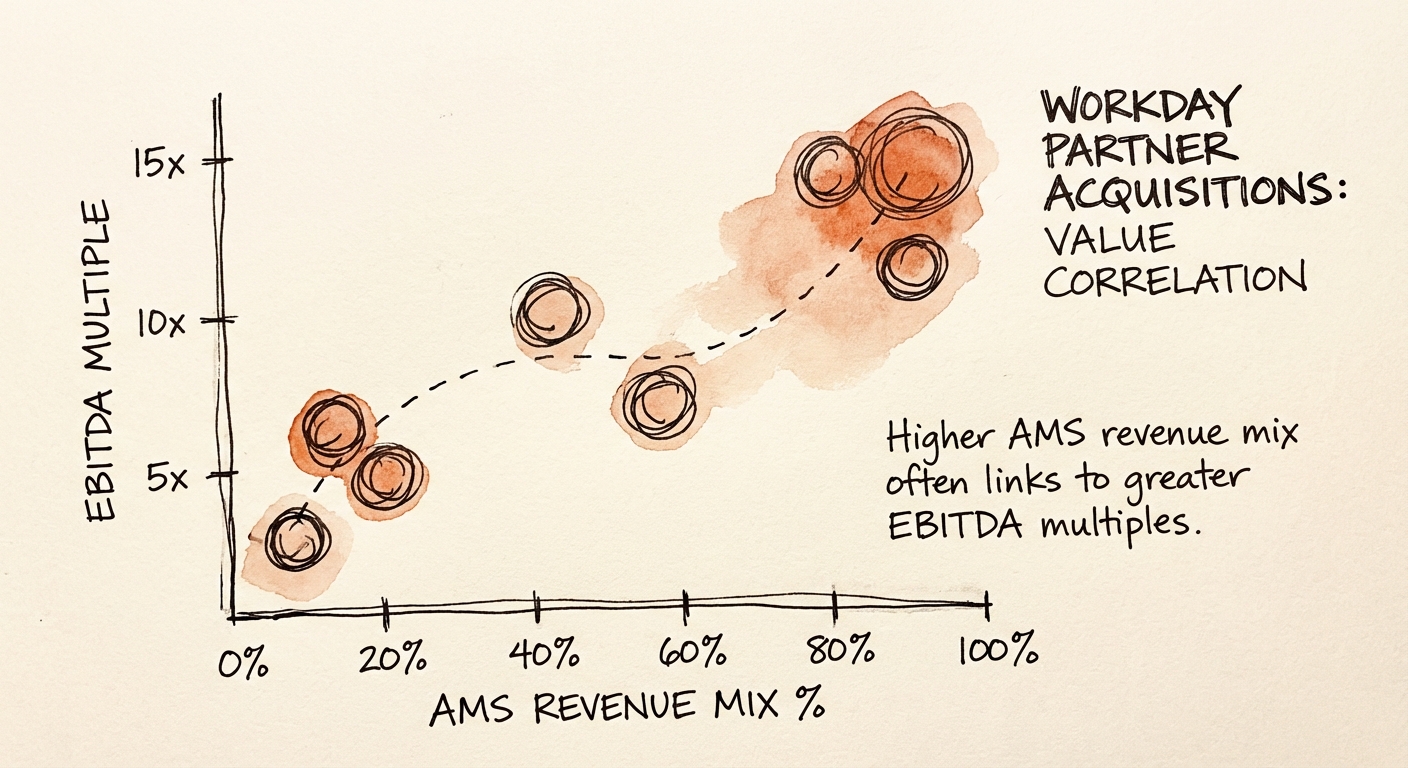

- 45% Minimum AMS (recurring) revenue mix required to unlock 12x+ valuation multiples.

The Valuation Bifurcation: Why 14x is Real (But Rare)

In the broader IT services market, trading multiples have softened. Generalist digital transformation shops are struggling to clear 8x EBITDA. But the Workday ecosystem is different. It is a closed loop, a "velvet rope" economy where supply is artificially constrained by the vendor. There are fewer than 160 active service partners globally, compared to thousands in the Salesforce or Microsoft ecosystems. This scarcity creates a floor on valuations, but it does not guarantee a ceiling.

We are currently tracking a massive bifurcation in Workday partner valuations. On the left side of the spectrum are the "Body Shops"—firms trading at 6x-8x EBITDA. These firms generate 80%+ of their revenue from "Launch" (initial implementation) projects. They are effectively high-end staffing agencies. Every quarter, they start from zero revenue. Their utilization is volatile, and their margins are chewed up by the bench costs required to keep expensive talent warm between deployments.

On the right side are the "Strategic Platforms" trading at 12x-15x EBITDA. The differentiator is not their headcount; it is their revenue mix. These firms have successfully pivoted to "Life" (AMS - Application Management Services). They don't just install Workday; they run it. When a partner demonstrates an AMS attach rate of >45% and multi-year contracts with automatic escalators, they stop being valued as a service firm and start being valued like a SaaS proxy. For a PE buyer, the thesis is simple: You are buying a tax on the payroll and financials of the Fortune 500.

In the Workday ecosystem, you aren't just buying a services firm. You are buying a monopoly on talent. If that talent walks out the door post-close, you bought a shell company with a high burn rate and no license to operate.

The Talent Trap: The "Velvet Rope" Ecosystem

In a Microsoft or AWS deal, talent attrition is a headache. In a Workday deal, it is an existential threat. Workday certifications are not open-market commodities; they are tightly controlled assets attached to the individual only while they are employed by a certified partner. If a Senior Financials Lead quits your target company to join a customer or an uncertified firm, that certification evaporates from your roster. It cannot be easily replaced because you cannot simply hire a freelancer to plug the gap.

The cost of replacing a Workday Lead in 2026 has hit $40,000 in recruitment fees alone, with a ramp time of 5-6 months to full billability. During due diligence, you must audit the "Certification Concentration Risk." I frequently see targets where 30% of the billable revenue is tied to three key architects. If those three people leave post-close—and they will, if you mess up the earnout—you haven't just lost capacity; you may have breached the partner threshold requirements to remain in the ecosystem. You are buying a monopoly on talent, but that talent has legs.

Furthermore, the rise of the Workday Talent Shortage means that labor cost inflation often outpaces rate card increases. If the target firm hasn't raised their AMS rates in 18 months, their gross margins are likely compressing by 200-300 basis points annually. A Quality of Earnings (QofE) report that ignores "Cost to Replace" for Workday talent is worthless.

The "Red Account" Diagnostic

Workday is not a passive vendor. They actively grade their partners on every deployment. A "Red Account" (a failed or stalled implementation) is not just a churn risk; it is an ecosystem exile risk. Unlike other vendors who might look the other way as long as the licenses get sold, Workday protects its brand ferociously. If a partner accumulates two or three "Red Accounts" in a rolling 12-month period, the Workday sales reps—who control the deal flow—will stop referring them.

In your diligence, you must demand the Partner Scorecard (often called the CSAT or C-Sat report) directly from the portal, not the sanitized version in the CIM. Look for the "Deployment Score." Anything below a 4.0/5.0 is a screaming red flag. It means the partner is burning political capital with the vendor. I have seen firms with $20M in revenue look healthy on a P&L basis, but they were effectively "shadow banned" by the Workday field sales team due to poor delivery. Their pipeline was drying up, and the historical growth rate was a mirage based on past reputation.

You also need to assess Integration Debt. Many partners hit their margins by cutting corners on integrations, leaving the client with a fragile system. This creates a "retention latent risk" that detonates 12 months later, usually right after you've integrated the add-on.