The practical answer

- Short answer

- A diagnostic guide for services founders on Workday partner economics. Analysis of tier requirements, certification costs, and the 2026 'bifurcation' of the ecosystem.

- Best fit

- Industry: Professional Services. Function: Alliances & Strategy

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- $22k Estimated 'Activation Cost' per consultant (Training + Exam + Lost Billable Time)

The "Pay-to-Play" Reality: Calculating the True Cost of Entry

For years, the Workday ecosystem was an exclusive club—a walled garden where a handful of partners enjoyed artificially high bill rates due to scarcity. In 2026, that garden gate has been blown off its hinges. Workday’s strategic pivot to become a "partner-first" organization has expanded the service partner ecosystem from roughly 40 firms to over 400 globally. While this sounds like an opportunity, for a mid-market consultancy, it represents a massive shift in unit economics.

The "Entry Tax" is no longer just about exclusivity; it is about capital efficiency. Our analysis of the 2026 program requirements shows that the Fully Loaded Cost of Certification has stabilized but remains a significant drag on gross margins.

The Certification "Toll Booth"

Unlike open ecosystems (like AWS or Microsoft) where certification is often a low-cost individual pursuit, Workday maintains strict controls. You are not just paying for an exam; you are paying for the privilege of billability.

- Direct Costs: Expect to pay between $1,500 and $4,000 per consultant for initial training and exams, depending on whether prerequisites are waived (a policy shift seen in late 2025).

- The "Churn Tax": Because certifications are tied to the partner firm, every time a senior consultant leaves, your investment walks out the door. If you have 20% attrition, you are effectively paying a 20% surcharge on your training budget annually just to stand still.

- The Opportunity Cost: The real killer isn’t the $4,000 fee; it’s the two weeks of lost billable time. At a standard bill rate of $225/hr, that is $18,000 in lost revenue per head during onboarding.

For a founder running a 50-person shop, this means your utilization rate floor is significantly higher than in a Salesforce or ServiceNow practice. You aren't just covering salary; you are amortizing a $22,000 "activation fee" for every new hire.

The scarcity premium is gone. You are no longer selling access to a gated community; you are selling a specific outcome in a crowded room. If you don't have IP, you don't have a moat.

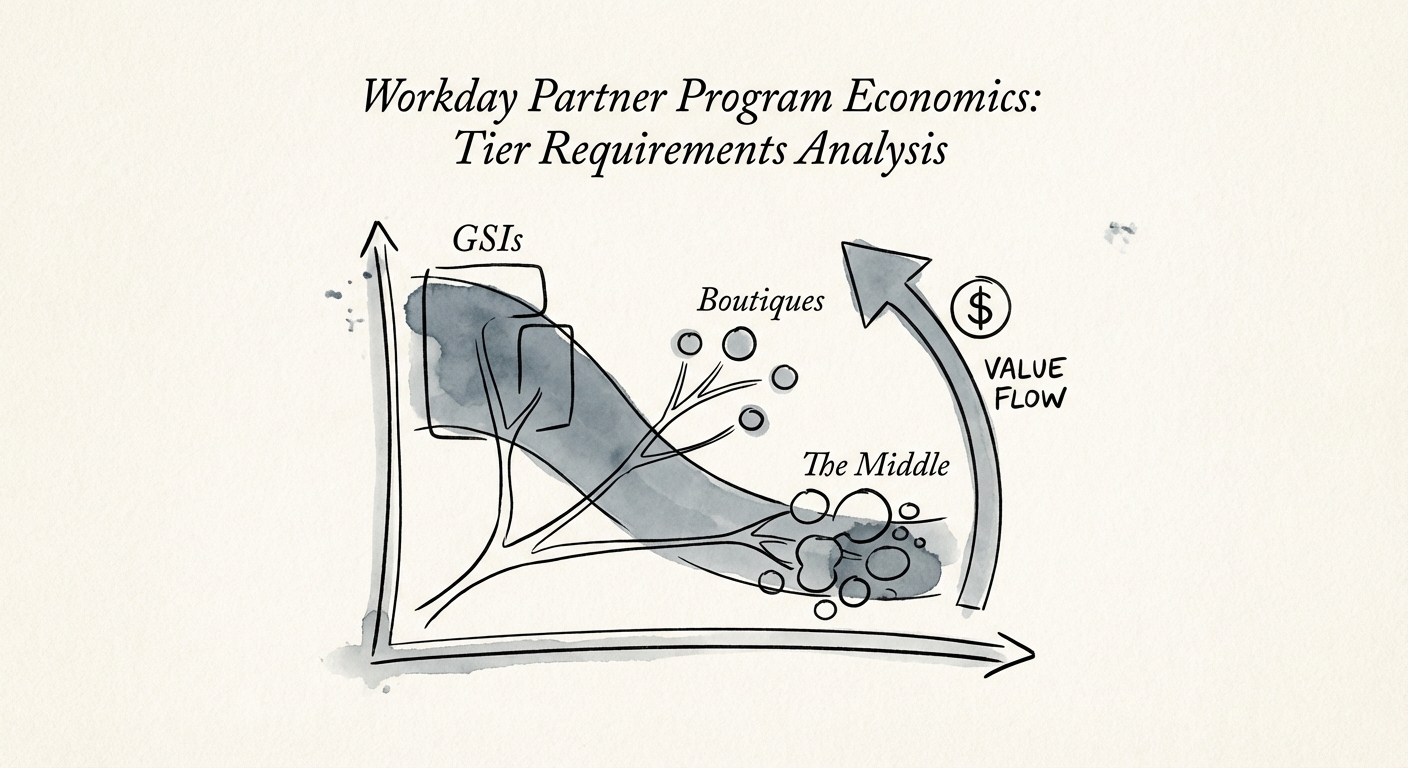

The Middle-Market Squeeze: Why Generalists Are Bleeding Margin

The explosion of partners from 40 to 400+ has created a dangerous bifurcation in the market. We are seeing a classic "barbell" distribution of value, leaving generalist implementation firms squeezed between scale and specialization.

The Barbell Effect

On one end, you have the Global Systems Integrators (GSIs) like Deloitte and Accenture. They own the massive, multi-year transformations involving thousands of seats. They can absorb the high certification costs through volume and cross-selling into Strategy/Ops.

On the other end, you have the Hyper-Specialized Boutiques. These firms don't just "do Workday"; they specialize in "Workday Financials for Healthcare" or "Adaptive Planning for SaaS." They command premium rates because they lower the client's risk profile.

The Squeezed Middle

The middle is where margins compress. If you are a generic "Workday Implementation Partner" with 50-100 staff and no distinct industry IP, you are now competing with 350 other firms for the same sub-enterprise scraps. The scarcity premium is gone. Rate cards in this segment are compressing by 10-15% as new entrants undercut legacy partners to buy market share.

This is a valuation trap. We see founders holding onto 2023 valuation multiples based on 2023 scarcity. But buyers know the landscape has changed. They aren't paying 12x EBITDA for a generic implementation shop anymore; they're paying for stickiness.

The Profitability Life Raft: IP and "Industry Accelerators"

If you are committed to the Workday ecosystem, you cannot survive on services revenue alone. The 2026 economic model demands Intellectual Property (IP). Workday’s aggressive push into the "Workday Economy"—opening up the platform for partners to build apps on Workday Extend—is your only lever for margin expansion.

The "Attach Rate" Strategy

Successful partners are shifting their mix from 100% Services to 80% Services / 20% IP. By building a proprietary app or connector (e.g., a specific payroll integration for a niche vertical), you do three things:

- differentiation: You become the only partner who can solve that specific problem, protecting your rate card.

- Stickiness: Services end when the project goes live. Apps renew annually.

- Valuation: Recurring revenue from IP trades at 6x-10x Revenue, whereas services revenue trades at 1x-1.5x Revenue.

Do not be a "Paper Tiger"—a term we use for firms that hoard certifications but lack delivery depth (see our analysis on certification risks here). Instead, use the Industry Accelerator program. Align your practice with Workday’s vertical sales teams (e.g., Higher Ed, Retail). If you can help a Workday rep close a deal 30% faster because you have pre-built configurations, they will bring you into every deal. That is how you lower your Customer Acquisition Cost (CAC) to near zero.