The practical answer

- Short answer

- A Private Equity due diligence framework for evaluating Veeva Systems partners. Benchmarks on Vault CRM migration opportunities, R&D Cloud premiums, and valuation multiples.

- Best fit

- Industry: Life Sciences. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 2029 The hard deadline for the Veeva CRM to Vault CRM migration, creating a defined 3-year revenue supercycle for partners.

The 'Vault CRM' Migration Supercycle: A $2B Services Opportunity

For Private Equity investors, the separation of Veeva Systems from the Salesforce platform represents the single largest capital deployment opportunity in Life Sciences IT since the initial shift to cloud. The mandatory migration from Veeva CRM (built on Salesforce) to Vault CRM creates a definitive 3-year service revenue supercycle (2026–2029) that will redefine ecosystem winners.

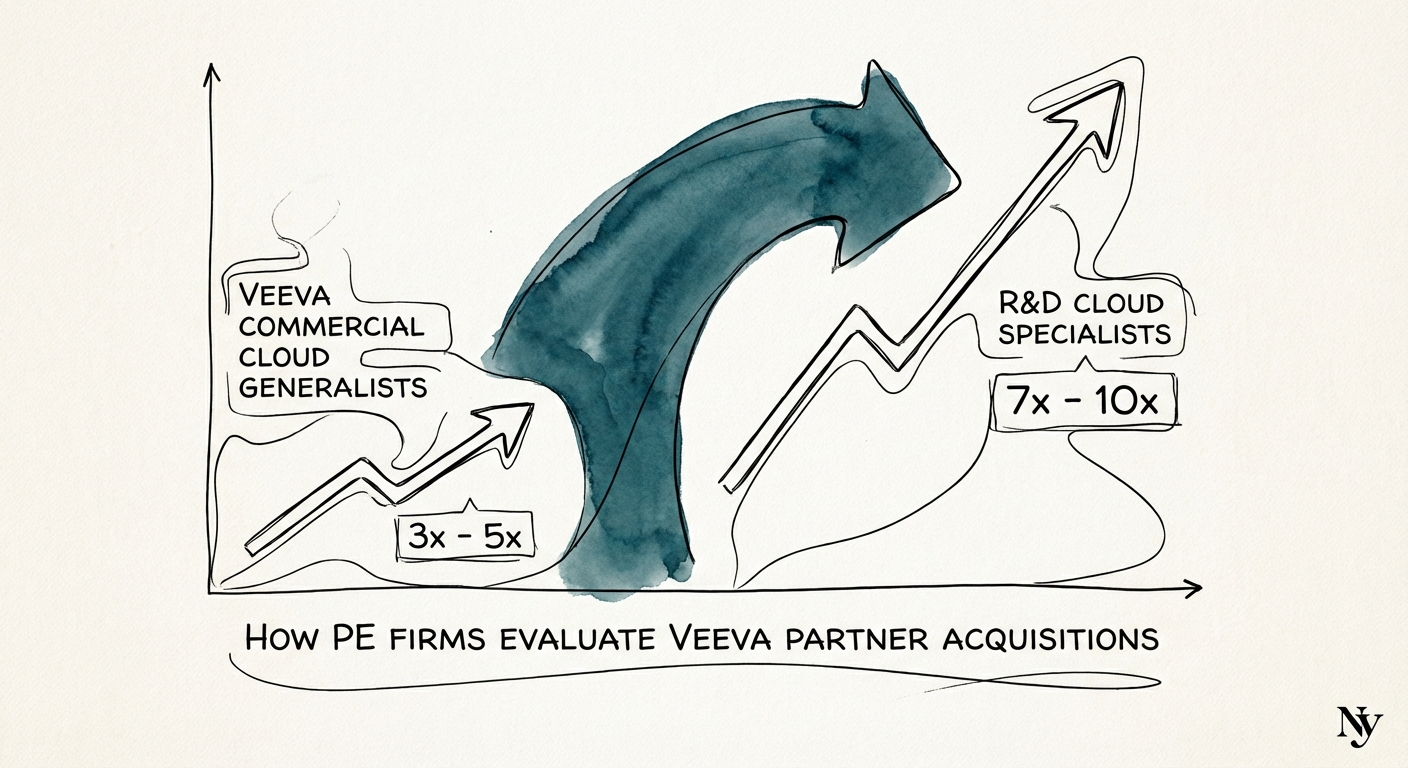

However, not all migration revenue is created equal. PE acquirers are currently bifurcating targets into two categories: Lift-and-Shift Generalists (trading at ~8x EBITDA) and Transformation Specialists (trading at 14x EBITDA).

The distinction lies in the ability to leverage the migration for broader commercial transformation. While generalists compete on hourly rates to move data fields, specialists are using the migration event to implement Veeva's Commercial Cloud suite (PromoMats, Crossix, OpenData). In due diligence, we look for a "Migration+" ratio: for every $1 of migration service revenue, the target should be generating $0.50-$0.75 in adjacent transformation services. If a target is merely moving data without upselling process re-engineering, their revenue cliff in 2030 will be fatal to the investment thesis.

The mandatory migration to Vault CRM isn't just a technical update; it's a market shakeout. Partners who treat it as a data move will be commoditized. Those who use it to rewrite commercial operating models will define the next decade of Life Sciences IT.

The Valuation Gap: Commercial Cloud vs. R&D Cloud

While the commercial side (CRM) offers volume, the R&D side (Clinical, Regulatory, Quality) offers "sticky" value. Our 2025 deal data indicates a significant valuation premium for partners specializing in the Development Cloud.

The Clinical Data Management Premium

Partners with deep expertise in Veeva Vault clinical applications (CDMS, eTMF, CTMS) are commanding the highest multiples in the sector. Unlike commercial deployments, which can fluctuate with sales force sizing, clinical systems are tied to the R&D pipeline—a budget line that remains resilient even during economic downturns.

Specifically, look for partners with "process governance" capabilities. A firm that simply configures Vault QualityDocs is a commodity. A firm that designs the Quality Management System (QMS) workflows inside Vault becomes an operational partner. Due diligence must test for this by auditing the billable rate hierarchy: if "Solution Architects" and "Subject Matter Experts" drive less than 30% of revenue compared to junior delivery staff, the firm lacks the IP moat required for a premium exit.

Beyond Staff Augmentation: The 'Agentic' AI Benchmark

The traditional Life Sciences IT services model—placing bodies to manage validation documents—is collapsing. With Veeva's aggressive rollout of Agentic AI capabilities in 2025/2026, the demand for low-level manual validation and data entry is disappearing. PE firms must evaluate a target's readiness for this shift.

The new metric for 2026 is AI-to-Services Density. We are seeing premium valuations for partners developing proprietary "AI Accelerators" for Veeva—specifically in regulatory submission automation and promotional content review. A target should be able to demonstrate how they are using Veeva's API to build proprietary IP that reduces implementation time by 30-40%. If their business model still relies on linear headcount growth to scale revenue, their terminal value is at risk.

Furthermore, the recent resolution of the data dispute between Veeva and IQVIA opens new integration opportunities. Partners capable of bridging IQVIA data assets with Veeva commercial workflows are currently trading at a scarcity premium, as this requires a dual-competency that few pure-play Veeva shops possess.