The practical answer

- Short answer

- A private equity due diligence framework for valuing Shopify agencies and apps. Analysis of the valuation gap between 'Theme Flippers' (5x) and 'Commerce Product Studios' (12x).

- Best fit

- Industry: Ecommerce Technology. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 92% Annual retention rate required to command a 'Strategic Partner' valuation multiple.

The Great Bifurcation: Why 'Shopify Agencies' Are Under Pressure

In 2026, the term 'Shopify Agency' is a valuation trap. The private equity market for Shopify partners has bifurcated into two distinct asset classes with radically different margin profiles and exit multiples. On one side, you have the 'Launch Factories'—traditional design and development shops that trade on project revenue. On the other, you have 'Commerce Product Studios'—strategic partners integrated into the enterprise 'Commerce Components' (CCS) stack.

The Valuation Gap: 5x vs. 12x

Our data, corroborated by 2025 market benchmarks, shows a massive disparity in how these assets are priced.

- The Launch Factory (5x EBITDA): These firms operate on a 'churn and burn' model. They build stores, launch them, and hand the keys to the merchant. Their revenue is 80% project-based, EBITDA margins hover around 18-22%, and client retention struggles at ~78%. Buyers view them as low-moat staffing businesses.

- The Commerce Product Studio (10-12x EBITDA): These partners have pivoted to Shopify Plus economics. They maintain 32%+ EBITDA margins and, crucially, retain 92% of their clients annually through high-margin managed services (AMS) and proprietary IP. They don't just 'build sites'; they manage gross merchandise value (GMV) for enterprise brands.

For PE buyers, the differentiator is no longer just 'Plus' status—it is the ability to execute on Commerce Components by Shopify (CCS). As Shopify pushes upmarket to compete with Salesforce Commerce Cloud and Adobe, partners capable of handling headless, composable architectures for $500M+ GMV merchants have become scarce, strategic assets.

The partners trading at 12x aren't selling websites; they are selling enterprise commerce infrastructure with 92% retention. If your revenue resets to zero every January 1st, you are a 4x asset.

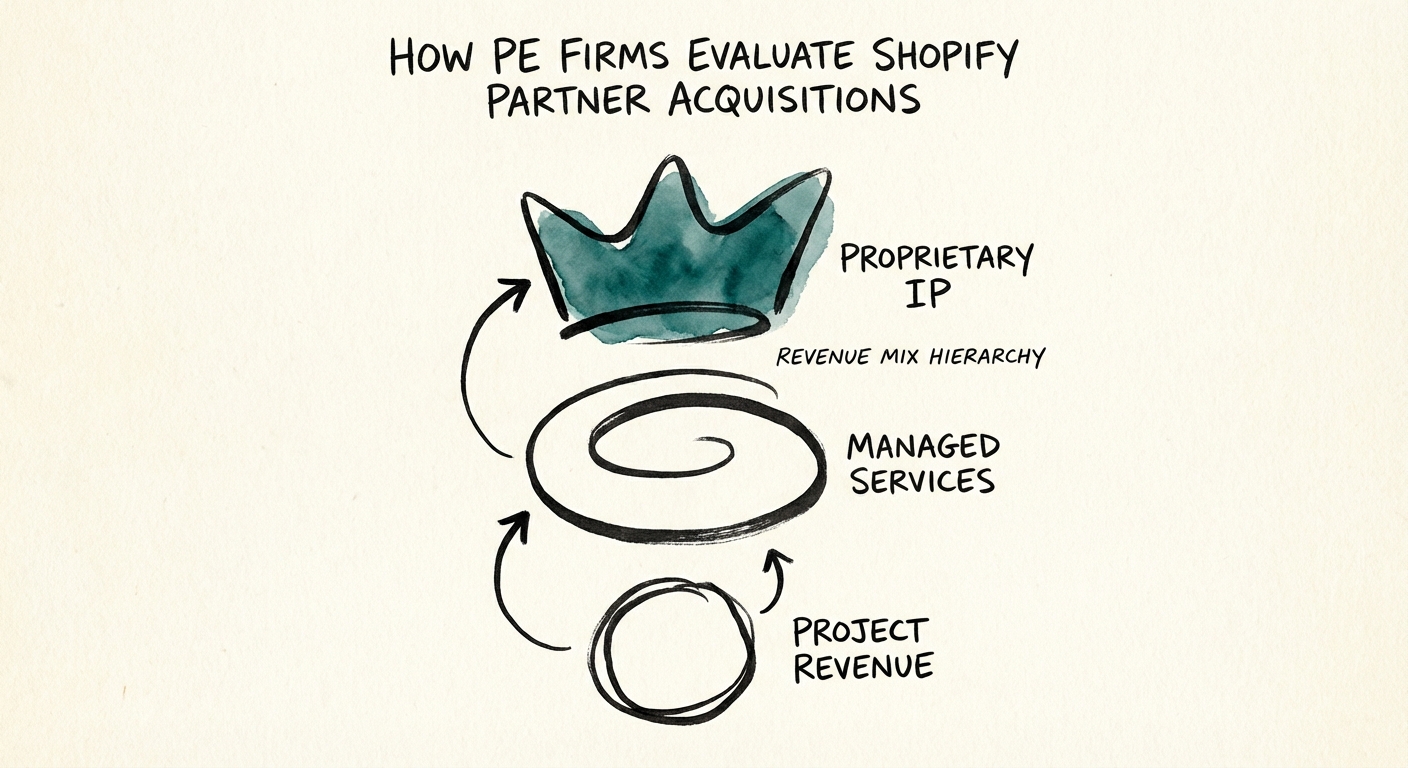

The Revenue Quality Diagnostic: Beyond the 'Launch Trap'

The most common deal-killer in Shopify partner M&A is the 'Launch Trap'—a revenue model dependent on constantly finding new logos to replace completed projects. In due diligence, we strip out one-time implementation fees to isolate the Recurring Impact Revenue.

Analyzing the Revenue Mix

We evaluate targets based on three specific revenue quality tiers:

- Tier 1: Committed Managed Services (The Gold Standard). This is not 'break-fix' support. This is a retained engineering and CRO team optimizing a headless stack. Elite partners generate 50%+ of revenue here. If a firm's launch revenue outweighs retention revenue by more than 2:1, it is a red flag for sustainability.

- Tier 2: Proprietary IP & Apps. The 2025 Shopify Partner Program split into 'Service' and 'Technology' tracks for a reason. Service partners who own niche apps (e.g., specific ERP connectors or returns management portals) command SaaS-like multiples on that revenue stream. However, buyers must audit whether these apps are genuine products or just 'white-labeled' scripts with high technical debt.

- Tier 3: The 'Theme Flip' Project. Revenue derived from customizing standard themes for SMB merchants is viewed as 'empty calories.' It boosts top-line revenue but degrades the valuation multiple because it has zero switching costs.

Technical Due Diligence: The 'Verified Skills' Moat

With the 2025 updates to the Shopify Partner Program, 'Verified Skills' and 'Credential Attainment' are now quantitative metrics for tier status (Premier/Platinum). In technical due diligence, we are seeing a direct correlation between a firm's certified talent density and its code quality.

The Code Audit Checklist

PE sponsors must dig deeper than the partner badge. Our technical debt assessments frequently uncover:

- 'Frankenstein' Headless Builds: Agencies that jumped on the Hydrogen/Remix bandwagon without sufficient engineering maturity often leave behind unmaintainable codebases. This creates a 'retention latent risk' where merchants churn because they cannot update their own storefronts.

- App Dependency Risk: Low-value agencies solve problems by installing 30+ third-party apps, killing site performance and margins. High-value partners write custom functions to eliminate app bloat.

- Vendor Lock-in via Spaghetti Code: We penalize valuations where the 'proprietary IP' is actually just undocumented, custom Liquid code that prevents the merchant from ever leaving the agency without a total rebuild. That is not a moat; it is a liability.

The Takeaway: To command a premium exit in 2026, a Shopify partner must look less like a digital agency and more like a specialized systems integrator. The multiple is in the integration, not the implementation.