The practical answer

- Short answer

- Shopify Partner valuation benchmarks for 2026. Why 'Plus' status, recurring revenue, and proprietary IP drive agency multiples from 4x to 12x EBITDA.

- Best fit

- Industry: eCommerce Technology. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 45% Minimum Recurring Revenue mix required to break the 8x EBITDA valuation ceiling in 2026.

The Valuation Bifurcation: Service Shops vs. Commerce Platforms

In the Shopify ecosystem, not all revenue is created equal. We are witnessing a stark bifurcation in partner valuations as we enter 2026. On one side, we have the Service Shops: generalist agencies executing themes, migrations, and standard implementations. These firms typically trade at 4x to 6x EBITDA. They are fundamentally capped by the "iron triangle" of billable hours: they can only grow by adding headcount, and their revenue resets to zero every January 1st.

On the other side are the Commerce Platforms—often Shopify Plus Partners—who have successfully bridged the gap between professional services and SaaS. These firms trade at 10x to 14x EBITDA, with some hybrid models commanding revenue multiples. The differentiator is not just the "Plus" badge, but the underlying revenue architecture. Premium partners have shifted at least 40% of their revenue to recurring managed services or proprietary IP (apps, middleware, connectors), effectively decoupling growth from headcount.

For Private Equity sponsors, the arbitrage opportunity lies in acquiring a high-performing Service Shop and installing the operational infrastructure to convert it into a Commerce Platform. This requires a fundamental shift in the business model: moving from "building stores" to "managing gross merchandise value (GMV)." The former is a project; the latter is a partnership.

The difference between a 5x and a 12x exit isn't the quality of your code—it's the quality of your revenue. Buyers don't pay for your past projects; they pay for your future predictability.

The "Plus" Premium: Access to High-LTV Enterprise Clients

The Shopify Plus Partner designation is more than a marketing badge; it is a velvet rope that filters client quality. In 2026, the valuation premium for Plus Partners stems primarily from the Unit Economics of their client base. Non-Plus partners typically serve merchants with $500k–$5M in GMV. These merchants have high churn rates, limited budgets, and require constant hand-holding.

Plus Partners, conversely, gain exclusive access to the $10M–$500M GMV segment (and increasingly, the B2B enterprise market). These clients offer:

- Higher Retention: Enterprise merchants rarely re-platform. Once integrated, the cost of switching is prohibitive, leading to multi-year lifecycles.

- Wallet Expansion: Large merchants require ongoing optimization, headless architecture management, and custom app development, driving Net Revenue Retention (NRR) above 110%.

- Predictable Cash Flow: Retainers for Plus clients often start at $10k/month, providing the recurring revenue floor that buyers covet.

However, the badge alone is not a guarantee of value. We see "Paper Plus" partners who hold the certification but still operate as transactional development shops. To unlock the 12x multiple, a partner must demonstrate that they are monetizing the lifecycle of the merchant, not just the launch.

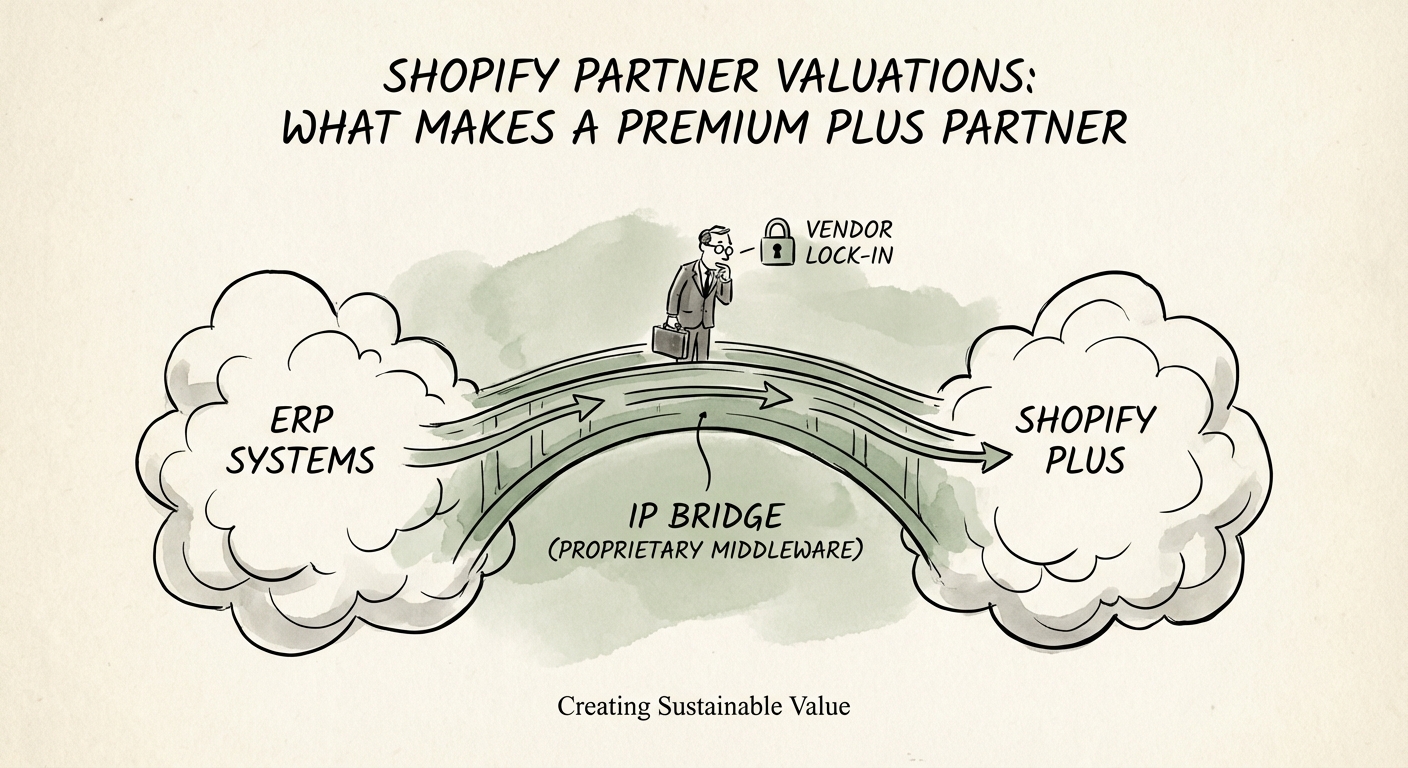

The IP Bridge: Transforming Services into Software

The single biggest lever for multiple expansion in Shopify Partner M&A is Proprietary Intellectual Property (IP). Pure-play agencies are valued on EBITDA; software companies are valued on Revenue. The "Premium Plus" partner sits in the middle, using IP to boost margins and stickiness.

This does not necessarily mean building a public app for the Shopify App Store (which is a different, highly competitive business model). Instead, high-value partners build "Middleware IP":

- Pre-built Connectors: Proprietary integrations for ERPs (NetSuite, D365) that reduce implementation time and create vendor lock-in.

- Accelerators: Vertical-specific headless frameworks (e.g., a "Luxury Fashion Accelerator") that standardize 80% of the build.

- Data Products: Analytics dashboards that aggregate merchant data to provide benchmarks.

When a partner owns the "glue" that holds the merchant's tech stack together, they become irreplaceable. A service contract can be cancelled; a critical integration cannot. In due diligence, we look for IP that generates "High-Margin Service Revenue"—revenue that looks like services on the invoice but has the 70%+ gross margins of software because it relies on pre-built assets rather than fresh code.