The practical answer

- Short answer

- Workday partners command a 40-60% valuation premium over generalist IT firms. Here is the data on multiples, certification moats, and the AMS revenue mix that drives 12x+ exits.

- Best fit

- Industry: Professional Services. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 12.1x Average EBITDA multiple for top-tier US private equity buyouts in specialized tech services (2025).

The "Closed Garden" Economics

In the IT services M&A market, not all billable hours are created equal. While generalist digital transformation shops and Microsoft/AWS partners are trading at 6x–8x EBITDA, certified Workday partners are consistently commanding 10x–14x EBITDA multiples, with platform-enabled firms pushing even higher. This isn't accidental; it is structural.

Unlike the Salesforce ecosystem, which is an open market with thousands of consulting firms, Workday operates as a "closed garden." There are fewer than 50 prime services partners globally. You cannot simply hire five certified consultants and hang a shingle; Workday controls the partner channel with an iron grip, capping the number of firms authorized to implement their software. This artificial scarcity creates a defensive moat that private equity buyers are willing to pay a premium for.

For a PE Operating Partner, this changes the investment thesis. You aren't just buying a services P&L; you are buying a license to operate in a market where supply is artificially constrained and demand is mandated by multi-year enterprise subscription contracts. The entry barrier is not capital; it is authorization.

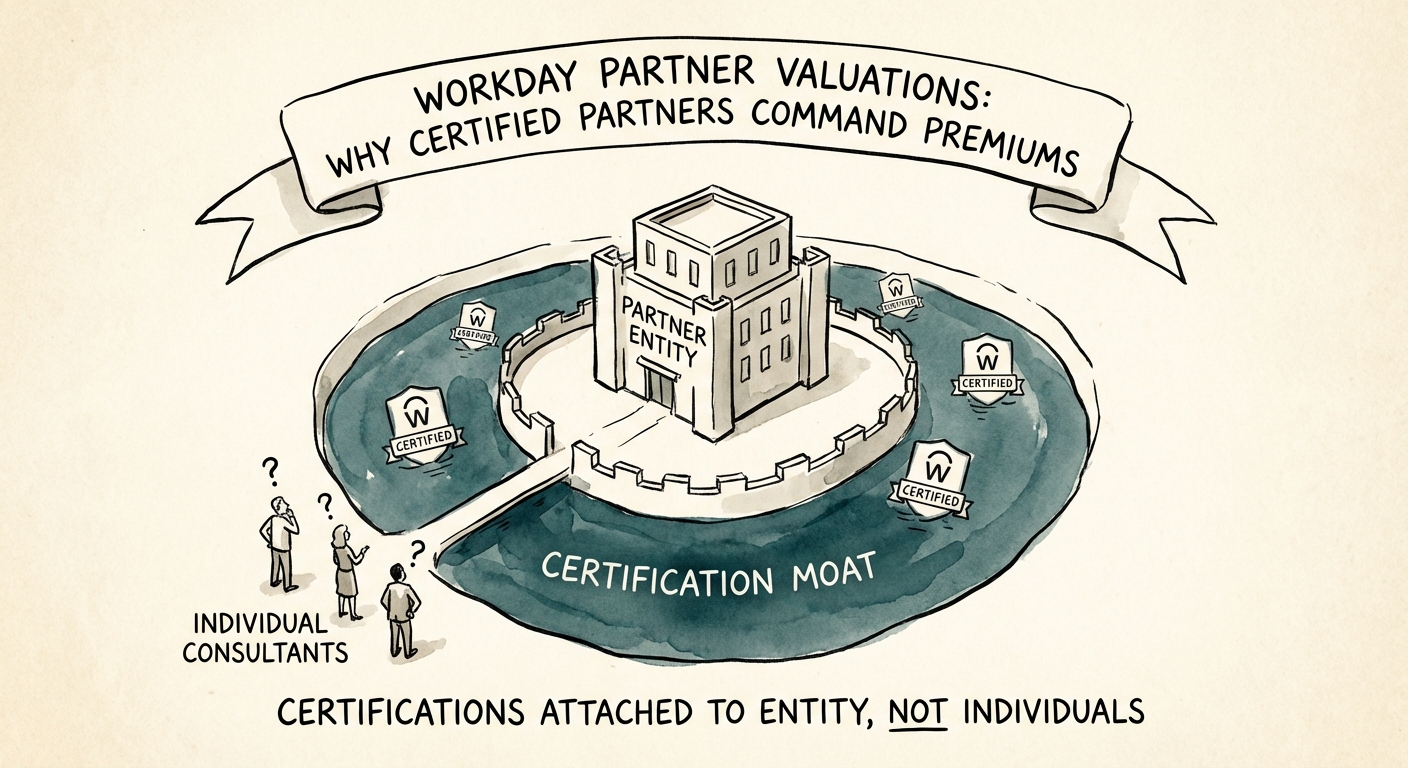

The Certification Moat

The primary driver of this premium is the unique nature of Workday certifications. In most ecosystems (AWS, Microsoft, Salesforce), a certification belongs to the individual. If a Senior Architect leaves Firm A for Firm B, they take their credentials with them. In the Workday ecosystem, certifications are tethered to the partner status. If a consultant leaves the ecosystem, their certification lapses. This creates two distinct valuation drivers:

- Talent Retention: Consultants are stickier because their career value is tied to their employment at a certified partner.

- Asset Durability: The "bench" is a tangible asset that competitors cannot easily replicate via poaching.

You aren't just buying a services P&L; you are buying a license to operate in a closed market where supply is artificially constrained and demand is mandated.

The Valuation Hierarchy: Deploy vs. AMS

While the Workday badge gets you in the door, the revenue mix determines the exit multiple. We see a clear bifurcation in how these firms are valued based on their reliance on "Deploy" (initial implementation) versus "AMS" (Application Management Services).

1. The "Deploy" Discount (8x–10x EBITDA)

Firms that generate >70% of their revenue from new implementations are essentially construction crews. They build the house and leave. While high-margin (45%+ gross margin), this revenue is lumpy and project-based. Every January 1st, the backlog resets. Buyers discount these cash flows because they require constant sales engine performance to maintain.

2. The "AMS" Premium (12x–15x EBITDA)

The unicorns of this ecosystem have flipped the model. They use implementations as a loss leader or customer acquisition channel to secure long-term AMS contracts. These are not break-fix help desk tickets; they are "optimization as a service." Because Workday pushes 2-3 major feature releases annually, clients need continuous high-level consulting to consume new innovation. Firms with 40%+ recurring revenue from AMS contracts trade at the top of the range.

3. The "Platform" Multiplier (15x+ EBITDA)

The highest valuations go to partners who have built IP on top of the Workday platform. Look at Kainos. Their "Smart Test" and "Smart Audit" products allow them to monetize customers who aren't even services clients. They trade closer to SaaS multiples because they have decoupled revenue from headcount. If your target asset has proprietary accelerators that reduce implementation time by 30%, that is IP, not just service efficiency.

Due Diligence: The "Paper Tiger" Trap

When evaluating a Workday partner, standard financial diligence will miss the specific risks of this ecosystem. We frequently see "Paper Tiger" firms that look healthy on a spreadsheet but are rotting operationally.

The Subcontractor Ratio

Workday strictly limits the use of independent contractors, yet many boutique partners secretly rely on them to flex up for big projects. In a Quality of Earnings (QofE) engagement, scrutinize the W2 vs. 1099 ratio. A firm relying on >20% contractors is a compliance risk and a margin risk. If Workday audits them, that capacity evaporates overnight. True enterprise value lies in the W2 bench.

Utilization vs. Billability

In this ecosystem, "Shadowing" is mandatory for certification. You will see junior consultants who are "billable" but generating zero revenue because they are tagging along on projects to get their certification stamps. Don't add these back to EBITDA as "one-time training costs." This is the cost of goods sold (COGS) in the Workday world. It is a permanent recurring expense required to maintain the bench.

The Customer Concentration Trap

Because Workday deals are massive (often global F500 deployments), a $20M partner might have 60% of their revenue tied to two clients. If one of those projects pauses—or if Workday assigns a different partner for Phase 2—the P&L collapses. We advise applying a specific liquidity discount for any partner where a single client represents >15% of Gross Profit, regardless of the brand name.