The practical answer

- Short answer

- Two Databricks partners, identical revenue, one trades at double the multiple. Why FRTB and VaR expertise reprices a financial-services practice at exit.

- Best fit

- Industry: Financial Services Technology. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- Premium Financial Services specialists can earn stronger buyer interest when IP, regulated workflows, and repeatable revenue are documented.

Two partners. Same $18M in revenue. One trades at twice the multiple.

Put two Databricks partners side by side at the deal table. Both did roughly $18M last year, both grew north of 35%, both have the certifications. One sells for a number that makes the founder uncomfortable in a good way. The other sells for a number that makes him reconsider whether to sell at all. The difference isn't size or growth. It's what the revenue is made of.

The category itself is on fire. Databricks closed a Series K at a $100B+ valuation, and the gravity of that number pulls every one of the ecosystem's thousands of partners along with it. But a rising platform doesn't reprice your services firm. Buyers don't pay you for Databricks' enterprise value; they pay you for how hard you'd be to replace. And on that question, the partner base has split clean down the middle.

On one side: the migration shop. It bills Spark engineers by the hour to lift on-prem Hadoop into the lakehouse. Honest, profitable, growing — and quietly terminal as an asset. Once the data lands, the project ends. A diligence team reads that as project revenue, prices it like project revenue, and no amount of year-over-year growth talks them out of it. The faster you grew on migrations, the more they wonder what happens when the migration backlog runs dry.

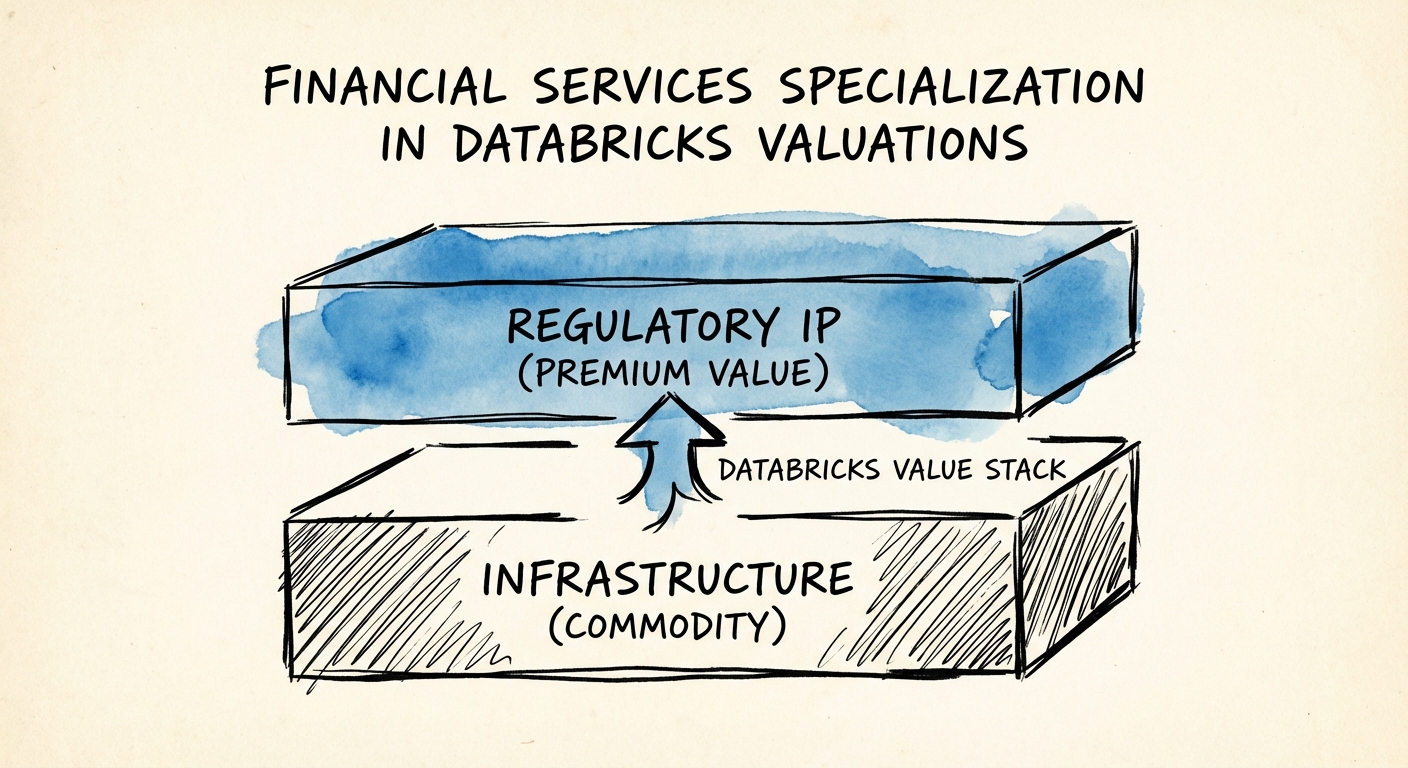

On the other side: the partner who stopped selling engineering hours and started selling things like real-time fraud scoring and automated regulatory reporting. The work is sticky because it's wired into a process the client cannot turn off. That's the gap that doubles the multiple — and in financial services, it's at its widest.

Any decent engineer can tune a Delta Lake table. The partner who knows why that table has to survive a regulator's FRTB audit is selling a different company entirely.

What FRTB does to a comp sheet

Here's the mechanic buyers are actually paying for. A generalist knows how to optimize a Delta Lake table. A financial-services specialist knows how to structure that table so it survives a Fundamental Review of the Trading Book (FRTB) capital-charge calculation, and so the lineage holds up when a regulator asks the bank to reconstruct a number from 14 months ago. That second skill is not a faster version of the first. It's a different business with a moat measured in years of domain scar tissue.

This is why PE sponsors in 2025 are screening for specific patterns rather than headcount. The work that reprices a practice clusters in a few regulated workflows:

- Risk and capital: accelerators that ingest market data and run Value-at-Risk and FRTB capital calculations on a schedule the trading desk depends on — not a one-off model, a standing process.

- Financial crime: graph-based transaction-monitoring and fraud-detection pipelines that the compliance team runs every single day and would never rip out mid-investigation.

- Regulatory and ESG reporting: data pipelines feeding disclosures the institution is legally obligated to file under applicable SEC, EU, or supervisory requirements.

What ties these together isn't the technology — it's that the client cannot stop running them. A migration ends. A monthly capital report does not. When a partner validates this kind of IP through the Brickbuilder Solutions program, they hand the buyer third-party evidence that the asset is real and reusable, not a slide deck.

Why your gross margin gives you away

The valuation gap shows up in the margin line before anyone reads the contracts. A pure-labor shop is structurally capped: cost of delivery scales one-for-one with revenue, so growing the top line never widens the percentage. A specialist who deploys a pre-built accelerator on each engagement is effectively re-licensing the same IP again and again, decoupling revenue from a hiring plan. Recent market analysis finds that consulting firms with genuine niche specialization are posting the strongest EBITDA-multiple expansion, well ahead of generalist peers — and a buyer reads a flat margin curve as confirmation you're selling time, not assets.

The mistake that hides your premium inside OpEx

Here's the part that costs founders real money, and it's an accounting choice, not a sales problem. The most common error I see in a specialized Databricks practice is burying the engineering hours that built the fraud-detection or VaR accelerator inside general operating expense — which means the very investment that justifies the premium is quietly depressing the EBITDA the buyer underwrites. You built the moat and then expensed it into invisibility.

Before you ever open a data room, run three adjustments. They're not gimmicks; they're the difference between a buyer seeing a labor shop and a buyer seeing a platform:

- Pull IP build cost out of COGS. The hours spent constructing a reusable accelerator are an investment in a durable asset, not the cost of delivering a single project. Where the accounting treatment genuinely supports capitalizing that R&D, doing so repositions those costs below the EBITDA line and lets the adjusted earnings reflect what you actually built.

- Carve out the recurring stream. If you're running ongoing DataOps — keeping a bank's risk pipelines live month after month — separate that revenue from one-time project work wherever the contracts support it. Buyers underwrite a standing operational mandate at a completely different multiple than a finite implementation.

- Quantify time-to-value, with the regulatory hook attached. In the CIM, show that your accelerator gets a bank to a compliant FRTB or AML deployment in a fraction of the time a generalist would need from a cold start. "Faster" is a feature. "Faster to a regulator-defensible result" is the moat — make the buyer feel the cost of choosing anyone else.

The timing matters because the window is open but not forever. The 2026 private-equity outlook points to sharpening sponsor appetite for high-quality AI and data assets, and sponsors are hunting platforms, not bodies. A Databricks practice that's a collection of clever engineers gets benchmarked against every other services firm in the pipeline. A practice that has become the institutional memory of a bank's risk department gets priced as something a competitor cannot reproduce — which is the entire game. If you can name the three regulated workflows you'd defend to the death, you already know which company you're selling.