The practical answer

- Short answer

- Azure partners with deep Data & AI capabilities (Fabric, OpenAI) command a 6-turn EBITDA premium over infrastructure generalists. Here is the 2026 M&A diagnostic.

- Best fit

- Industry: IT Services & Technology. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- Premium Median EBITDA multiple for Azure Partners with >40% Gross Margin from Data & AI Services (2026).

The Great Bifurcation: Why "Lift and Shift" is Now a Commodity

For the last five years, the private equity playbook for Azure partners was simple: acquire robust Infrastructure-as-a-Service (IaaS) shops, consolidate the CSP (Cloud Solution Provider) spend, and arbitrage the Microsoft incentives. That playbook is dead. In 2026, we are witnessing a massive bifurcation in valuation multiples that has left generalist infrastructure firms puzzled and specialized Data & AI firms swimming in LOIs.

The data is merciless. According to Q4 2025 transaction data, generalist Azure partners—those primarily focused on VM migrations, backup, and basic CSP resale—are trading at a median of 8.1x EBITDA. They are viewed as utilities: necessary, reliable, but low-growth commoditized assets. Conversely, Data & AI Specialists—firms delivering "Frontier" capabilities like Microsoft Fabric implementation, Azure OpenAI integration, and complex data estate modernization—are commanding a median of premium EBITDA multiples. That spread is driven largely on what you sell, not just how much you sell.

Why the gap? Because PE sponsors have realized that infrastructure is merely the plumbing. The value creation in the next cycle (2026-2030) comes from the "Intelligence Layer." Buyers are no longer paying for the capacity to move a server to the cloud; they are paying for the capability to turn that cloud data into predictive insight. If your firm’s primary revenue stream is attached to compute consumption rather than data transformation, you are effectively selling electricity in an AI gold rush. You might keep the lights on, but you won't get the exit premium.

If your primary revenue stream is attached to compute consumption rather than data transformation, you are effectively selling electricity in an AI gold rush. You might keep the lights on, but you won't get the exit premium.

The "Fabric" Moat: The New Litmus Test for Due Diligence

In 2026, Microsoft Fabric has become the single most critical technical diligence signal for Azure partner value. It is no longer just a product; it is a proxy for your firm's future relevance. When our team conducts Technical Due Diligence for PE buyers, the absence of a mature Fabric practice is an immediate red flag that caps valuation. Why? Because you cannot deploy Copilot or Azure OpenAI effectively on a fragmented, legacy data estate.

We typically see three types of partners in the market:

- The Legacy Reseller: Resells SQL licenses and manages VMs. Valuation ceiling: 6x-8x.

- The Modernizer: Moves data to Azure Synapse/Data Lake but lacks AI execution. Valuation range: 9x-11x.

- The AI-Native Specialist: Implements Fabric as the "nervous system" for generative AI applications. Valuation floor: 14x.

The premium exists because the "AI-Native Specialist" solves the hardest problem in the enterprise: Data Governance and Readiness. Generative AI is useless without clean, governed data. Partners who have mastered the transition from distinct data silos to the unified Fabric architecture are unlocking the "Implementation Gap" premium. They aren't just billing hours; they are building the intellectual property (IP) and frameworks that allow enterprise clients to actually use the AI tools they are buying. This is why the 2025 M&A trend lines show such a sharp detachment between high-value consulting and commodity implementation.

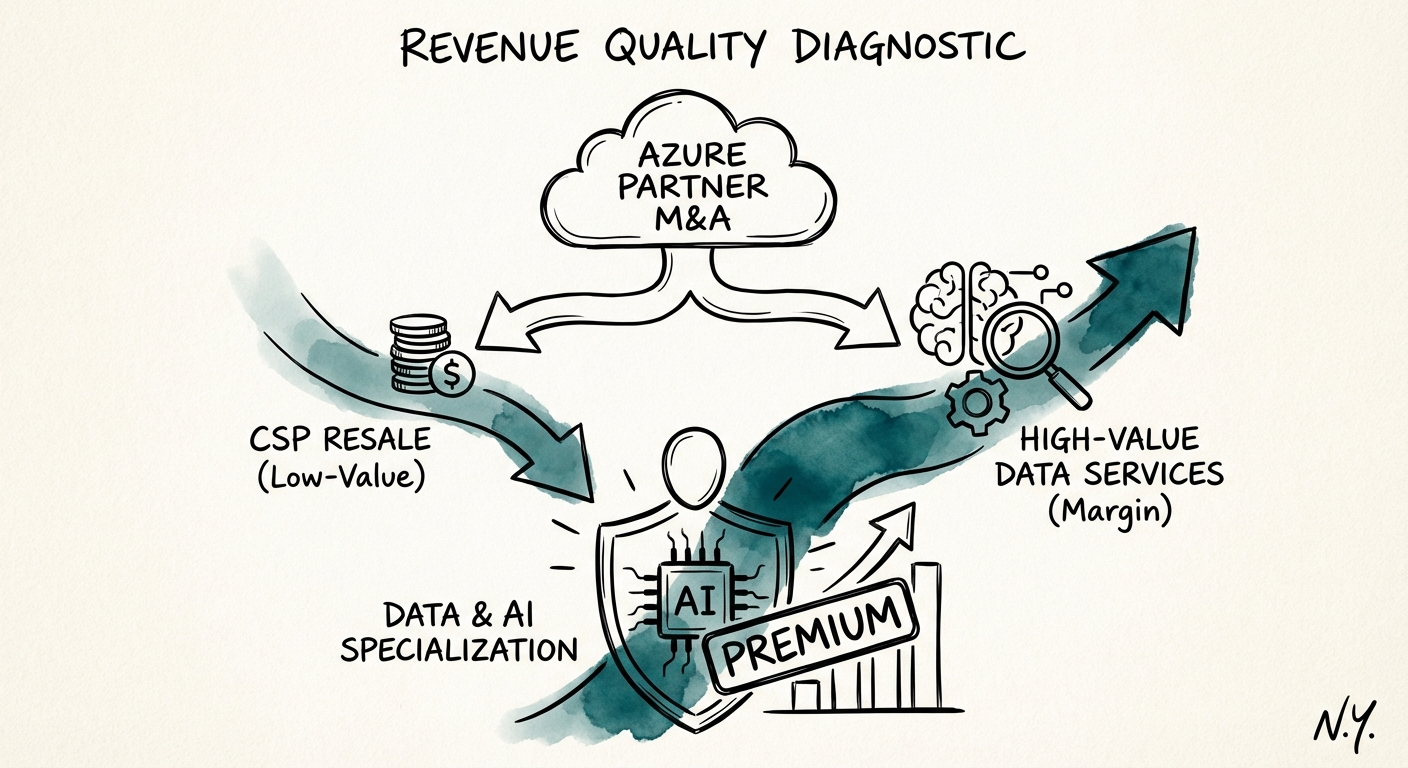

The Revenue Quality Diagnostic: Are You a "Fake" Specialist?

Many Azure partners slap an "AI" badge on their website because they ran a single Copilot pilot. In M&A processes, we dismantle this narrative using a simple Revenue Quality Diagnostic. We strip out low-margin licensing (CSP) and commodity managed services to isolate the High-Value Data Services (HVDS) revenue mix.

The 40% Threshold

To command the 14x premium, a partner typically needs at least 40% of their Gross Margin generated from Data & AI professional services (Architecture, Data Engineering, Model Tuning). If 80% of your margin comes from CSP rebates and Tier 1 helpdesk support, you are an infrastructure company in disguise, and you will be priced like one. Buyers are applying a modified "Rule of 40" to these service firms: Organic Revenue Growth % + EBITDA Margin %, but with a heavy weighting on the composition of that growth.

For founders looking to exit, the move is clear: Stop buying revenue that churns (low-margin CSP) and start building revenue that sticks (Data Estate IP). If you want the multiple expansion, you must pivot your delivery teams from "keeping it running" to "making it smart." The market has spoken: Infrastructure is the dial-tone. Data is the conversation. Make sure you're selling the right one.