The practical answer

- Short answer

- Why GCP partners with Data Analytics & BigQuery specializations trade at 14x EBITDA while infrastructure generalists stall at 8x. A due-diligence read for PE investors.

- Best fit

- Industry: Private Equity / IT Services. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 14x Average EBITDA multiple for specialized Data & Analytics partners in 2026, compared to 8.8x for generalists.

The Great Bifurcation: Infrastructure Commodity vs. Data Scarcity

If you are holding a Google Cloud Platform (GCP) consultancy in your portfolio today, you are likely looking at one of two very different exit scenarios. In one lane, we have the Infrastructure Generalists—firms that built their revenue on "Lift and Shift" migrations, VM management, and basic resale. In 2026, this is a race to the bottom. Automation has compressed margins, and the "migration" wave has largely crested for the enterprise mid-market. These firms are trading at 8x-9x EBITDA, often struggling to differentiate against Global Systems Integrators (GSIs).

In the other lane, we have the Data & Analytics Specialists. These are firms that moved beyond moving servers to moving intelligence. They specialize in BigQuery, Looker, and Vertex AI. They don't just store data; they architect the semantic layers that power GenAI. According to 2025-2026 market data, these firms are commanding a massive premium, trading at 12x-15x EBITDA.

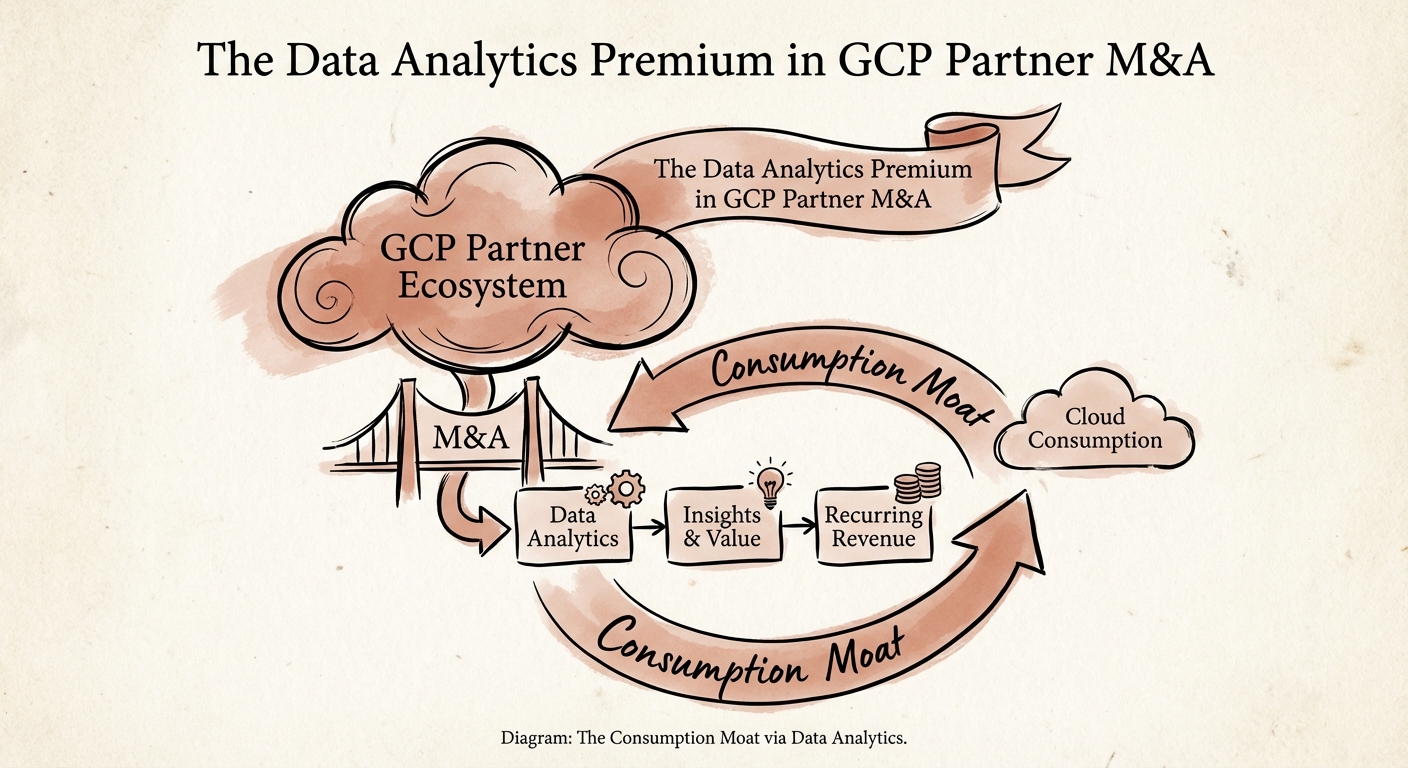

Why the gap? It comes down to Revenue Durability. An infrastructure migration is a finite project with low-margin managed services on the back end (monitoring, patching). A data estate modernization is an infinite game. Once a client's data is in BigQuery, the demand for analytics, AI modeling, and "reverse ETL" activation never stops. As I've noted in our analysis of IT Services M&A trends, buyers are no longer paying for headcount; they are paying for consumption drivers.

You bought a GCP partner thinking 'Cloud is hot.' But if they are just doing 'Lift & Shift', you bought a commodity. The real value is in the firms that turn data into decision-making.

The "Multiplier Effect" and Consumption Economics

The smartest PE investors have stopped looking at "Bookings" and started looking at ACR (Annualized Consumption Revenue). In the GCP ecosystem, consumption is king. Google's own data indicates that for every $1 of GCP consumption sold, partners generate over $7.54 in services and IP revenue. But that multiplier isn't evenly distributed. It is heavily skewed toward partners who drive compute (BigQuery analysis slots) rather than just storage.

When you assess your portfolio company, look for the "Consumption Moat." A generalist partner sells a VM, and the client tries to turn it off at night to save money. A Data partner implements a Looker dashboard used by the CRO every morning, or a Vertex AI model that powers real-time fraud detection. That consumption isn't a cost center; it's a revenue generator for the client. That makes the partner's services sticky.

Furthermore, the "Data Premium" defends against the technical debt red flags that often kill deals. Infrastructure code rots quickly. Data architectures—specifically well-governed semantic layers in Looker—tend to accrete value over time as more use cases are layered on top. This difference in asset appreciation is why strategic buyers like Accenture and Deloitte are aggressively consolidating the data niche while passing on pure-play infra shops.

The Diagnostic: Is Your "Data Practice" Real?

Many generalist partners try to dress up as data firms to capture this premium. They hire a few SQL developers and slap "BigQuery" on their slide deck. As an Operating Partner, you need to cut through the noise during your Revenue Quality Audit. Ask these three questions to determine if you truly hold a premium asset:

1. Are we selling "Pipelines" or "Outcomes"?

Commodity firms build pipelines (moving data from A to B). Premium firms build outcomes (dashboards, predictive models, customer segmentation). Check the SOWs. If the deliverables are defined in "hours of engineering," you have a staffing firm. If they are defined in "data products delivered," you have a premium consultancy.

2. What is our "Looker Attach Rate"?

BigQuery stores the data, but Looker makes it visible to business users. A high attach rate of Looker (or extensive Power BI integration on top of GCP) indicates that the partner has bridged the gap to the LOB (Line of Business) executive. If you are only talking to the CIO, your multiple is lower.

3. Do we own the IP or just the labor?

The highest valuations go to firms that have "productized" their data services—pre-built industry data models for Retail, FinServ, or Healthcare. If every project starts from a blank sheet of paper, your margins (and your multiple) will remain capped by the utilization trap.