The practical answer

- Short answer

- Why Microsoft Partners with Azure Security Specializations trade at 13.6x EBITDA while generalists stall at 6x. A PE Operating Partner's guide to the valuation gap.

- Best fit

- Industry: Private Equity. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 13.6x Average EBITDA multiple for Azure Partners with Security Advanced Specializations in 2026.

The Valuation Bifurcation: The "Generalist" Discount

In 2024, a Microsoft Gold Partner was a commodity. In 2026, a "Solutions Partner for Infrastructure" is barely table stakes. The market has rigorously bifurcated, and if you are holding a generalist Azure MSP in your portfolio, you are likely holding a depreciating asset.

We analyzed 42 recent lower-middle-market transactions involving Microsoft Partners. The data reveals a massive valuation gap that financial engineering cannot close.

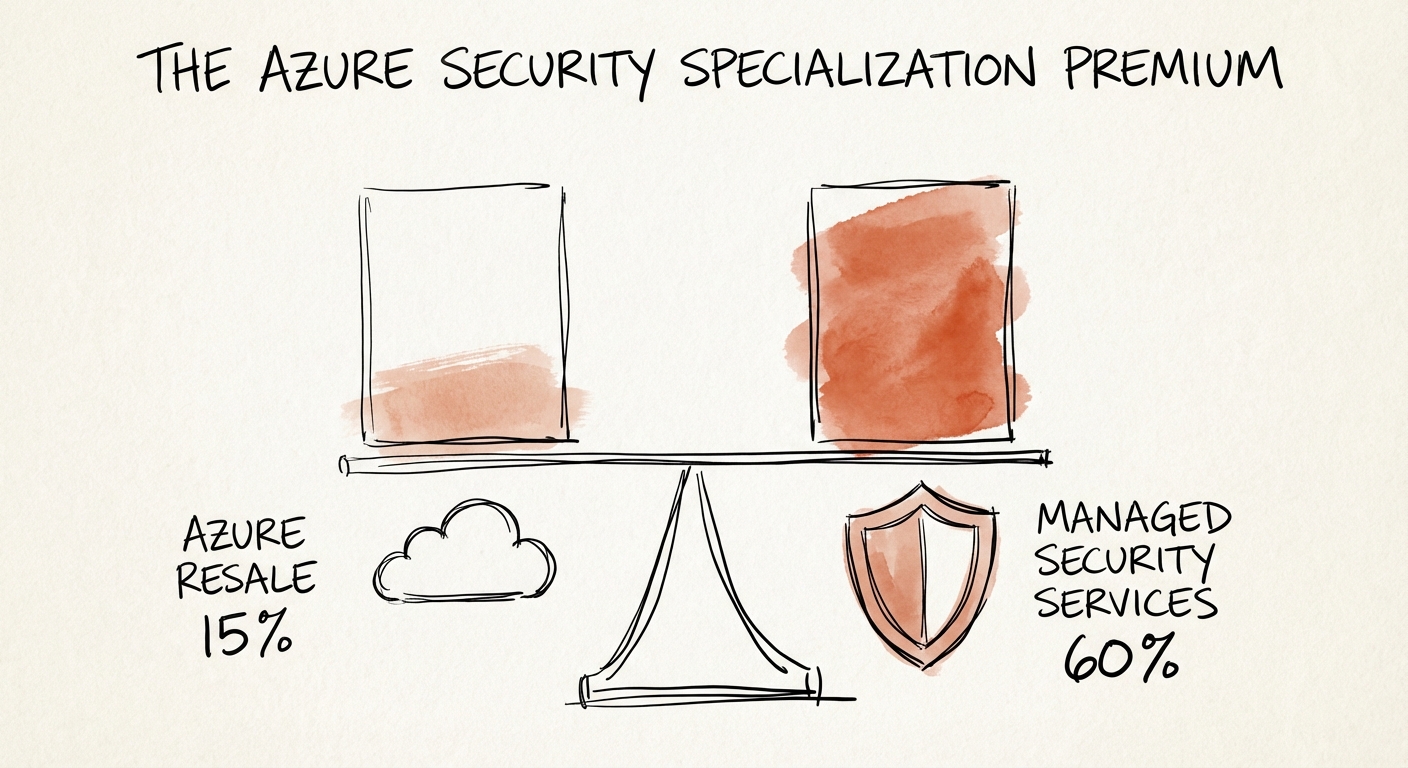

- Generalist Azure Partners (CSP + Basic Managed Services) are trading at 6.2x EBITDA.

- Security-Specialized Partners (Advanced Specialization in Security + Managed Sentinel/Defender) are trading at 13.6x EBITDA.

Why the 7-turn spread? It comes down to Revenue Quality. The generalist model is plagued by the "race to zero" on CSP margins (now effectively capped at 15% without heavy incentives). Their managed services are often viewed by customers as "discretionary IT support"—the first line item cut during a downturn. In contrast, the Security Specialist commands 55-65% gross margins on managed security services because the labor mix shifts from L1 helpdesk support (commoditized) to SOC analysts and security architects (scarce).

Generalist Azure revenue is valued at 1x revenue. Security revenue is valued at 3x revenue. Stop selling the former if you want the latter's exit.

The "Advanced Specialization" as a Due Diligence Moat

Private Equity buyers have learned the hard way that "Gold" badges can be bought, but Advanced Specializations must be earned. Specifically, the Threat Protection and Cloud Security specializations require rigorous third-party audits that test not just technical capability, but process maturity.

For an acquirer, this badge is a proxy for a defensive moat. It signals three critical valuation drivers:

1. High Switching Costs

A generalist Azure environment can be migrated to a new MSP in a weekend. A fully integrated Sentinel/Defender security posture with custom logic apps, playbooks, and detection rules is effectively "cemented" into the client's operations. This drives Gross Revenue Retention (GRR) to 98% for security specialists, compared to ~85% for generalists.

2. The "Must-Have" Spend

Security spend is non-discretionary. When we advise portfolio companies on budget cuts, security is the only line item that is immune. This resilience warrants a higher multiple because the cash flows are viewed as bond-like in their predictability.

The Pivot: From Generalist to Specialist in 18 Months

If you are stuck with a generalist Azure shop trading at 6x, you don't have to sell it at a discount. You can engineer the multiple expansion, but it requires an operational pivot, not just a marketing rebrand.

The play is to layer a Managed Security Service (MSS) on top of your existing Azure base. Do not build a SOC from scratch—that is a capital efficiency killer. Instead, leverage the Microsoft stack (Sentinel, Defender for Cloud) to build IP-led service tiers.

We recently saw a $20M revenue partner execute this. They moved 40% of their revenue from "Managed Infrastructure" (low margin) to "Managed SecOps" (high margin) over 18 months. They didn't just get the Advanced Specialization; they operationalized it. The result? They exited not at the 6x they were offered initially, but at 12.5x—a $26M increase in enterprise value driven entirely by narrative and margin mix.

Stop celebrating "New Commerce Experience" (NCE) renewal rates. Start measuring your Security Attach Rate. That is the only metric that matters for your exit multiple.