The practical answer

- Short answer

- Why Adobe Commerce specialists trade at 12x EBITDA while generalist partners stall at 6x. A diagnostic guide for PE sponsors on maximizing exit value.

- Best fit

- Industry: Private Equity. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 91% of retailers view composable architecture as critical, driving a valuation premium for agencies with headless expertise.

The Tale of Two Adobe Partners

In the private equity ecosystem, not all Adobe badges are created equal. We consistently see a valuation bifurcation that catches sponsors off guard: two firms with identical revenue, similar headcount, and the same "Gold" or "Platinum" Adobe Solution Partner status, yet one trades at 6x EBITDA and the other at 12x.

The difference isn't in the logo; it's in the workload. The 6x asset is effectively a digital marketing agency wrapping itself in technology services—implementing Adobe Experience Manager (AEM) for content, running campaigns, and billing by the hour for creative work. It is valued like a marketing agency because its revenue is discretionary. When budgets tighten, marketing is the first line item cut.

The 12x asset is a Commerce Specialist. This firm implements and manages mission-critical transactional infrastructure (Adobe Commerce/Magento). Their code processes revenue. If their work fails, the client stops making money immediately. This proximity to the transaction creates "defensive stickiness" that buyers—specifically strategic acquirers and larger PE platforms—pay a premium for.

The Multiplier Gap Data

Recent market data validates this split. According to 2025 benchmarks, generalist digital marketing agencies are trading between 4.5x and 7x EBITDA, driven by lower barriers to entry and higher customer churn risks. In contrast, specialized commerce infrastructure firms are commanding multiples north of 10x, with elite "composable" shops reaching 12x-14x. The market is effectively saying that a dollar of EBITDA generated from transactional infrastructure is worth double a dollar generated from creative services.

The market is effectively saying that a dollar of EBITDA generated from transactional infrastructure is worth double a dollar generated from creative services.

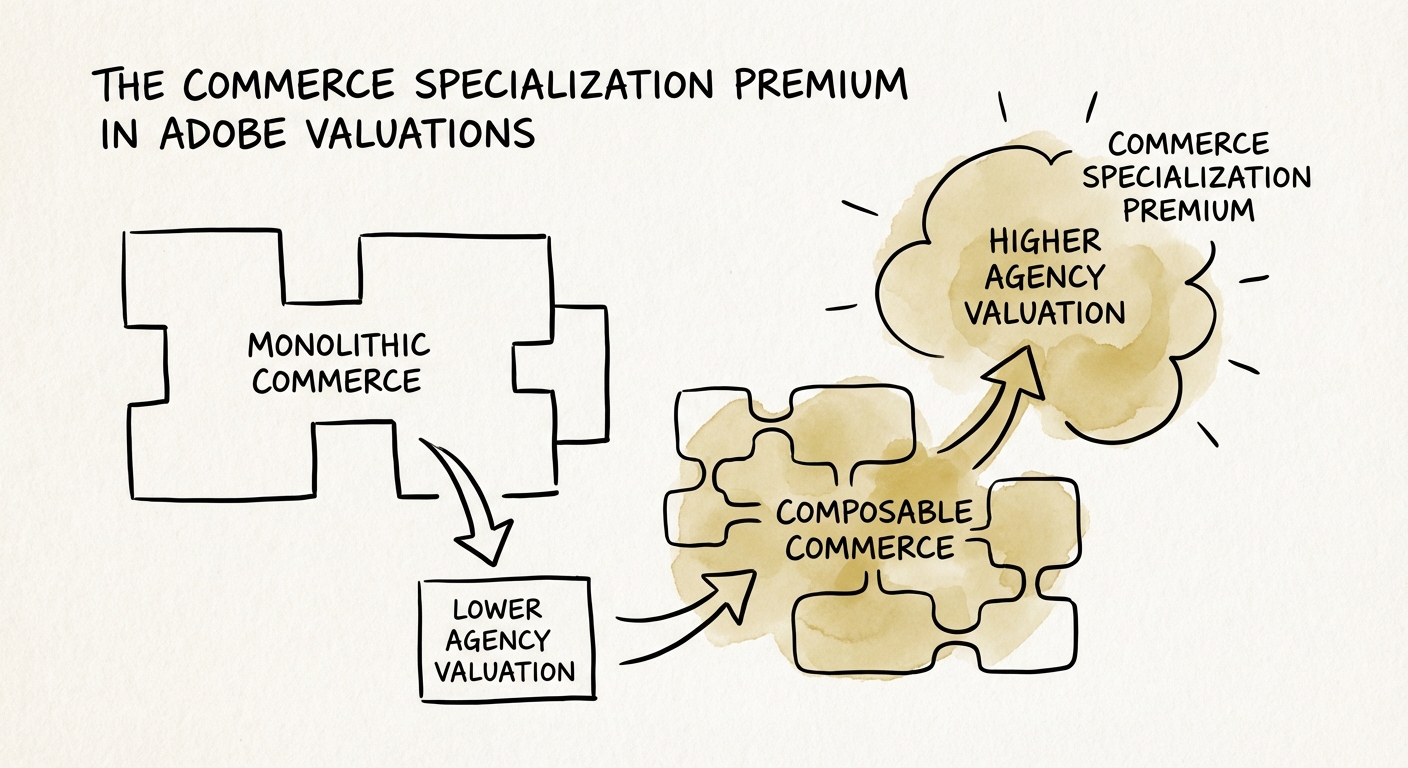

The "Composable" Moat vs. The Monolithic Trap

The second major driver of the Commerce Premium is architectural. The Adobe ecosystem is undergoing a massive shift from monolithic "all-in-one" architectures to "composable" (API-first, headless) strategies. This shift has created a dangerous trap for PE sponsors holding legacy Magento shops.

A "lift and shift" shop—one that simply installs the standard Adobe Commerce software and customizes themes—is rapidly becoming a distressed asset. These firms face commoditization as AI automates basic coding tasks and low-cost offshore providers dominate the market. Their valuation is capped because their technical differentiation is near zero.

The premium belongs to partners mastering Composable Commerce. These firms don't just "install software"; they architect complex data flows between ERPs, PIMs, and front-end experiences. Research indicates that 91% of retailers now view composable architecture as critical to their strategy. Consequently, acquirers view composable-native agencies as "future-proof" platforms, while monolithic shops are viewed as "fixer-uppers" requiring significant R&D investment.

Identifying the "Fake" Specialist

In due diligence, do not rely on the "Platinum" partner status alone. That status often reflects license resale revenue rather than technical capability. Instead, audit the ratio of Adobe Certified Experts (ACEs) to total delivery headcount. A generalist agency often has a ratio below 1:10. A true specialist maintains a ratio closer to 1:3. This density of certified talent is a primary indicator of the human capital quality that defends the premium multiple.

From Service Shop to Strategic Asset

If your portfolio company is currently trading at the 6x "Agency" level, bridging the gap to a 12x "Commerce" exit requires a deliberate operational pivot over 18-24 months. You cannot simply market your way to a higher multiple; you must fundamentally change the revenue quality.

1. Pivot to Managed Services (AMS): Move away from pure project revenue. Project revenue resets to zero every January 1st. High-value commerce shops typically generate 40-50% of revenue from recurring Application Management Services (AMS). This is not "support"; it is continuous optimization of the transaction engine.

2. Specialize in B2B Complexity: The B2C commerce market is crowded. The B2B market—involving complex pricing tiers, punch-out catalogs, and ERP integrations—is where the scarcity value lies. A firm known for solving "impossible" B2B manufacturing commerce problems commands a significantly higher multiple than one launching fashion boutiques.

3. Document the IP: Buyers pay for systems, not heroes. If your commerce practice relies on three key architects to deliver every project, you have a Key Person Risk discount, not a specialization premium. Documented accelerators, connectors, and deployment frameworks convert "tribal knowledge" into transferrable intellectual property, directly impacting the Quality of Earnings.