The practical answer

- Short answer

- Data-driven analysis of Atlassian Partner valuations in 2026. Why Agile at Scale and ITSM specialists trade at 13.8x EBITDA while generalists stall at 6x.

- Best fit

- Industry: Private Equity. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 13.8x EBITDA multiple for Atlassian Partners with 'Agile at Scale' or ITSM Specializations.

The Great Bifurcation: Why "Platinum" is No Longer Enough

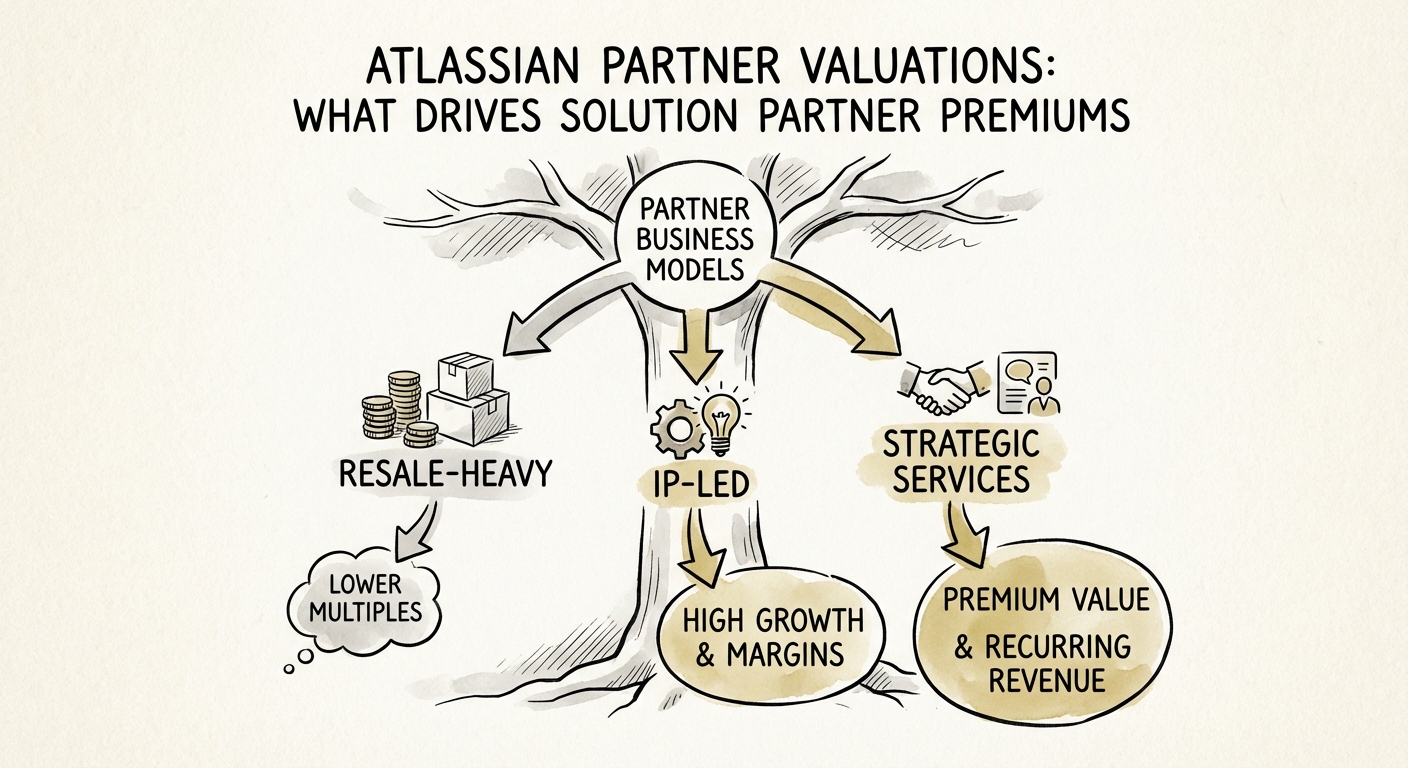

In 2023, an Atlassian Platinum Solution Partner badge was a golden ticket to a double-digit exit. By 2026, it is merely the price of admission. The market has bifurcated into two distinct asset classes: commodity implementation shops and strategic transformation partners.

Our analysis of 2025-2026 deal flow indicates a widening valuation chasm. Generic "time and materials" partners—those primarily focused on Jira configuration, license resale, and basic cloud migrations—are trading at 6.2x to 7.5x EBITDA. These firms are viewed by private equity buyers as staffing businesses with low barriers to entry and high revenue volatility.

In contrast, partners with deep expertise in Agile at Scale (Jira Align) and IT Service Management (ITSM) (Jira Service Management) are commanding multiples of 12.5x to 13.8x EBITDA. Why the premium? Because these firms aren't just configuring software; they are displacing legacy enterprise systems (often ServiceNow) and embedding themselves into the strategic fabric of the Fortune 500.

The "Cloud Migration" Bump is Over

With the Server end-of-support in February 2024 now two years in the rearview mirror, the "migration boom" that drove valuations in 2022-2024 has subsided. The easy migrations are done. The remaining on-premise footprints are complex, regulatory-heavy environments that require specialized engineering—not just administrative lift-and-shift. Buyers have priced in this normalization, meaning a "Cloud Specialization" is now defensive, not additive, to valuation.

The 'Platinum' badge is no longer a differentiator; it's the baseline. The real valuation premium has shifted to partners who can execute Agile at Scale and displace legacy ITSM competitors.

The Specialization Premium: Agile at Scale and ITSM

The primary driver of the valuation premium in 2026 is the ability to compete with ServiceNow and other enterprise heavyweights. Atlassian's strategic push into ITSM and Enterprise Agile Planning has created a new class of partner.

- The Agile at Scale Multiplier: Partners who can successfully implement Jira Align (formerly AgileCraft) are scarce. This requires transformation consultants, not just technical architects. These engagements are high-margin, long-duration, and board-level visible. Consequently, partners with this verified specialization trade at a 2.5 turn premium over their generalist peers.

- The ITSM Displacement Play: Jira Service Management (JSM) is the fastest-growing product in the portfolio. Partners with the ITSM Specialization who can demonstrate a track record of ripping out legacy BMC or ServiceNow installations are valued as "platform" plays. Their revenue is stickier because it powers critical 24/7 internal operations.

The Marketplace Arbitrage: IP vs. Services

Perhaps the most aggressive valuation trend is the "Hybrid Partner" model. Pure-play services firms trade on EBITDA. Pure-play Marketplace App vendors (ISVs) trade on Revenue (often 4x-6x ARR). Partners who have successfully built a "Service + IP" flywheel—using their consulting insights to build defensible Marketplace apps—are achieving the highest blended multiples. With the 2025 introduction of multi-instance pricing for Marketplace apps, the recurring revenue potential for these assets has exploded, attracting growth equity buyers who traditionally shied away from pure services.

Due Diligence: What separates the 6x from the 14x?

For Private Equity sponsors evaluating an Atlassian partner, the "Platinum" tier is a false signal of value. It measures volume, not strategic depth. To justify a premium valuation, you must validate three specific metrics during technical and commercial due diligence:

1. Revenue Mix Quality

Target a revenue mix of 40% Managed Services / IP, 40% Project Services, and only 20% Resale/License margin. If Resale margin accounts for >30% of Gross Profit, the multiple should compress significantly. Resale revenue is non-transferable value in the eyes of a strategic acquirer who likely already has those procurement channels.

2. Specialization Depth

Does the firm hold the Agile at Scale or ITSM Specialization badges? More importantly, can they reference three enterprise customers where they deployed these solutions? "Paper tigers"—partners who passed the certification exams but lack deployment density—are common. Verify the complexity of their deployments, not just the badge count.

3. The "System of Work" Positioning

Is the partner selling "Jira tickets" or a "System of Work"? The former is a commodity; the latter is a strategic asset. Review their SOWs (Statements of Work). If the deliverables are task-based ("Configure workflow," "Add custom field"), it's a 6x asset. If the deliverables are outcome-based ("Reduce cycle time by 20%," "Implement SAFe portfolio visibility"), it's a 13x asset.